Are You Positioned For The Value Cycle To Run?

Fourth Quarter 2021 Commentary

This Pzena Investment Management, LLC (“Pzena”) commentary is a historical document and is intended solely for informational purposes. The views expressed reflect the views of Pzena Investment Management (“PIM”) as of the date published and are subject to change. Neither the writer nor PIM undertake to advise you of any changes in the views expressed therein. There is no guarantee that any projection, forecast, or opinion in this material has been or will be realized. Past performance is not indicative of future results. All investments involve risk, including risk of total loss.

For Financial Advisor Use Only

Severe underperformance by specific emerging-market countries has historically created a fertile hunting ground to find alpha-generating stocks. We are finding good value opportunities in 2021’s laggards.

While developed markets were strong in 2021 with most countries posting positive returns, emerging markets lagged significantly. The broad MSCI Emerging Markets Index came in slightly lower for the year despite most countries moving higher, as notable laggards such as China, Turkey, and Brazil each faced unique macro uncertainties, and were all sharply lower. Ardent fundamental value investors view this wholesale selling, and the resulting cheap prices caused by the uncertainty, as opportunities to explore and potentially initiate positions in select companies at attractive starting points. For China in particular, investors who enjoyed several years of stability, growth, and perceived safety fled the increasingly uncertain environment, as the government took actions investors see as anti-capitalist. While the circumstances creating potential opportunity in particular countries may be unique, experienced value investors are accustomed to uncertainty; in fact, we seek it out to identify mispricing and thus raise the opportunity for superior returns.

FINDING VALUE IN EMERGING MARKETS

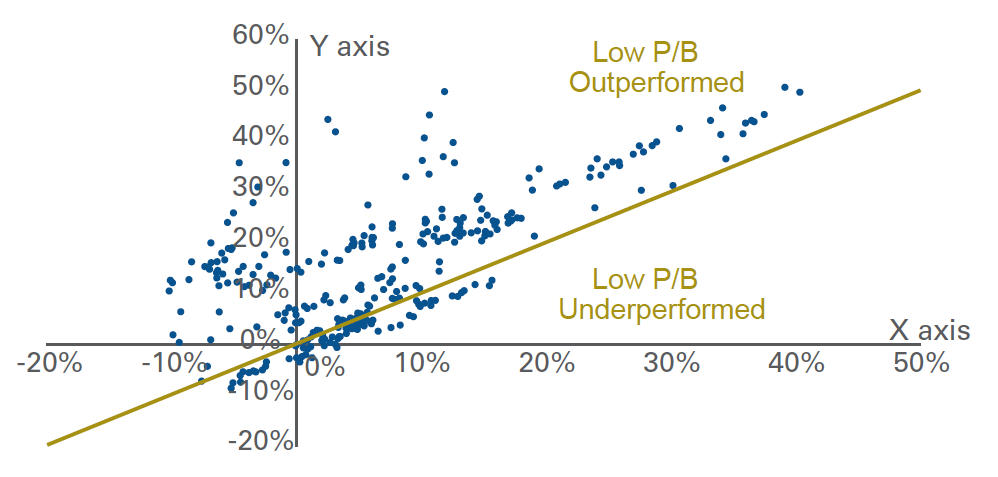

There are numerous studies showing that value philosophy works across market cap, geography, and asset classes. Before we started managing emerging- market portfolios in 2008, we undertook a study to see how value performed in emerging-market countries, and found it worked quite well (Exhibit 1).

Exhibit 1 – 5-Year Rolling Returns of Low Price/Book* vs. MSCI EM Index 1992 – 2021

Y axis: Monthly rolling 5-year USD annualized return of Low Price/Book*

X axis: Monthly rolling 5-year USD annualized return of MSCI Emerging Markets Index (gross returns)

Source: MSCI, Sanford C. Bernstein & Co., Pzena analysis

*Cheapest quintile price to book of MSCI EM universe (equal-weighted data);Does not represent any specific Pzena product or service. Data through December 31, 2021. Past performance is not indicative of future returns.

Many view emerging-market investing as a growth story, but over time, the value approach has proven superior. Higher beta emerging markets endure more frequent bouts of volatility but offer amplified return potential for value investors for several reasons, including:

Psychology — Investors tend to exaggerate the significance of near-term problems and discount

the potential for business, industry, management, currency, or macroeconomic improvements over time. The emotional response is more pronounced in emerging markets, adding to valuation dispersions that offer opportunities when deeper discounts are ascribed to out-of-favor companies.

Earnings power — Despite a lack of empirical evidence, investors often associate GDP growth with higher equity returns. When growth-seeking investors don’t achieve the quick gains they’re looking for, their reaction to disappointment can be amplified, presenting opportunity to the disciplined value investor.

Wide range of outcomes — The array of political and legal structures, currencies, and governance practices each add to the complexity in emerging markets. The variety of economies, industries, and market capitalizations offer robust opportunities across a large pool of stocks.

Underexploited — Most investment managers tend to favor macroeconomic or quantitative approaches to investing in emerging markets, leading to crowded trades and wider market swings.

These factors are ever-present in emerging markets, though they are usually ignored when markets perform well and can make entire markets “uninvestable” during times of uncertainty. Uninvestable situations, implying investors wouldn’t purchase at any price, are something value investors find intriguing. These opportunities to purchase stocks with low expectations, at low starting points, sow the seeds for future outperformance.

COUNTRY-SPECIFIC OPPORTUNITIES

Geographic, or country-specific opportunities, which arise when a region or country faces an uncertainty that others don’t, are more pronounced in the emerging markets. While there are periods where general fears lead to broad underperformance versus developed markets, country-specific fears are far more prevalent. Uncertainty can make a specific country uninvestable to many, leading to share prices that decouple from the broad emerging-markets index, often creating an asymmetric risk/reward profile. Countries, however, do generally recover, and good businesses find ways to navigate crises.

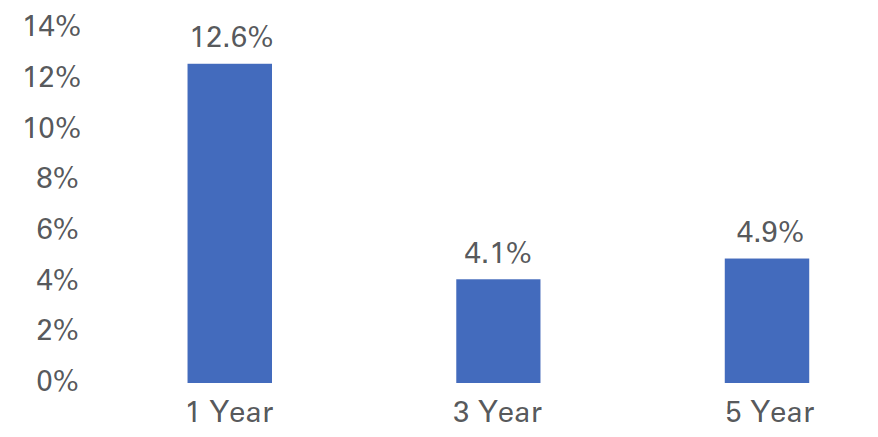

The disciplined value investor sees these collapsing stock prices as opportunities to begin deep fundamental company-level research, seeking to identify strong companies unduly punished by a sweeping reaction to temporary issues. Is this a sound strategy, and do countries actually recover? We studied this phenomenon and found significant long-term alpha potential available to investors who adhere to this discipline.

We looked at significant emerging-market country declines, defined as 2,000 basis points or more

of underperformance versus the MSCI Emerging Markets Index over the prior 12 months, and then looked at how those countries performed over the next several years. Our data set includes 30 years of data for 10 different countries (some did not have data for the full period). In these instances, we found 4.9% of outperformance per annum, on average, versus the MSCI Emerging Markets Index over the five years following those steep declines (Exhibit 2).

Exhibit 2 – Average Annualized Alpha of EM Countries Following Steep 12 Month Underperformance

Source: MSCI, Pzena analysis

The data set is from January 1, 1992 through December 31, 2021 and includes 10 different countries (some did not have data for the full period). The 10 countries chosen were the 10 largest weightings held in the MSCI Emerging Markets Index (as of December 31, 2021) that have at least a 10-year MSCI track record. Data in US dollars. Past performance is not indicative of future returns.

Like all strategies that create significant alpha, this approach doesn’t always work. In fact, it generated alpha about 60% of the time. This is what value investors expect; if the strategy worked all the time, it would not generate subsequent annual outperformance, as there would be no associated uncertainty with investigating beaten-down emerging-market countries. The key is to recognize that it will not always work, and therefore focus on the significant alpha generated over the long term.

OPPORTUNITY IN EMERGING MARKET UNCERTAINTY

Macroeconomic issues specific to emerging- market countries over the past 12 months have created many value opportunities. China is a good example of an entire country experiencing uncertainty. From 2016-2020 China was seen as an emerging market safe haven and generated a 19% compound annual return. In 2021, however, market perception deemed China uninvestable, and the MSCI China Index declined by 22%, trailing the rest of emerging markets by more than 30 percentage points. As our study showed, this level of market underperformance is generally a good investment starting point, with subsequent outperformance typically led by the most undervalued stocks. We recently built positions in Chinese internet e-commerce giant Alibaba and property company China Overseas Land and Investment (COLI). (For additional detail, revisit our 3Q21 Newsletter.) However, there are statistically cheap areas that we are avoiding, as they offer poor risk/reward profiles, such as the education sector.

History has shown that stock market sell-offs are generally a good time to dedicate resources to research beaten-down geographies. As investors fear uncertain macroeconomic outlooks, we are finding fantastic emerging-market businesses trading at a fraction of their intrinsic values.

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results. All investments involve risk, including risk of total loss.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity performance of emerging markets, and provides equity returns including dividends net of withholding tax rates as calculated by MSCI. The index cannot be invested in directly.

For U.K. Investors Only:

This financial promotion is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Mirabella Advisers LLP, which is authorised and regulated by the Financial Conduct Authority. The Pzena documents are only made available to professional clients and eligible counterparties as defined by the FCA. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For EU Investors Only:

This financial promotion is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2021. All rights reserved.