2023 Stewardship Report

A MESSAGE FROM OUR CEO

This is now our second annual stewardship report where we highlight some of our stewardship activities from the prior calendar year. The philosophy underpinning our approach to stewardship has remained consistent year to year. As value managers, we look to improvement in business fundamentals as a source of excess return. We are therefore focused on the embedded investment opportunity, whether this may come from improvements in environmental, social or governance (ESG) issues or any other potential value driver.

Stewardship (through direct engagement and proxy voting) is one of the more effective tools that we have at our disposal to exert a constructive, long-term-oriented influence on the improvement trajectory of a company. We view stock ownership as an opportunity to help steer companies in the direction of creating long-term value for our clients, and therefore explicitly favor engagement over divestment.

We also believe that it is important to continue to refine the practical application of our stewardship philosophy. In 2023 we made two such enhancements to our approach:

- We started specifically tracking engagement outcomes and introduced a proprietary rating system for all companies on our Opportunity List. These changes are explained in further detail on page 4.

- We began piloting thematic engagements to complement our bottom-up research and engagement approach. This is because we see value in our ESG team exploring emerging and/or important thematic topics with companies to feed back into and enhance our bottom-up research. We profile a couple of examples of thematic engagement starting on page 7 of this report.

We hope this report continues to provide some insight into how we approach and continue to evolve our stewardship activities over time.

CAROLINE CAI

Chief Executive Officer and Portfolio Manager

Pzena Approach to Stewardship

At Pzena, our role as responsible stewards of capital has always been an integral part of our fiduciary responsibility to act in our clients’ best interests, maximizing long-term shareholder value.

As value investors, we often find ourselves in situations where something has gone wrong, and we rely on fundamental research to assess the likelihood of improvement on these issues. Taking advantage of the gap between a valuation that reflects near-term challenges compared to the value of the long-term earnings power of the company is the heart of our investment philosophy. In some cases, the issues or opportunities facing a company fall under the ESG umbrella.

Deep research and extensive engagement can help value investors capitalize on controversy and access this potential source of alpha, making engagement a cornerstone of our investment philosophy and a critical component of our process as long-term active investors.

As we do with all key investment issues, significant ESG considerations are analyzed internally, discussed with company management and industry experts, and monitored. Each step of this process contributes to the team’s determination of whether to invest and, if we do, at what position size. Once an investment has been made, we continue to engage management on an ongoing basis. Through these conversations, along with our proxy voting and other escalation options, we seek to exert influence in a constructive way, oriented toward the long-term success of the company.

ENGAGEMENT APPROACH

We engage with company management throughout our due diligence process, and extensively after an investment is made, on all material or potentially material investment issues. As shareholders, we believe we have the opportunity to help guide companies toward long-term value creation, and therefore prefer engagement over divestment.

If we determine an ESG consideration to be material to our investment thesis, we raise it with the management team. Each company and management team is unique. Consequently, our approach to management conversations is organic in each case; however, we always seek an open, cooperative dialogue. We prefer to maintain an ongoing dialogue with company management through regular meetings, in-person site visits, and calls. When we engage with companies, we are typically speaking to some combination of the following: senior management team, members of the board, ESG or sustainability lead, and investor relations.

Roles and Responsibilities

For ESG to be integrated into the research process, the industry analyst covering the stock must also lead the associated investment due diligence, of which engagement is a key part. The industry analysts are best placed to evaluate the investment implications of ESG issues, and therefore they bear primary responsibility for discussing these with company management. Our ESG analysts support the industry analysts in these conversations as needed, but we intentionally do not delegate these responsibilities to a separate stewardship team.

Engagement Purpose

Broadly speaking, our discussions with company management have the following purposes in mind:

- Testing assumptions — intended to deepen our understanding of issues that we have identified as material or potentially material to the investment. Sometimes we identify these issues at the point of investment and other times they arise during ownership. In both cases, we discuss the issues with management, solicit their input, assess their response, and evaluate the impact on our investment thesis. To the extent that the issues are ongoing, we continue to follow up until the issue is resolved or no longer relevant.

- Maintaining an informed dialogue — whereby we keep apprised of decisions relating to strategic and operational considerations. We routinely meet with management following earnings, strategic business updates, and management transitions.

- Advocacy — an explicit opportunity for us, as shareholders, to advocate for different decisions that we believe will enhance long-term shareholder value. With increasing regularity, companies also proactively seek our input on a range of issues.

The success of each engagement is measured on a case-by-case basis, depending on the company-specific context and goals of the engagement. Below are some examples of different engagements we have had with companies in 2023 with one or more of the above purposes in mind.

Examples of Engagement

General Electric (GE), US multinational industrial conglomerate

We have maintained a dialogue with GE management on the potential for the Power and Renewables division (GE Vernova), which has historically struggled to turn a profit. The renewables industry in general has been loss-making, as fixed-price contracts with long lead times quickly became uneconomic when input costs spiked in recent years amid the global inflationary environment.

From our more recent discussions, we believe GE is making material operational improvements and implementing better oversight. Though still in the red, GE’s renewables unit has been improving, with 27% organic sales growth and order intake at an all-time high, reflecting surging demand. Near-term cost pressures notwithstanding, this unit stands to benefit from long-term end market demand as governments incentivize wind power and technologies that enable the energy transition.

We will continue to monitor the performance of this business unit and discuss any questions or concerns with GE management because the business model still carries uncertainty. Beyond direct profitability concerns, the turnaround timeline of this business unit could impact the ability and timing for GE to complete its separation plan.

Cognizant, provider of IT, consulting and business process outsourcing services

Cognizant has underperformed leading IT Services peers for multiple years as execution issues resulted in subpar growth, margin contraction, and high employee turnover. We maintain a regular dialogue with the board and management to evaluate Cognizant’s turnaround plan, and we were encouraged by our recent engagement (Q4 2023) with the Chairman and other Board members. We believe the company has a thoughtful strategy in place, the recently refreshed Board is closely engaged, and the Governance practices appear well-aligned with the strategy.

The two key topics of engagement involved 1) the recently executed management change and 2) details around the Board’s plan to oversee and evaluate the turnaround. Regarding the CEO turnover, the prior CEO, who did not have a tech services background, made significant positive contributions enhancing Cognizant’s operational capabilities. However, some of these managerial changes negatively impacted employee morale and may not have been conducive to gaining commercial momentum. As such, the Board concluded that shareholders would be better served by attracting a new CEO with extensive IT Services experience who could help the company accelerate growth during the next phase of its turnaround. We appreciate both prior management’s contributions during a challenging period and the Board’s willingness to make difficult decisions to drive the best outcome for shareholders.

Regarding the current strategy, one component of accelerating growth is winning and successfully executing larger, longer-term client engagements, which Cognizant historically shied away from during prior periods of operational instability. We were pleased that the Board is focused on both the opportunities and, importantly, the risks inherent in this strategy. They are engaging closely with management on how to properly evaluate and manage these risks, measuring success with intelligent KPIs applied over multi-year timeframes, and properly aligning incentives with a robust executive compensation philosophy. Cognizant’s strong Governance may not guarantee a successful outcome, but we believe this function has improved over time and increases the odds of commercial success. We look forward to continuing our dialogue with Cognizant and monitoring the company’s progress.

Teijin, Japanese chemical, pharma and IT company

We have spent time engaging with the management team of Teijin on the auto composites business in the US, where labor productivity issues have led to substantial operating losses. Teijin’s could not deliver the volume of composites promised to the auto original equipment manufacturer (OEMs) with their full-time workforce. This led to the hiring of contract labor at 1.5 to 2 times the cost which was not easily passed on to the OEMs.

Management’s plan to restructure the business to improve profitability appears sensible but still carries execution risk. If none of the following proposed restructuring plans have the desired effect, management will consider exiting select US auto composite programs entirely:

- Working with the existing workforce to try and improve efficiency

- Investing in automation to shift more of the labor from humans to machines, but this still requires bringing engineers from Japan for one-off implementation and hiring skilled operators, which remains a work in progress

- Negotiating with auto OEMs to pass through labor cost inflation

In addition, Teijin is also removing layers of hierarchy to have business unit heads, such as the head of the US auto composite business, report directly to the CEO. We think that the new corporate structure may help to improve decision making. We will continue to monitor Teijin’s restructuring plan to assess its ongoing effectiveness.

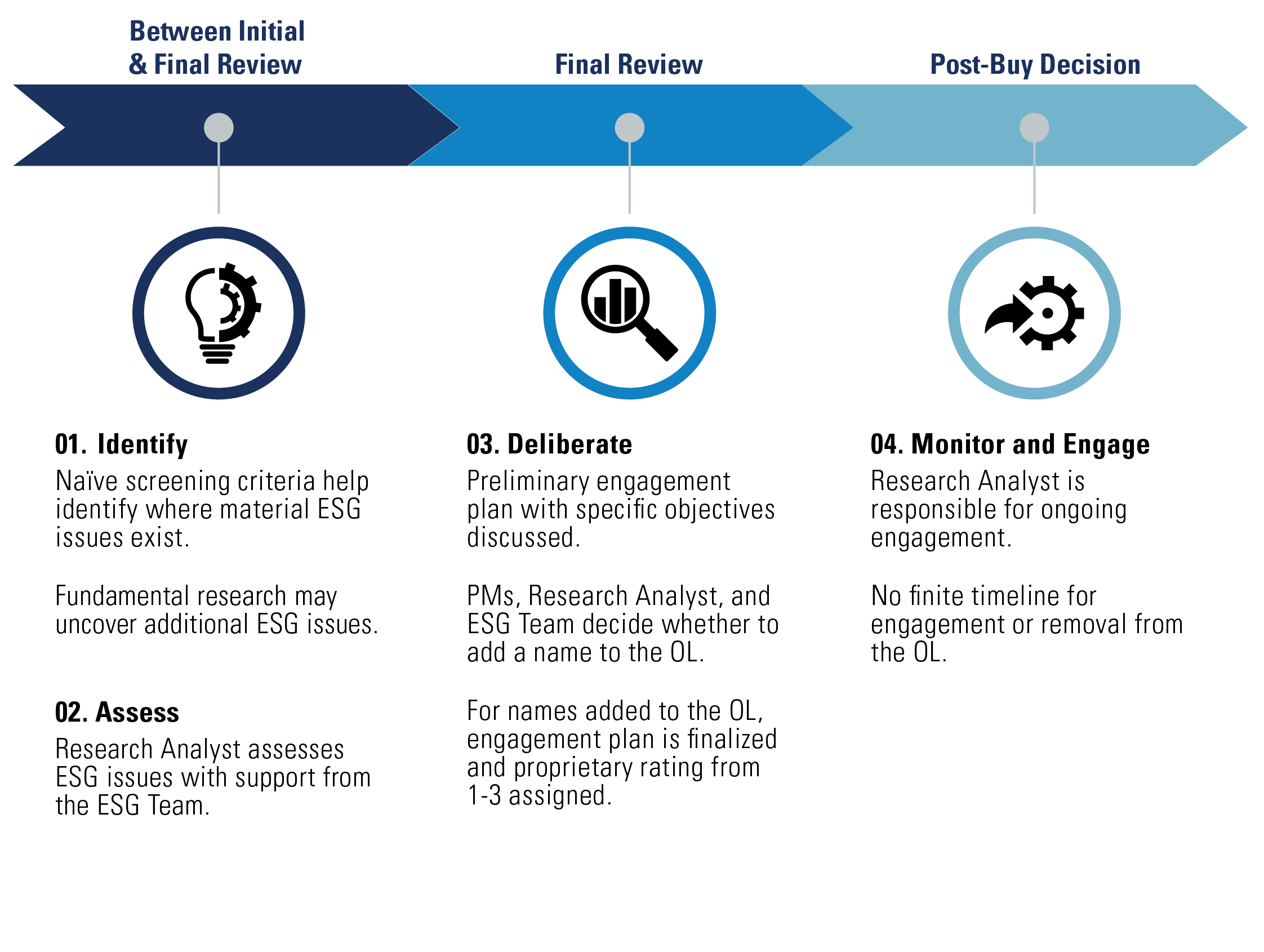

SPOTLIGHT: OPPORTUNITY LIST

The belief in our ability to push for better outcomes by engaging with the companies we own has been a driving force behind the development and application of the Pzena Opportunity List. The Opportunity List seeks to systematically identify opportunities in our portfolio where material ESG issues exist and engagement could have a positive impact. If we choose to add a company to the Opportunity List, it means there is significant room for improvement on material ESG considerations.

Once a company is placed on the Opportunity List, we create an engagement plan with specific objectives to track progress. In practice, progress against the engagement plan will not manifest all at once, but will appear in incremental steps over the investment time horizon. If we see a company is trending off-track, we have several options to escalate engagement, as laid out above. Persistent failures to address our concerns could lead to our reevaluation of the investment thesis and potential divestment.

In some cases, removal from the Opportunity List will come with the gradual resolution of the ESG issue(s) over time and/or only require discreet changes, such as the resolution of a pending litigation. In many cases, removal is more nuanced and requires continuous research, engagement, and monitoring. Regardless, all investments require us to be in dialogue with management and to respond to changes that may impact the range of investment outcomes.

In 2023 we made a couple of enhancements to our Opportunity List:

Proprietary ESG Ratings

We introduced a proprietary rating system for all companies on the Opportunity List. Companies are rated from 1 to 3 in accordance with our engagement objectives. A score of ‘1’ is for those companies that have made little to no progress on the objectives we have outlined and/or have not yet acknowledged the issues. A ‘3’ rating is for companies that are making substantial progress in addressing our objectives and/or are highly engaged in addressing the issues. This rating is determined when the engagement plan is created and is reviewed, at a minimum, every 6 months during our bi-annual Opportunity List review.

Companies that have been classified as a ‘3’ for 6 months or more may be – though not always – good candidates for potential removal from the Opportunity List. A company may be rated a ‘3’ but the issues the company is addressing may take years to resolve, such as capitalizing on opportunities in the energy transition. Conversely, a company may be rated a ‘3’ because the company is addressing a discreet issue, such as lack of a fully independent audit committee.

These ratings allow us to track the progress of names on the Opportunity List more explicitly over time. We can measure how long a company has remained at its rating and whether the company is making progress towards our objectives and over what time horizon. This also allows us to evaluate in a timely manner whether we need to escalate our engagement.

ESG Outcomes

We have also introduced more explicit documentation and tracking of engagement outcomes for names on the Opportunity List. At every 6-month Opportunity List check-in, the research team explicitly discusses whether there have been any notable outcomes related to engagements in the prior 6 months. We do not always expect outcomes, given that some issues take a while to resolve. Tracking outcomes, where they exist, allows us to judge the success of our engagements over time.

Opportunity List Engagement Examples

Edison International, regulated electric utility

Edison is on our Opportunity List due to its exposure to wildfire risk and we have maintained a dialogue on this issue throughout our ownership. Wildfires in California have become a chronic seasonal issue and led to large losses in 2017-2018 due to California’s inverse condemnation law. Since then, this risk has been mitigated by AB 1054 which capped wildfire losses and introduced a new prudency standard, as well as Edison’s own efforts to reduce wildfire risk through tree trimming, covering conductors and targeted shutoffs. Limited risks remain, as Edison is liable for up to one third of its rate base over a three-year period, if it is found to have acted imprudently by the regulators.

Most recently in Q3 2023, we met with the Edison CFO to discuss continued wildfire mitigation investments. Following that discussion, we believe Edison has met two out of our three engagement objectives.

- Monitor km of wires covered in line with approvals from the California Public Utilities Commission (CPUC). This objective has been met. Edison has continued to cover wires in alignment with approvals from CPUC and has approval for 4.5 thousand miles through the end of 2023. Edison can exceed this amount and still receive future payment from the state, assuming they are found to have acted prudently. Edison has already filed for further approvals beyond 2023.

- Continue to monitor 1.2k miles of annual covered conductor installations. We continue to monitor this objective but Edison appears to be tracking comfortably against it. After a debate earlier in 2023 about whether Edison’s covered conductor program or PG&E’s undergrounding program was best for reducing wildfire risk in a cost-effective manner, Edison moved forward with covered conductor spanning 5,000 miles in certain areas. The focus on covered conductors was determined by the risk drivers of certain areas, specifically vegetation like shrubs and chapparal. Edison will address different areas where undergrounding is the better choice in 2025.

- Track catastrophic wildfires (3 years of time without fire may warrant removal). This objective has been met. Using a 3rd party service Edison has assessed that catastrophic wildfire risk is down 85% vs. 2018 and power shutoffs are becoming a less important part of their toolkit (only 1 has been required this year). Investment in wildfire mitigation is beginning to wind down and in in the 2025 general rate case Edison will turn their focus to investing in the grid for decarbonization.

Given the significant progress against our engagement objectives, we have rated Edison a 3 on our proprietary rating system and consider it a candidate for removal from the Opportunity List at our next 6-month review (assuming the trajectory of progress is maintained).

Hon Hai, Taiwanese multinational electronics contract manufacturer

As we discussed in last year’s Stewardship Report, we made the decision to add Hon Hai to the Opportunity List given the escalating number of labor-related controversies at various Hon Hai facilities over the prior few years. Our engagement objective was to discuss remediation measures to help prevent Hon Hai ceding market share to competitors. We have had several conversations with Hon Hai about the steps it has been taking to raise its code of conduct to international best practices and hold those accountable who fail to maintain the standard. We were encouraged to see Hon Hai investing in third party audits at sites where there have been previous issues. Hon Hai is also taking steps to build a culture of transparency. For example, the Chairman has created a quarterly forum for employees to bring any concerns to his attention.

We set a minimum expectation of 1 year without any further labor-related incidents before we could consider removing Hon Hai from the Opportunity List. Given that this 1-year milestone has now been met, we decided to rate Hon Hai a 3 on our proprietary rating system. This makes Hon Hai a potential candidate for removal from the Opportunity List at the next 6-month review, assuming we continue to see progress.

Petrobras, state-owned Brazilian oil and gas company

We added Petrobras to our Opportunity List because of governance issues and embedded climate transition risk. Our specific engagement objectives are as follows:

- Monitor for any sign of detrimental changes to the import parity pricing formula

- Maintain full independence of the audit committee

- Evaluate expected forthcoming revisions to energy transition plan and overall capital plan under new company leadership

We have engaged several times on these issues in 2023, most recently with the CFO in Q2 2023. Overall, we feel relatively comfortable that the governance reforms instituted following the ‘Car Wash’ scandal will hold. The CFO reiterated the culture of compliance and that there is no desire under the new management team to roll back any of the protections. Any such roll back would also require changes to bylaws and new board elections and so would be very visible to shareholders should it ever occur. Specifically on the pricing policy, we learned that this would now be determined by the customer’s alternative supply price (which incorporates import pricing parity) and Petrobras’ marginal value. We view this as a positive as it gives the company more opportunity to gain share and maximize value and we were reassured that the company would not sell products at a loss, as had occurred 2010-2015.

On climate transition, the CFO outlined plans to increase capex 11% over a 5-year period to invest in energy transition opportunities, either in the form of organic investments or M&A, and specifically cited onshore wind farms in the northeast of Brazil as the most profitable investment area. This would still be below the 20% that on average European oil majors have invested, but we believe this lower percentage better reflects the current regulatory environment in Brazil. We were also encouraged to hear that any investments are predicated on finding opportunities with attractive returns.

We will continue to engage on these issues and will have to reassess the independence of the audit committee when those individuals are announced. We rated Petrobras a 2 on our proprietary rating scale, reflecting reasonable performance against our stated engagement objectives but it is still too early to assess the credibility.

NOV, provider of equipment, technologies and expertise to the upstream oil and gas industry

NOV was added to the Opportunity List because we observed that more could be done to enhance emissions disclosures and develop a differentiated energy transition strategy. Specifically, we had the following three engagement objectives:

- Disclose scope 1 and 2 emissions

- Set goals for mitigating the intensity of scope 1 and 2 emissions with appropriate timelines

- Continue to explore and refine the company’s energy transition strategy

We have had many engagements with the CEO and CFO of NOV on these topics over the past couple of years. While we appreciate that many other investors may also have advocated for similar things, NOV recently started disclosing its scope 1 and 2 emissions as a baseline for future target-setting. We consider this a significant engagement outcome and continue to discuss our two remaining objectives with NOV on a regular basis. NOV is rated a 2 on our proprietary rating system because there is still more work to be done to achieve our remaining engagement objectives.

TriMas, manufacturer of products for the consumer, aerospace and industrial markets

We originally had TriMas on our Opportunity List because it flagged as in the highest decile of carbon emissions intensity for its respective investment universe which, in theory, would indicate embedded climate transition risk. When we explored further, we discovered that MSCI (our provider of carbon emissions intensity information) was estimating this number for TriMas due to a lack of scope 1 and 2 emissions disclosure. It was our sense that TriMas would not actually be in the highest decile of carbon emissions intensity, but absent any actual disclosure from the company, we could not verify this.

We engaged with TriMas and encouraged them to invest in an emissions inventory so scope 1 and 2 emissions intensity could be directly disclosed. No doubt other investors were also engaging, and we were pleased to see TriMas eventually disclose a number that was approximately one third of the MSCI estimation (reflective of 2022 data). Once this happened, as we expected, TriMas dropped out of the 10th decile of carbon emissions intensity reported. At that point, we made the decision to remove TriMas from the Opportunity List, reflecting a lower actual exposure to climate transition risk.

Opportunity List

Our Opportunity List provides us with a structure to utilize fundamental research for assessing the likelihood of issue improvements.

THEMATIC ENGAGEMENTS

Biodiversity

Bayer, German multinational life sciences company

We identified biodiversity as an emerging issue in 2022 and started by developing a framework for how assess its financial materiality across our investments. This led us to differentiate between companies that in some way rely on biodiversity and those that impact biodiversity though their operations. Some companies are financially at risk because they are dependent on biodiversity and ecosystem services, while others are more at risk from a regulatory and reputational standpoint because of their high impact on biodiversity. Bayer is an example of a company in our portfolio that, to some extent, has exposure on both of those dimensions. In 2023 when we decided to research the issue of biodiversity more deeply, Bayer was a natural starting point. Thus far, we have approached the issue with Bayer from the perspective of what impact Bayer may be having on biodiversity, positive or negative.

Through the course of our conversations with Bayer, we started to develop a more detailed understanding of how this issue has the potential to be a business opportunity for the agricultural sector. Unlike carbon, biodiversity does not have one standard measurement, and may never given the complexity of the issue and interdependency with other issues such as climate change and water scarcity. Instead, we discussed the idea of an impact metric specific to the industry, productivity/acre. The logic being that the higher that percentage, the fewer resources are being consumed to grow crops for human needs.

This is clearly something that is still under some debate internally at Bayer but aligns with their strategic shift announced in June 2023 to pivot away from a volume-driven business in agriculture to one that is more outcome driven, focused on boosting yields and reducing resource footprint for farmers. Bayer is also putting this philosophy into practice with the launch of a new direct-seeded rice cultivation system which can reduce water usage by 40%, emissions by 45% and manual labor by 50%. Bayer is predicting that 75% of rice fields in India will adopt this method by 2040, up from 11% today. Given that it is estimated rice production consumes 43% of the world’s total irrigation water, this has the potential to significantly move the needle in terms of water conservation and efficiency.

Our key takeaway from this discussion was that it may be less helpful to continue to try and measure and financialize ‘biodiversity’, but instead focus on industry-specific metrics as well as the various other metrics that are in some way connected to the idea of biodiversity, such as reducing emissions and water use. This is very much aligned with the direction of the TNFD or Taskforce on Nature-Related Financial Disclosures, an industry-leading biodiversity disclosure framework.

Given the complexity of the issues and evolving regulation, we continue to engage with Bayer to both learn and determine whether we need to reassess the range of outcomes we expect for the investment going forward.

Freshwater Scarcity

TSMC, Taiwanese semiconductor manufacturing company

The issue of freshwater water scarcity is not necessarily a new issue, but the team chose to do a deeper dive into its financial materiality for our investments in 2023. We wanted to understand how exposed our portfolios could be to this risk and identify any higher risk companies. In our portfolio analysis, we found that Pzena portfolios held a lower exposure to water risk than the respective strategy benchmarks, but we also identified a couple of companies at potentially higher risk than others.

One of those higher risk companies was TSMC because the semiconductor industry is one of the more water intensive. The latest estimates suggest that on average, 8 gallons of water are required per wafer. We had raised this issue in the past with TSMC and had been told that it was not financially material but we wanted to do our own independent research to verify this.

What we learned through our research was that despite high exposure to water scarcity on paper, this issue was indeed not likely to become financially material to TSMC in the short to medium term. Some incremental capex and opex will be required to reach TSMC’s goal of net zero water; something in the range of low hundreds of millions to dollars per fab. In a scenario where this cost cannot be passed on to the consumer (which we view as unlikely), this would only be a 1-2% hit to TSMC earnings. In a worst-case scenario where TSMC runs out of water in its most water stressed operation in Arizona, TSMC would need approximately $5-10B in incremental capex to build the infrastructure required for a new site in a less water stressed area. We do not think this is a particularly realistic scenario in the short to medium term, particularly because of the political and economic incentives that exist to keep the Arizona plant operational.

Overall, our takeaway was that while there are costs associated with reducing water use, the profitability of the industry, and TSMC in particular, can support the necessary investments. We will continue to explore the issue of water scarcity if and when it becomes financially material for other investments.

Audit Committee Independence

Akbank, one of the largest Turkish banks

We identified the independence of the audit committee as an important thematic focus based on our survey of the academic literature on governance standards. The academic literature suggests that the independence of the audit committee had the strongest correlation to company performance of all standard governance metrics. This makes sense given that company performance is directly tied back to company financials, the direct purview of the audit committee. It is the role of the audit committee to provide objective oversight of company financials and the financial auditor. If the audit committee is fully independent, it is logical that they will be better able to fulfil their intended function, specifically providing: an objective check-and-balance, overseeing and as-needed taking a critical look at the decisions of management and the opinion of the external auditor; and transparency and trust in the company’s financial reporting and audit process.

Based on this research, we added Akbank to the Opportunity List, with the objective of encouraging a fully independent audit committee. We have engaged directly with the CEO, CFO and IR on multiple occasions to express our preference for the former Head of Internal Audit to be removed from the audit committee. We believe his prior role presents a conflict of interest and prevents him from exercising fully independent oversight. We also discussed our intention to use our proxy vote accordingly. While management has appeared open to the feedback, we decided to rate Akbank a 1 on our proprietary rating system to reflect the lack of progress to date in replacing this audit committee member. We will continue to engage on this matter and will escalate our engagement as needed.

ADDITIONAL ENGAGEMENT TACTICS

Engagement Escalation

In instances where we feel that our concerns have not been adequately addressed during our routine engagement with management teams, we may consider the following actions to escalate our concerns:

- A private meeting with the chairman or other board members

- A written letter to members of the senior management team and/or board members

- Voting against members of the board or resolutions at annual general meetings

- Divestment if the lack of progress changes our view of the investment embedded risk-reward

Collaborative Engagement

While we typically prefer to engage directly with the companies we own, occasionally we recognize the potential benefits of collaborative engagement with other investors. In such cases, we may seek to work with other investors, but only when we believe it’s in our clients’ best interests and permissible under applicable laws and regulations.

Situations where we have found collaborative engagement helpful include, but are not limited to, advancing a shared agenda with clients for a particular portfolio company and/or working with other investors to share insights on a particular issue. For example, we spoke to various other investors and stakeholders as we were deciding how to approach a corporate governance issue at Danieli Group, an Italian supplier of equipment and plants to the metal industry. These discussions were an opportunity to share our views with other investors and amplify our message to Danieli through those who were like-minded.

There are also aspects of collaborative engagement efforts that are less well-aligned with our approach and investment philosophy. Firstly, we do not seek to become activists or insiders, nor do we encourage proxy battles. Instead. we prefer to maintain a constructive dialogue with management teams and work collaboratively to achieve the desired outcome.

Secondly, company-specific bottom-up ESG-integrated investment analysis is core to our investment philosophy and approach to stewardship. This naturally lends itself to a more company-specific approach to engagement. The perspective we want to bring to management teams is often more nuanced than some collaborative organizations allow. As such, we have not necessarily found collaborative engagement initiatives particularly helpful to advance our agenda with company management. If we were applying ESG themes top-down, it might make more sense to team up with other investors focusing on the same ESG theme. We also find we maintain good access to management teams through our concentrated portfolios and so have not needed to leverage these collaborative groups for the purpose of seeking an audience with management teams.

That said, we do periodically consider membership in some of these collaborative organizations and remain open to evolving our approach. Our ESG team has evaluated Climate Action 100+, the IIGCC, Ceres, and CII for potential membership. While we have no plans to join any of them at present, we keep them on our radar and remain open to joining any of them in the future. Our ESG team also spends significant time engaging with the ESG community through panels and other means. As members of the Principles for Responsible Investment (PRI), International Financial Reporting Standards (IFRS), and the Net Zero Asset Management initiative (NZAMi), we frequently attend convenings with other members. The PRI has also launched a collaborative engagement portal which we will continue to monitor.

PROXY VOTING

Proxy voting is a critical component of our engagement efforts and ability to drive change. As such, we take our responsibilities as stewards of our clients’ capital seriously, actively voting the shares of companies in which we invest on their behalf as an integrated part of our investment process. Each proxy is voted in the best interest of our clients. We exercise proxy voting to highlight our views on management decisions, including ESG-related items, regardless of whether we agree with management’s recommendation. We evaluate each proxy item for any investment on its own merit and therefore vote on a case-by-case basis, informed by our PROXY VOTING POLICY.

By way of resources, Institutional Shareholder Services (ISS), provides us with a proxy analysis with supporting research and a vote recommendation for each shareholder meeting. Nevertheless, we retain ultimate responsibility for instructing ISS how to vote proxies on behalf of each individual proxy item for each company. We evaluate each proxy item for any investment on its own merit and therefore vote on a case-by-case basis.

We disclose our proxy voting records publicly, and they can be found AT THIS LINK.

Roles & Responsibilities

Each proxy is reviewed and voted by the industry analyst covering the stock. We intentionally do not outsource this responsibility to a separate stewardship team, as we consider it a fundamental part of our investment due diligence and engagement.

The ESG team assists the industry analyst in making a vote determination, primarily on ESG items where either the specific issue falls outside of the scope of our policy or the industry analyst thinks it would be helpful to seek additional guidance.

Our Director of Research is responsible for monitoring analyst compliance with voting procedures.

Significant Proxy Examples

Duerr, German industrial equipment and engineering and construction company

Repricing any aspect of an executive compensation plan mid-cycle falls afoul of our philosophy on executive compensation. Such adjustments are typically made to insulate management from a negative event or further capitalize on a positive event. Either defeats the purpose of the fundamental pay-for-performance principle that should underscore all compensation packages. That is why we decided to vote against the pay package for the CEO of Duerr.

Duerr changed the short-term incentive (STI) target—100% EBIT margin based—in the CEO’s pay package retrospectively to insulate the ultimate payout from negative events, specifically the ongoing China shutdown and Ukraine war. The change resulted in payouts above the target of 110%, equating to approximately EUR1M rather than the EUR600k that would have been paid out if the goalposts had not been moved.

Enel, diversified Italian utility

As long-term shareholders, one of the more important votes we cast for companies every year is for the individual directors that comprise the board of directors. The role of the board is to oversee the strategic decisions of the management team, ideally with long-term shareholder value creation in mind. This is why we voted for the slate of directors at Enel proposed by activist Covalis Capital. The slate proposed by Covalis would have meant a majority independent board and independent Chairman, which, in our view, would have best represented the interests of non-government shareholders who still own the majority of shares outstanding. The other options were the Italian government’s slate (the government owns ~24% of shares outstanding) and a slate proposed by the Assogestioni, an association of Italian asset managers.

The backdrop to this vote was the decision earlier in the year, under pressure from the Italian government, to replace the former CEO, Francesco Starace. We were supportive of the business strategy pursued under Starace’s leadership. Absent a credible reason for the government’s loss of confidence in Starace, we generally view leadership transitions under such circumstances as potentially value destructive. The influence that the Italian government maintains over decision-making at Enel—without a controlling stake—provided further justification to back the slate of independent directors proposed by Covalis.

Unfortunately, the activists’ slate received less than 10% of the vote, while the government slate received 49% and the association’s slate received 43%, resulting in six government nominees and three association nominees being named to the nine-person board. Nevertheless, we will continue to engage the new management team to ensure that there is business continuity, particularly with respect to Enel’s transition plan, which we have long viewed as industry-leading, and the prudent use of capital.

Dow, multinational commodity chemical producer

One of the key environmental issues facing the chemicals sector is exposure to revenue generated from plastic products, particularly single-use plastic. The financial materiality of this issue is largely driven by regulation seeking to ban plastic products with limited recyclability and/or regulation that encourages “circularity” (i.e., a system where plastic materials are reduced, redesigned, and reused or recycled to recapture any “waste” as a resource for new plastic materials). A truly circular economy would result in a reduction in virgin plastic demand, which would be an adverse outcome for virgin plastic producers such as Dow.

Given the materiality of this issue, it is perhaps not surprising that a shareholder put forward a proposal for Dow to commission an audited report on the business impact from reduced plastics demand. The proposal made specific reference to one particular scenario—System Change Scenario—put forward in a report by The Pew Charitable Trust. While we agree with the materiality of this issue, we decided to vote against the proposal for two considered reasons:

- Dow is already adopting principles of circularity. For example, Dow has committed to making 100% of products reusable or recyclable by 2035, commercializing three million tons of circular and renewable solutions annually, and has entered into various joint ventures to develop circular plastics.

- We viewed the proposal itself as overly specific and narrowly deterministic in nature, such that the demands were a poor use of management time and resources. The specific scenario put forward by the proponent is highly theoretical, hypothetical, and, in our view, unlikely to materialize as stated. Many of the assumed interventions in the plastic value chain have no basis in existing or proposed regulation. Even if all plastics bans currently under consideration came into effect, the estimated result would affect less than 2% of Dow’s total sales based on 2022 revenue.

While we voted against this specific proposal, we continue to engage Dow management on this topic as part of our Opportunity List. Our ongoing research and engagement is focused on better understanding the evolving regulatory environment, determining which products may move in and out of the scope of single-use plastic regulation, and advocating for greater clarity on the associated capex and opex required to develop a more circular plastics business.

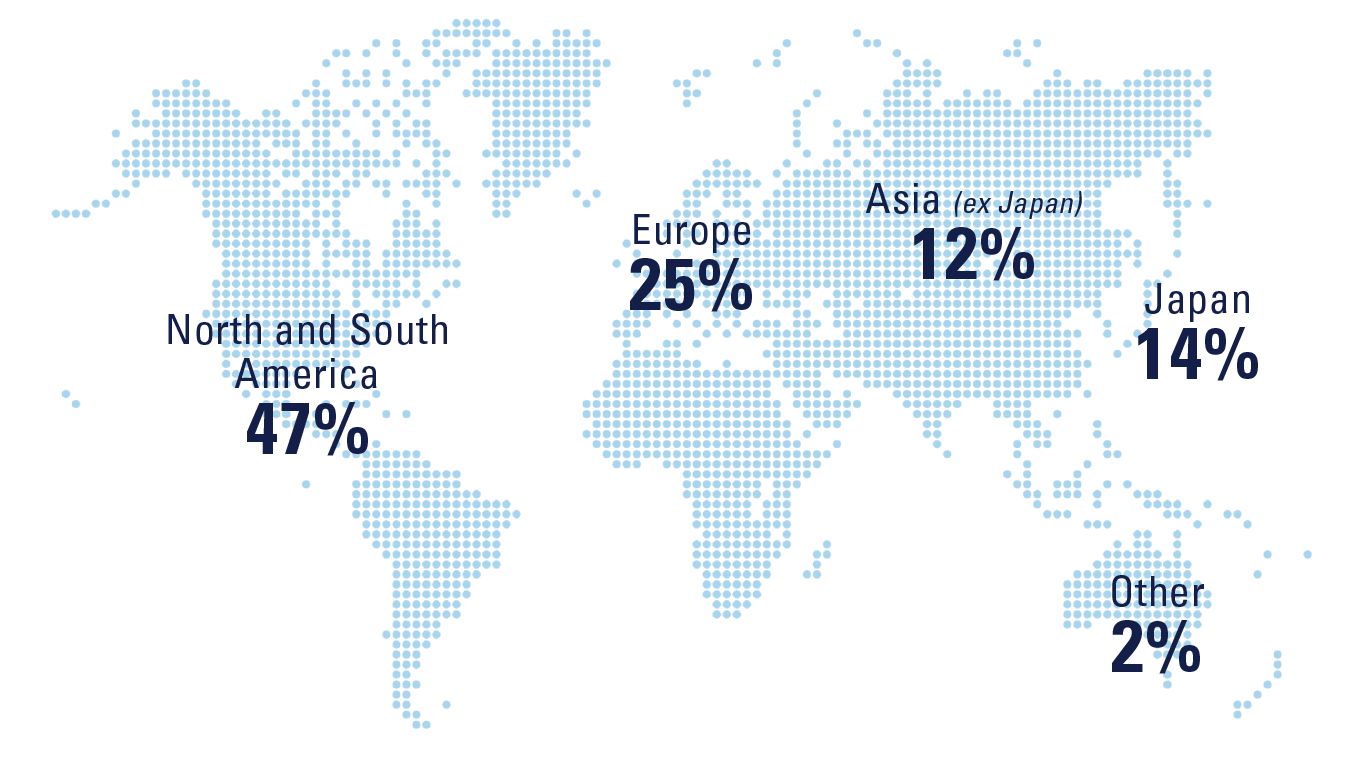

ENGAGEMENT BREAKDOWN

Geographic location breakdown for all engagements in 2023

location is based on the where the headquarters of the company are

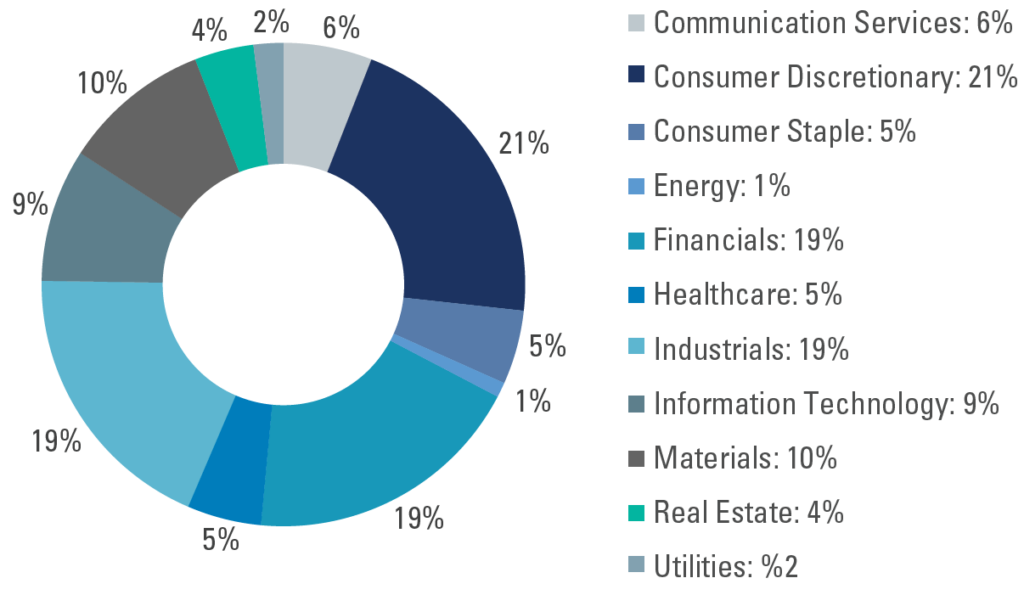

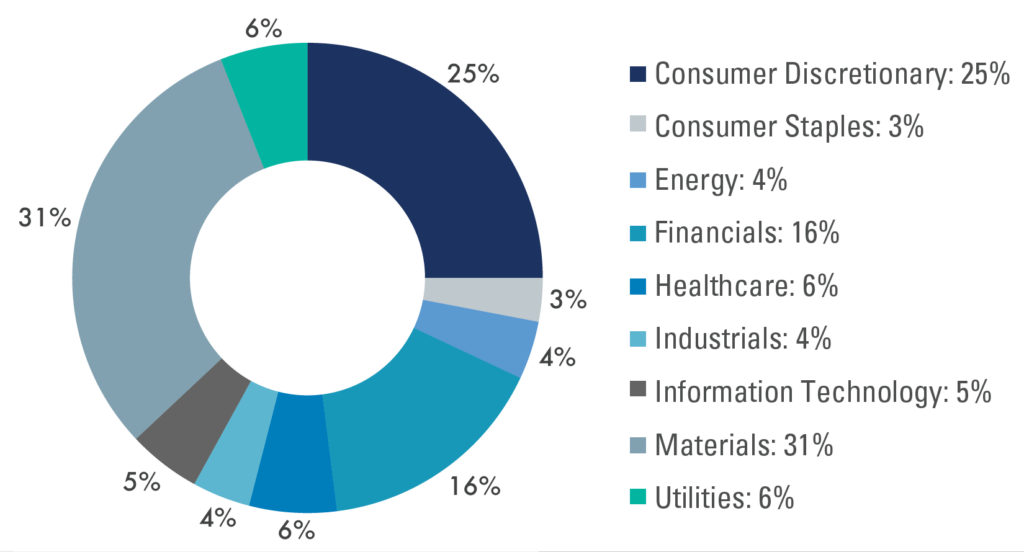

Sector breakdown for all engagements in 2023

Sector breakdown for all Opportunity List engagements in 2023

E, S & G breakdown of Opportunity List engagements

overlap due to multiple topic meetings

Further information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management, LLC (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Limited (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2024. All rights reserved.