2022 Stewardship Report

A MESSAGE FROM OUR CEO

ESG integration means fully understanding the value opportunity at stake for a given company. As value managers, we look to improvement in business fundamentals as a source of excess return. Where ESG issues are financially material, ESG improvement may also be a source of alpha. We believe that value isn’t a factor – it’s a philosophy of investing in out of favor stocks that are systemically undervalued; similarly, we do not think in terms of “good” or “bad” ESG stocks. Rather, we focus on the embedded investment opportunity, ESG or otherwise.

Stewardship (through direct engagement and proxy voting) is one of the more effective tools that an active manager such as Pzena has at its disposal to exert a constructive, long-term-oriented influence on the trajectory of a company. We view stock ownership as an opportunity to help steer companies in the direction of creating long-term value for our clients, and therefore explicitly favor engagement over divestment.

We hope this inaugural stewardship report gives a sense of the engagement we have with companies in which we invest. We believe that true ESG integration should be industry-analyst led, and therefore what follows by way of examples reflects the investment analyst perspective on key engagements from the prior calendar year.

CAROLINE CAI

Chief Executive Officer and Portfolio Manager

Pzena Approach to Stewardship

At Pzena, our role as responsible stewards of capital is an integral part of our fiduciary responsibility to act in our clients’ best interests, maximizing long-term shareholder value.

As value investors, we often find ourselves in situations where something has gone wrong, and we rely on fundamental research to assess the likelihood of improvement on these issues. Taking advantage of the gap between a valuation that reflects near term challenges compared to the value of the long-term earnings power of the company is the heart of our investment philosophy. In some cases, the issues or opportunities facing a company fall under the ESG umbrella.

Deep research and extensive engagement can help value investors capitalize on controversy and access this potential source of alpha, making engagement a cornerstone of our investment philosophy and a critical component of our process as long-term active investors.

As we do with all key investment issues, significant ESG considerations are analyzed internally, discussed with company management and industry experts, and monitored. Each step of this process contributes to the team’s determination of whether to invest and, if we do, at what position size. Once an investment has been made, we continue to engage management on an ongoing basis. Through these conversations, along with our proxy voting and other escalation options, we seek to exert influence in a constructive way, oriented toward the long-term success of the company.

ENGAGEMENT APPROACH

We engage with company management throughout our due diligence process, and extensively after an investment is made, on all material or potentially material investment issues. As shareholders, we believe we have the opportunity to help guide companies toward long-term value creation, and therefore prefer engagement over divestment.

If we determine an ESG consideration to be material to our investment thesis, we raise it with the management team. Each company and management team is unique. Consequently, our approach to management conversations is organic in each case; however, we always seek an open, cooperative dialogue. We prefer to maintain an ongoing dialogue with company management through regular meetings, in-person site visits, and calls. When we engage with companies, we are typically speaking to some combination of the following: senior management team, members of the board, ESG or sustainability lead, and investor relations.

Roles & Responsibilities

For ESG to be integrated into the research process, the industry analyst covering the stock must also lead the associated investment due diligence, of which engagement is a key part. The industry analysts are best placed to evaluate the investment implications of ESG issues, and therefore they bear primary responsibility for discussing these with company management. Our ESG analysts support the industry analysts in these conversations as needed, but we intentionally do not delegate these responsibilities to a separate stewardship team.

Engagement Purpose

Broadly speaking, our discussions with company management have the following purposes in mind:

- Testing assumptions — intended to deepen our understanding of issues that we have identified as material or potentially material to the investment. Sometimes we identify these issues at the point of investment and other times they arise during ownership. In both cases, we discuss the issues with management, solicit their input, assess their response, and evaluate the impact on our investment thesis. To the extent that the issues are ongoing, we continue to follow up until the issue is resolved or no longer relevant.

- Maintaining an informed dialogue — whereby we keep apprised of decisions relating to strategic and operational considerations. We routinely meet with management following earnings, strategic business updates, and management transitions.

- Advocacy – an explicit opportunity for us, as shareholders, to advocate for different decisions that we believe will enhance long-term shareholder value. With increasing regularity, companies also proactively seek our input on a range of issues.

The success of each engagement is measured on a case-by-case basis, depending on the company-specific context and goals of the engagement. Below are some examples of different engagements we have had with companies with one or more of the above purposes in mind.

![]()

BASF: German multinational chemical company

The most material ESG issue facing BASF is finding a way to decarbonize operations. We engage regularly on this issue in our conversations with management. However, the challenge for BASF, along with the chemicals industry as a whole, is that getting to Net Zero by 2050 will require considerable financial investment and in some cases the application of new technologies that are not yet commercially viable.

Our research and engagement have focused on how BASF will continue to grow the business and simultaneously reduce emissions over time. While there is a cost to developing and implementing emissions reduction technologies, we view BASF as competitively positioned because of its best-in-class R&D platform and integrated (and therefore more efficient) Verbund approach to production. BASF’s phased strategy to decarbonize and grow includes the following:

- Converting fossil fuel cogeneration plants to run on renewable

- Capturing value uplift from increasing demand for low-carbon footprint and sustainable product

- Scaling carbon-efficient technologies as they become economic (e.g., blue and green hydrogen, e-cracking)

We are also continually tracking BASF’s emissions reductions trajectory. Based on our discussions with management, BASF has a reasonable line of sight to hitting its 2030 target to reduce Scope 1 & 2 emissions by 25% (baseline 2018). Meeting these targets requires an estimated associated capex of €1B over the next 5 years and a further €2-3B between 2026-2030, which is modest relative to the total capex spend of €25.6B from 2022-2026.

Management acknowledges that the path beyond 2030 remains more uncertain for BASF and the industry, both in terms of emissions reductions and associated capex, due to lack of clarity on which emissions reduction technologies will become commercially viable. BASF is engaged in exploratory technology development, and we continue to discuss these developments with management. Based on recent conversations, BASF expects to spend another €10B after 2030 to hit its 2050 net zero target. The financial impact of this net zero plan is reflected in our forecast. We are also anticipating an accelerated pace of decarbonization of BASF’s European assets in response to the ongoing energy crisis in Europe.

![]()

Andritz: international engineering and construction company

Andritz has been on our radar for having a higher risk of labor and project governance issues purely due to the nature of its business, mobilizing a low-cost workforce to work on different projects around the world. We have analyzed these risks and engaged management, which has led us to the conclusion that Andritz is a responsible operator.

Strong policies, procedures, and operating practices are, however, not a guarantee that there will never be project-specific issues. It came to our attention that a third party had flagged Andritz for historical issues in their hydro business and alleged human rights violations at associated infrastructure projects. After engaging Andritz on these concerns, it became clear that the third party had an incorrect interpretation of events. Andritz was merely part of a consortium of entities as an equipment supplier and was not running the alleged forced labor camp. We also learned through engagement that Andritz maintains a very rigorous project management checklist for projects (including environmental and social issues) and has stepped back from the bidding process when their checklist is not met. Andritz is actively engaged in trying to correct the third party’s assessment, and Andritz’ ESG rating has already been upgraded.

In this case, our engagement with Andritz confirmed our view that it is a responsible operator and helped Andritz correct market misperceptions of its ESG credentials. We will continue to engage on the operating practices at Andritz to make sure there is no change in our assessment and perception of the risk profile of the investment.

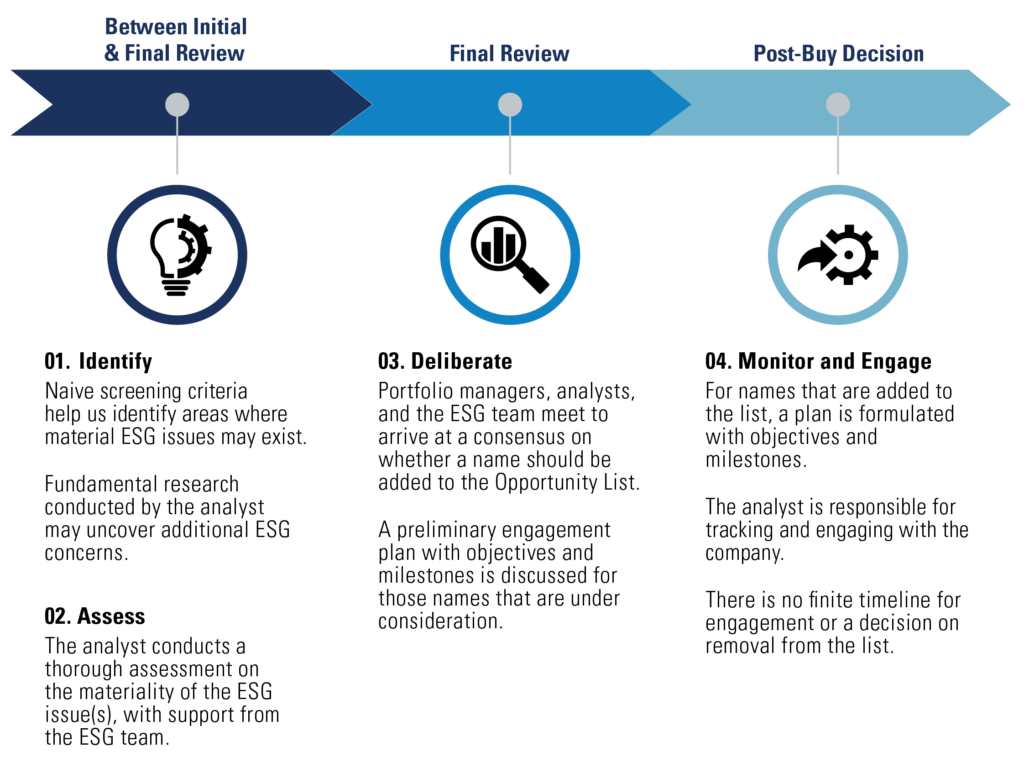

SPOTLIGHT: OPPORTUNITY LIST

The belief in our ability to push for better outcomes by engaging with the companies we own has been a driving force behind the development and application of the Pzena Opportunity List. The Opportunity List seeks to systematically identify opportunities in our portfolio where material ESG issues exist and engagement could have a positive impact. If we choose to add a company to the Opportunity List, it means there is significant room for improvement on material ESG considerations.

Once a company is placed on the Opportunity List, we create an engagement plan with specific objectives and milestones to track progress. In practice, progress against the engagement plan will not manifest all at once, but will appear in incremental steps over the investment time horizon. If we see a company is trending off-track, we have several options to escalate engagement. Persistent failures to address our concerns could lead to our reevaluation of the investment thesis and potential divestment.

In some cases, removal from the Opportunity List will come with the gradual resolution of the ESG issue(s) over time and/or only requires discreet changes, such as the resolution of a pending litigation. In many cases, removal is more nuanced and requires continuous research, engagement, and monitoring. Regardless, all investments require us to be in dialogue with management and to respond to changes that may impact the range of investment outcomes.

OpportunityListProcess

Opportunity List Engagement Examples

Hon Hai: Taiwanese electronics manufacturer

Labor is both a critical business resource and potential risk factor for Hon Hai. From a business perspective, ensuring a supply chain that meets international standards is critical to the long-term success of the company. For example, Hon Hai has been subject to inspection of its facilities and practices by customers, including Apple, for which it is a major supplier. There is a risk that Apple will choose to diversify if Hon Hai is seen to mismanage its workforce. We therefore consider social issues a tail risk that we continue to monitor. In 2022, there have been several labor-related issues which have required an ongoing dialogue with Hon Hai, and we therefore added Hon Hai to the Opportunity List.

In early 2020, Hon Hai was accused of using controversial Uighur labor by an Australian think tank report. We took these allegations seriously and engaged with Hon Hai. In so doing, we could not find any evidence of complicity in the mistreatment of Uighur and other minorities inside and outside Xinjiang. Hon Hai, along with a wide range of manufacturers in China, participated in the government’s ‘poverty alleviation’ program and employed Uighur workers in its factories in the past. However, as the program generated significant controversy, Hon Hai Investor Relations indicated to us that they have discontinued participation in the program.

However, this issue resurfaced in late 2022 when other organizations picked up on the same 2020 report. We re-engaged with Hon Hai and believe there is no new information, as the 2022 reports were referring to the prior 2020 report. Hon Hai has since conducted a series of independent third-party audits of its facilities, and none of them have evidence of forced labor at Hon Hai campuses.

In early 2022, we engaged with Hon Hai on allegations that worker dormitories and dining rooms in Indian facilities did not meet required standards. Indian operations account for less than 2% of Hon Hai’s total production, though this incident led to Apple putting Hon Hai on probation as a supplier. Our assessment was that, while regrettable, it was an isolated incident, and we were pleased with Hon Hai’s corrective actions. These actions included raising its code of conduct and operating practices to global standards and replacing the local operating team that presided over this issue.

Most recently in November 2022, worker protests erupted at Hon Hai’s Zhengzhou campus in response to strict COVID lockdown measures and delayed incentive payments. It appears these were caused in part by a technical error in the Hon Hai payments system. We engaged with Hon Hai and learned that there may also have been shortcomings in the recruitment process, including miscommunication of the timeline of incentive payments and hiring too many new workers for one campus at one time. Our assessment is that this is another regrettable incident, but not necessarily one indicative of broken corporate culture or management practices. Hon Hai emphasized the negative impact strict COVID-19 policies have had on employee relations and the ongoing importance of anonymous channels by which employees can report any concerns. While we see scope for improvement at Hon Hai, we recognize the unique challenge of operating a massive and highly labor-intensive process in the chaotic and uncertain environment under the zero COVID policy.

We continue to advocate for increased transparency of reporting on these issues, and, while we are disappointed to see a recurrence of labor-related issues, we are pleased that Hon Hai is more proactive in disclosing information and discussing these incidents with shareholders. It is our assessment that management is focused on compliance with best practice operating standards, including a commitment to human rights and equal treatment of workers. We maintain an ongoing dialogue with the company on labor issues and will only consider removing Hon Hai from the Opportunity List once we feel more confident these issues are behind the company and the risk of losing market share is reduced.

Edison International: U.S. regulated utility

We view Edison International as an overall above-average ESG performer in the industry. Edison has a history of generally positive trends in resource intensity and workforce safety, in addition to well-articulated decarbonization strategies in line with California’s ambitious climate change and air quality goals. It is exposure to wildfire-related liabilities that led us to add Edison to the Opportunity List. This exposure, while presenting a valuation opportunity, will also likely imply structurally higher risk going forward given increasing wildfire frequency and severity, associated (in large part) with climate change.

The challenge of navigating the shifting complexities of wildfire liability offers Edison unique potential opportunities to collaborate with the state of California in reducing wildfire risk and mitigating financial impact. We believe Edison is well positioned, given its reputation and strong business, including a robust operational and technological approach to building a climate-resilient energy system.

In recent years, Edison management has noted highly risky conditions continue; however, catastrophic wildfires have quelled. Edison attributes the 65-70% risk reduction to their mitigation investments. These include fire prevention capex, targeted shutoffs, situational awareness, vegetation management and partnerships on suppression.

We continuously engage Edison about their capex project to deploy miles of covered conductor to the high-risk areas. In the last few years, we have been pleased to see progress towards objectives put in place early on. The aim is 10,000 miles of covered conductor in total (5000 by 2023), 3,600 of which has been deployed so far. Edison has worked for approval from the California Public Utilities Commission for certain permissions around how much conductor they may deploy. We anticipate the partnership will continue, and additional fillings will be approved. Leveraging this partnership has proven successful for an even more effective risk mitigation strategy than Edison acting alone.

We continue to engage with the objective of tracking and assessing Edison’s success with their capex goals and the overall ongoing wildfire mitigation plans.

![]()

Isuzu: Japanese automaker

For some auto makers, a return to normal earnings may hinge on how effectively they can address growing demand for electric vehicles (EVs). Isuzu is a case of an Opportunity List company that we felt was not adequately addressing this market reality, with no carbon neutrality strategy or published plans for EV rollout. We added Isuzu to the Opportunity List with the goal of encouraging management to set a coherent transition strategy.

Through multiple engagements in 2021, we monitored the steps management was taking to advance that strategy. This included strategic partnerships they were planning with Hino and Toyota to develop fuel cell and electric light trucks. In the second quarter of 2022, Isuzu published its plan to achieve carbon neutrality in its operations, beginning with a goal to halve scope 1 and 2 CO2 emissions by 2030. Additionally, management set a timeline to research and develop the conversion of the product lineup of light-duty and heavy-duty trucks and buses to electric and hybrid models with short and medium-term development targets.

These insights assured us that management is appropriately positioning the business for the EV transition, and their capex plans and timeline seem reasonable. This led to the determination that Isuzu could be removed from the Opportunity List. We will continue to engage with management to ensure the company is following through on the stated plan.

![]()

Ube: Japanese chemicals company

Ube Industries is on our Opportunity List because it is in the 10th decile of carbon emissions intensity for our Japanese investment universe. The high carbon emissions intensity results primarily from its chemicals and cement businesses (the latter of which is now reported off balance sheet following recent deconsolidation). Our ongoing engagement efforts are therefore focused on Ube’s decarbonization plan.

Ube’s decarbonization targets include:

- Reduce scope 1 and 2 greenhouse gas emissions 55% by 2030

- Achieve carbon neutrality by 2050

- Lower emissions in the cement business

When assessing decarbonization plans, we are focused on credibility and rigor, as well as what makes sense from a long-term shareholder value creation perspective. We are encouraging Ube management to provide additional granularity on the steps towards their reduction targets for 2030 and 2050, as well as the associated financial implications.

Ube management has a line of sight to hit the 2030 emissions reduction target (primarily from closing ammonia production in Japan by 2030) but lacks detail for the 2030-2050 timeline. This is partly because the path to Net Zero for the chemicals and cement industries remains somewhat uncertain; the commercial viability of technology required to significantly reduce emissions for these sectors is unclear (e.g., carbon capture and storage). We will continue to engage on this topic and encourage Ube to release more details on their long-term decarbonization plan as soon as possible.

In the meantime, the deconsolidation of the cement business and the chemicals segment restructuring will considerably lower Ube’s emissions baseline. There will be inevitable reporting complexities, so we will need to closely monitor how Ube plans to report emissions moving forward.

![]()

Volkswagen: German automaker

From a third-party ESG ratings perspective, Volkswagen is a poor performer. These ratings are largely reactive to the 2015 “Dieselgate” emissions scandal, one of the worst ESG-related controversies in corporate history from a cost perspective. ESG improvement has been central to our investment thesis for Volkswagen, which made it a natural candidate for our Opportunity List. We spend considerable time engaging with management on the two most material ESG considerations: electrification and corporate governance.

Overall, we are pleased with Volkswagen’s electrification strategy and the pace at which it is being rolled out across Europe. As part of the Opportunity List, we are continually tracking how the strategy may need to evolve with tightening EU emissions standards. Volkswagen (along with many peers) did not meet its 2020 emissions targets, which resulted in a costly fine of more than 100 million Euro. While Volkswagen met 2021 emissions standards and expects to comply with targets set by the government for the next couple of years, 2025 is the year to watch, as it is when the targets become significantly more challenging. We will continue to monitor progress and engage management to make sure we continue to agree with their strategic decisions.

With corporate governance arguably foundational to sound business strategy, it is unfortunate that there are clearly several governance shortcomings at Volkswagen. These include a lack of a fully independent audit committee, the entrenched power of the Porsche family, and labor unions that are often opposed to necessary business transformation initiatives. We continue to engage on these topics in the hope that we see some improvements.

There have been select yet notable improvements in corporate governance, including conformity with the German Corporate Governance Code and long-term equity grants for the top 7,000 managers so that decisions may be better aligned with shareholder interests. We hope to influence additional incremental governance improvements through our ongoing engagement efforts.

Opportunity List

Our Opportunity List provides us with a structure to utilize fundamental research for assessing the likelihood of issue improvements.

ADDITIONAL ENGAGEMENT TACTICS

Engagement Escalation

In instances where we feel that our concerns have not been adequately addressed during our routine engagement with management teams, we may consider the following actions to escalate our concerns:

- A private meeting with the chairman or other board members

- A written letter to members of the senior management team and/or board members

- Voting against members of the board or resolutions at annual general meetings

- Divestment if the lack of progress changes our view of the embedded risk-reward

Below are a few examples of where we have employed one or more of the escalation tactics outlined above:

![]()

Bangkok Bank: one of the largest commercial banks in Thailand

As an Opportunity List name, Bangkok Bank is a high priority for engagement. We wrote a formal letter to Bangkok Bank criticizing company governance standards (mainly board composition) and a lack of communication and transparency with investors. We received no response to our initial letter, but, in a subsequent engagement where we referred to our formal letter, we noted a more positive tone from the board, along with an offer to set up a call with the CEO. However, this meeting has still proven difficult to actualize, so we are considering additional engagement escalation steps. It can be more challenging in some markets than others to make progress through engagement, particularly on governance matters. We believe it is important to try to continue to raise the standard as much as possible, and, in some ways, persevering with stewardship activities is even more important in these contexts.

![]()

Oracle: US computer software company

In 2021, Oracle modified the performance stock option plan for 2018-2022 and extended it to 2025, as it was looking like most of the plan tranches would not be met. We disagree with the premise of modifying performance-based awards partway through because this undermines the purpose of having performance-related targets in the first place. We have engaged Oracle on this issue over the past few years and offered suggestions for a more appropriate way to continue to incentivize management, such as issuing a new award. We decided to vote against the compensation plan for the 2022 AGM and withhold votes for directors on the compensation committee to formally register our dissatisfaction with how compensation incentives have been handled.

![]()

Korea Shipbuilding and Offshore Engineering: South Korean shipbuilding and major heavy equipment manufacturer

Korea Shipbuilding and Offshore Engineering is an example where governance failures have significantly impacted the normal earnings of the company. Weak corporate governance, as evidenced by improper capital allocation decisions, nepotism in the management structure, poor hedging of commodity risk exposure, and lack of clarity around expected future divestments of the core operating businesses, has led us to reconsider the investment thesis. Despite our attempts to engage with the company and suggest shareholder-friendly ways to promote recovery, the lack of responsiveness from management is concerning and has impacted our evaluation of the range of outcomes. Even with an expected recovery in the macro environment positively impacting the global shipping industry, the deterioration in company operating fundamentals has convinced us Korea Shipbuilding and Offshore Engineering will not benefit from this cyclical return and has driven our consensus to divest.

Collaborative Engagement

While we typically prefer to engage directly with the companies we own, occasionally we recognize the potential benefits of collaborative engagement with other investors. In such cases, we may seek to work with other investors, but only when we believe it’s in our clients’ best interests and permissible under applicable laws and regulations.

Situations where we have found collaborative engagement helpful include, but are not limited to, advancing a shared agenda with clients for a particular portfolio company and/or working with other investors to share insights on a particular issue. For example, we spoke to various other investors and stakeholders as we were deciding how to approach a corporate governance issue at Danieli Group, an Italian supplier of equipment and plants to the metal industry. These discussions were an opportunity to share our views with other investors and amplify our message to Danieli through those who were like-minded.

There are also aspects of collaborative engagement efforts that are less well-aligned with our approach and investment philosophy. Firstly, we do not seek to become activists or insiders, nor do we encourage proxy battles. Instead. we prefer to maintain a constructive dialogue with management teams and work collaboratively to achieve the desired outcome.

Secondly, company-specific bottom-up ESG-integrated investment analysis is core to our investment philosophy and approach to stewardship. This naturally lends itself to a more company-specific approach to engagement. The perspective we want to bring to management teams is often more nuanced than some collaborative organizations allow. As such, we have not necessarily found collaborative engagement initiatives particularly helpful to advance our agenda with company management. If we were applying ESG themes top-down, it might make more sense to team up with other investors focusing on the same ESG theme. We also find we maintain good access to management teams through our concentrated portfolios and so have not needed to leverage these collaborative groups for the purpose of seeking an audience with management teams.

That said, we do periodically consider membership in some of these collaborative organizations and remain open to evolving our approach. Our ESG team has evaluated Climate Action 100+, the IIGCC, Ceres, and CII for potential membership. While we have no plans to join any of them at present, we keep them on our radar and remain open to joining any of them in the future. Our ESG team also spends significant time engaging with the ESG community through panels and other means. As members of the Principles for Responsible Investment (PRI), Sustainability Accounting Standards Board (SASB) Alliance, and the Net Zero Asset Management initiative (NZAMi), we frequently attend convenings with other members. The PRI has also launched a collaborative engagement portal which we will continue to monitor.

PROXY VOTING

Proxy voting is a critical component of our engagement efforts and ability to drive change. As such, we take our responsibilities as stewards of our clients’ capital seriously, actively voting the shares of companies in which we invest on their behalf as an integrated part of our investment process. Each proxy is voted in the best interest of our clients. We exercise proxy voting to highlight our views on management decisions, including ESG-related items, regardless of whether we agree with management’s recommendation. We evaluate each proxy item for any investment on its own merit and therefore vote on a case-by-case basis, informed by our PROXY VOTING POLICY.

By way of resources, Institutional Shareholder Services (ISS), provides us with a proxy analysis with supporting research and a vote recommendation for each shareholder meeting. Nevertheless, we retain ultimate responsibility for instructing ISS how to vote proxies on behalf of each individual proxy item for each company. We evaluate each proxy item for any investment on its own merit and therefore vote on a case-by-case basis.

We disclose our proxy voting records publicly, and they can be found AT THIS LINK.

Roles & Responsibilities

Each proxy is reviewed and voted by the industry analyst covering the stock. We intentionally do not outsource this responsibility to a separate stewardship team, as we consider it a fundamental part of our investment due diligence and engagement.

The ESG team assists the industry analyst in making a vote determination, primarily on ESG items where either the specific issue falls outside of the scope of our policy or the industry analyst thinks it would be helpful to seek additional guidance.

Our Director of Research is responsible for monitoring analyst compliance with voting procedures.

Significant Proxy Examples

Climate shareholder proposals at banks

This proxy season, banks have come under greater scrutiny as providers of financing to the fossil fuel industry through their loan and capital market activity. Climate-related proxies for financial institutions fell into two categories of proposals: 1) confirming investor satisfaction with banking climate targets; and 2) limiting the types of financing banks provide to the fossil fuel industry.

The first category, “Say-on-Climate” proposals, have become a means for shareholders to express support for, or dissatisfaction with, company climate strategy, including stated decarbonization targets. For a bank, this means phasing out direct emissions in their own operations, but more importantly, setting interim targets for decarbonization in high-emitting industries where they provide financing as well as committing to new financing in “greener” or sustainable alternatives. In 2022, several bank management teams requested shareholder input through management proposed “Say-on-Climate” votes. Within our portfolios, these votes came up at UBS, NatWest, and Standard Chartered. In these instances, we thoroughly reviewed the climate plans and spoke directly with the relevant stakeholders. Our votes in favor of the climate plans reflect our view that the management team is approaching decarbonization in a way that is beneficial for the long-term health of the business and its shareholders.

The second category of climate proposals we encountered during this proxy season arose from shareholder activist groups looking to immediately cease all funding of new fossil fuel projects. These proposals, inspired by the IEA Net Zero by 2050 report, which aims to limit global warming to 1.5 degrees Celsius by the end of the century, would require banks to commit (and in some cases amend their Articles of Incorporation) to bar any new financing of oil and gas fields or coal mining developments.

While we recognize the importance of the energy transition, we do not believe that a prescriptive ban on new fossil fuel financing is the best way to achieve global decarbonization goals. These proposals were on the ballot at a number of our financial holdings and we voted against them. Even with extremely aggressive energy transition timelines, oil and gas demand is expected to peak only in the 2030 to 2035 timeline and remain a meaningful part of the global energy mix for an extended period of time. As oil and gas production naturally declines at approximately 8% per annum, constant reinvestment is necessary to ensure supply meets demand. Any overly-hasty withdrawal of capital from the sector is likely to unduly restrict supply, adversely impact the global economy and therefore, potentially reduce the capital available for the energy transition. Additionally, blanket bans on financing certain industries could compromise a bank’s ability to serve as partners to their clients in achieving their energy transition goals.

We believe that in most cases, management teams at financial institutions are well-positioned to set an appropriate timeline to phase out fossil fuel financing in a way that does not threaten the stability of the global energy supply or the bank’s existing relationships.

SS&C Technologies: a leading American cloud-based provider of financial services technology solutions

Executive compensation is a common issue we are faced with during proxy season. Analysts are tasked with judging management pay levels and awards within the scope of company performance, balancing the need to attract and retain key talent without deteriorating shareholder value.

Institutional Shareholder Services (ISS), which we use as a third-party resource on proxy voting issues, flagged several components of SS&C’s advisory vote on executive compensation as potentially problematic. The matters of concern arose from a severance payout to a departing executive and relatively high compensation awards for both the COO and the Founder/CEO. Often, we find that the company-specific context is not well-understood by proxy advisors who have limited means of engaging with the companies they cover. This is a critical reason why we believe there is no substitute for the relationships we maintain with management teams.

After engaging with SS&C’s CEO, General Counsel, and an Independent Director, we learned that the flagged severance payout was a contractual obligation owed to the departing executive and was therefore improperly handled by ISS. On the issue of COO compensation, the team at SS&C provided us with their rationale for the outsized compensation award, citing his skillset and experience as attractive to many of their competitors who may seek to poach him and thus warranted additional incentives to retain his talents. Our engagements enabled us to feel at ease with the company’s decision-making on these components of the advisory vote.

Occasionally, however, the ISS flag may help draw our attention to problematic issues that we are subsequently able to explore in greater depth by engaging with the company. On the issue of CEO compensation, despite an increase in the performance-oriented component of equity, the compensation was excessive and was far outside the range of peers. Even after engagement, we remained convinced that the award was too high to offer our support. Extreme bonus payouts such as this are at the expense of shareholders and led us to vote against the advisory vote on compensation.

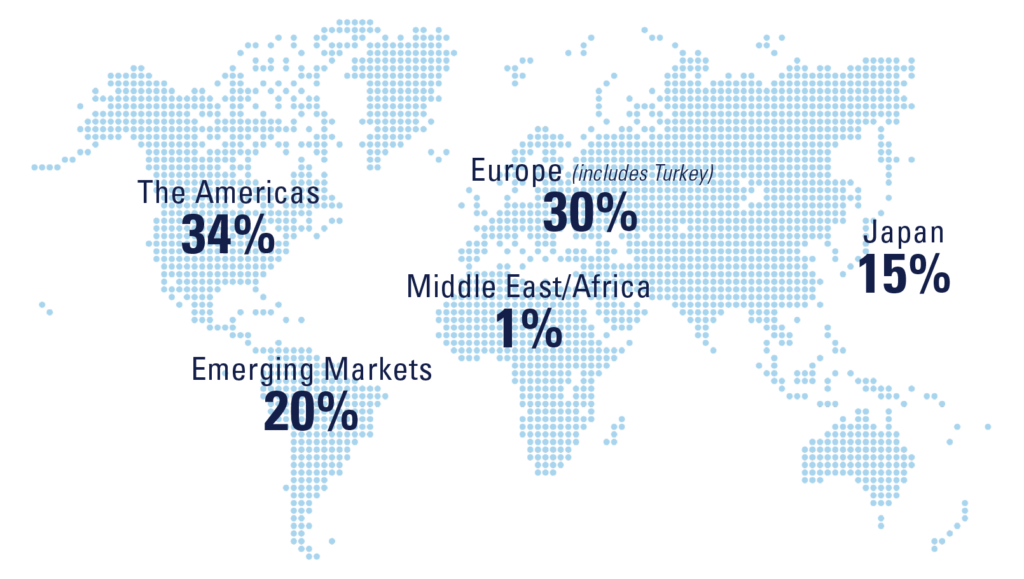

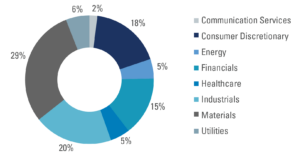

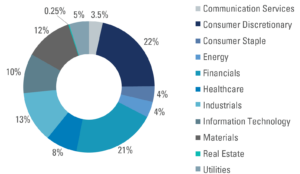

ENGAGEMENT BREAKDOWN 2022

Geographic location breakdown for 2022 engagements

based on company headquarters

Sector breakdown for Opportunity List engagements

Sector breakdown for 2022 engagements

ESG breakdown for Opportunity List engagements

higher than 100% due to some overlapping meetings

Further information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management, LLC (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Limited (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia. In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2023. All rights reserved.