Q1 2023 – Emerging Markets Quarterly Update

Principal and Portfolio Manager Rakesh Bordia provides an update on the first quarter for our Emerging Markets strategies.

Overview

Emerging market bourses were relatively unscathed by concerns over global banking weakness, benefiting instead from China’s reopening and an improvement in semiconductor supply chains (SE Asia is the world’s major chip hub). Similar to European banks and GSIFIs, most EM banks’ securities books are marked to market, so there are no hidden capital holes like at SVB. What’s more, our EMFV banks are mostly industry leaders that benefit from deposit flights to safety; and in general, most EM bank management teams are used to dealing with high and volatile interest rates, so their investment books are managed accordingly.

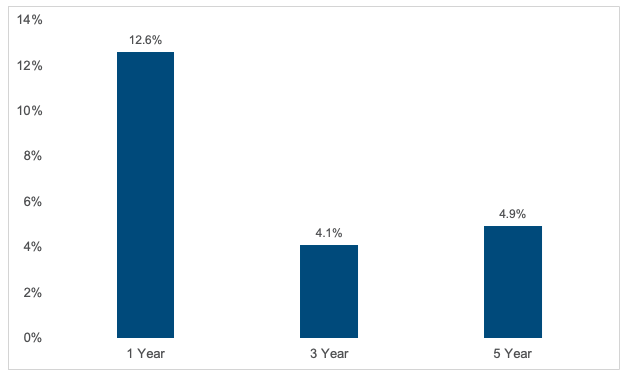

After a nearly 2-year steady decline driven mostly by Chinese economic malaise, we are starting to see EM stocks regain market leadership, which is what we would expect following a period of especially painful performance.

Average Annualized Alpha of EM Countries Following Steep 12 Month Underperformance¹

Attribution

Our Emerging Markets portfolio closed the quarter solidly in the black, outperforming both the broad MSCI EM Index as well as the value series².

Largest Sector Contributions (absolute)

- Information Technology

- Consumer Discretionary

Largest Individual Contributors (absolute)

- Korean steel producer POSCO Holdings

- Chinese PC-maker Lenovo Group

- Taiwanese chipmaker TSMC

Largest Sector Detractors (absolute)

- Real Estate

- Energy

Largest Individual Detractors (absolute)

- S. African energy & chemicals company Sasol

- Chinese real estate company COLI

- Indian vehicle financing company Shriram Finance

Notable Adds

We added Weichai Power Co., which is China’s leading diesel engine OEM, with a dominant position in heavy-duty trucks with economies of scale, best-in-class technology, and proven pricing power. The Brazilian market weakness and concerns over the new government provided us the opportunity to buy some of the industry leaders in Brazil at attractive valuations, including one of the largest Brazilian banks Banco do Brasil, and Brazilian energy company Petroleo Brasileiro.

Notable Sales

We sold out of Korea Shipbuilding and Offshore Engineering, despite a fairly attractive valuation, as we lost confidence in the company’s long-term capital allocation strategy. At a high level, KSOE’s management planned to IPO a few of its subsidiaries and use the proceeds to make investments in green energy, but wouldn’t provide specifics on said investments. Because we couldn’t determine whether the company would participate in value-destructive M&A, we elected to exit our position.

Outlook

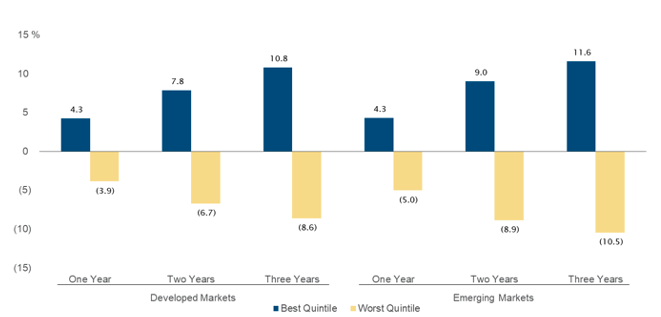

Ongoing macro and geopolitical concerns, turmoil in the banking sector, and volatility in both the US dollar and interest rates kept the market on edge throughout the quarter. We believe controversy and fear can create opportunities for value investors – especially in developing markets where price dislocations are often magnified – and we continue to be very excited by the cheap company valuations against their fundamentals in emerging markets.

Developed³ and Emerging Markets4 Relative Returns to the Best and Worst Quintiles of Valuation5 Measured over One- to Three-Year Holding Periods6

¹Source: MSCI, Pzena analysis. We looked at significant emerging market country declines, defined as 2,000 basis points or more of underperformance versus the MSCI Emerging Markets Index over the prior 12 months, and then looked at how those countries performed over the next one, three, and five years. The data set is from January 1, 1992 through December 31, 2021 and includes 10 different countries (some did not have data for the full period). The 10 countries chosen were the 10 largest weightings held in the MSCI Emerging Markets Index (as of December 31, 2021) that have at least a 10-year MSCI track record. Data in US dollars.

²Past performance is not indicative of future returns. Past performance is not indicative of future results. Returns could be impacted, positively or negatively, by currency fluctuations, where applicable.

3Proxy for MSCI World universe.

4Proxy for MSCI Emerging Markets universe.

5Developed market returns are USD-hedged from 1987. USD returns for emerging markets from 1992; equal-weighted data.

6Source: Empirical Research Partners. Based on Empirical Research Partners multi-factor model. Best and Worst Quintiles are derived using a combination of valuation factors. Data through March 31, 2023. Does not represent any specific Pzena product or service. Past performance is not indicative of future returns.

FURTHER INFORMATION

This recording is for institutional investors, and in the UK for professional investors and eligible counterparties only. Any views and statements expressed in this recording are those of Pzena Investment Management, are based on internal research, and are subject to change. It does not constitute investment advice. Your capital is at risk and past performance is not an indicator of future performance.

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. Neither the speaker nor PIM undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

The specific portfolio securities discussed in this document were selected for inclusion based on their ability to help you better understand our investment process. They do not represent all of the securities purchased or sold during the quarter, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell securities. Holdings vary among client accounts as a result of different product strategies having been selected thereby. Holdings also may vary among client accounts as a result of opening dates, cash flows, tax strategies, etc. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

This recording does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM, the speaker, or any other person does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

For UK Investors Only: This marketing communication is issued by Pzena Investment Management, Limited (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Mirabella Advisers LLP, which is authorised and regulated by the Financial Conduct Authority. The Pzena documents are only made available to professional clients and eligible counterparties as defined by the FCA. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For EU Investors: This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland.

For Australia and New Zealand Investors Only: This recording has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“PIM”). PIM is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. PIM is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. PIM offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This recording is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia. In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This recording is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only: Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South Africa Investors Only: Pzena Investment Management LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).