Finding Value in ESG (2Q 2023)

8 min read

ESG ratings can be useful in identifying leaders and laggards based on ESG fundamentals. They may provide an additional service by forcing companies with the worst ESG credentials to recognize and remediate their ESG shortcomings. We believe this improvement may relate positively to stock price performance.

At Pzena, integration of ESG into the investment process means focusing on the financially material ESG issues that influence the investment case and, through their remediation, could be reflected in better stock price outcomes. As fundamental investors, we rely on various sources of information to inform our decisions about the companies in which we invest. This includes third-party ESG scores despite their notable shortcomings, such as consideration of issues we believe may be immaterial to company performance. Nevertheless, ESG scores can be a helpful proxy in determining relative ESG performance. Our preliminary empirical research has revealed a possible link between ESG score improvement and better company performance (see ESG Scores whitepaper). This research has contributed to our emphasis on engagement with companies we own to achieve these better outcomes (see Opportunity List piece), while always maintaining focus on our fiduciary duty of maximizing long-term risk-adjusted returns.

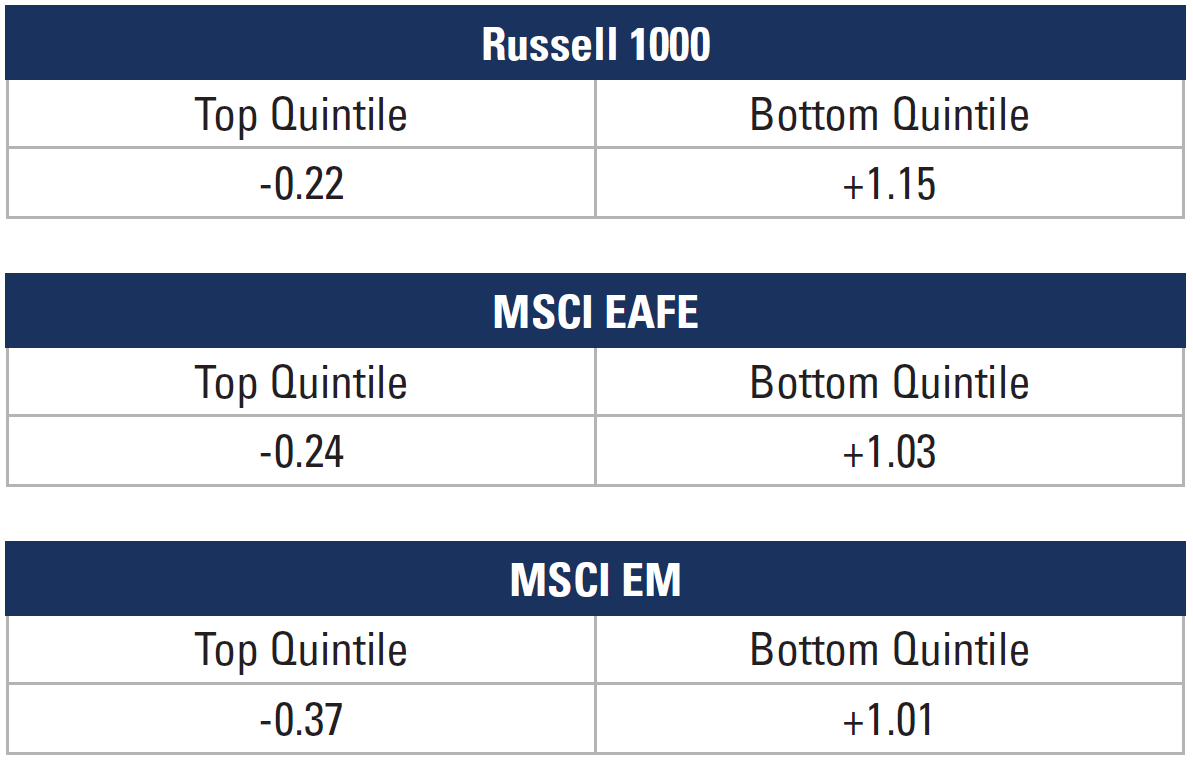

As a supplement to our initial research linking performance with ESG improvement, we theorized that the most significant laggards might recognize the need to improve their ESG standing more so than ESG leaders and, therefore, take corrective action. This could benefit not only the companies themselves, but their broader stakeholders as well. To test this, we looked at the three-year ESG score change of companies in the top quintile and bottom quintile of ESG score performance. To avoid unfair comparisons as a result of differences in industry structures, the analysis was undertaken on a sector-neutral basis.

Our observations for the three-year forward score change rolling monthly (2014–2019) were as follows:

Change in ESG score – 3-year Average1

¹ Based on MSCI’s Industry Adjusted Scores

Source: MSCI, Pzena Analysis, FactSet

Data table displays forward 3-year rolling monthly averages from December 31, 2013 – December 31, 2019.

Past performance is not indicative of future returns

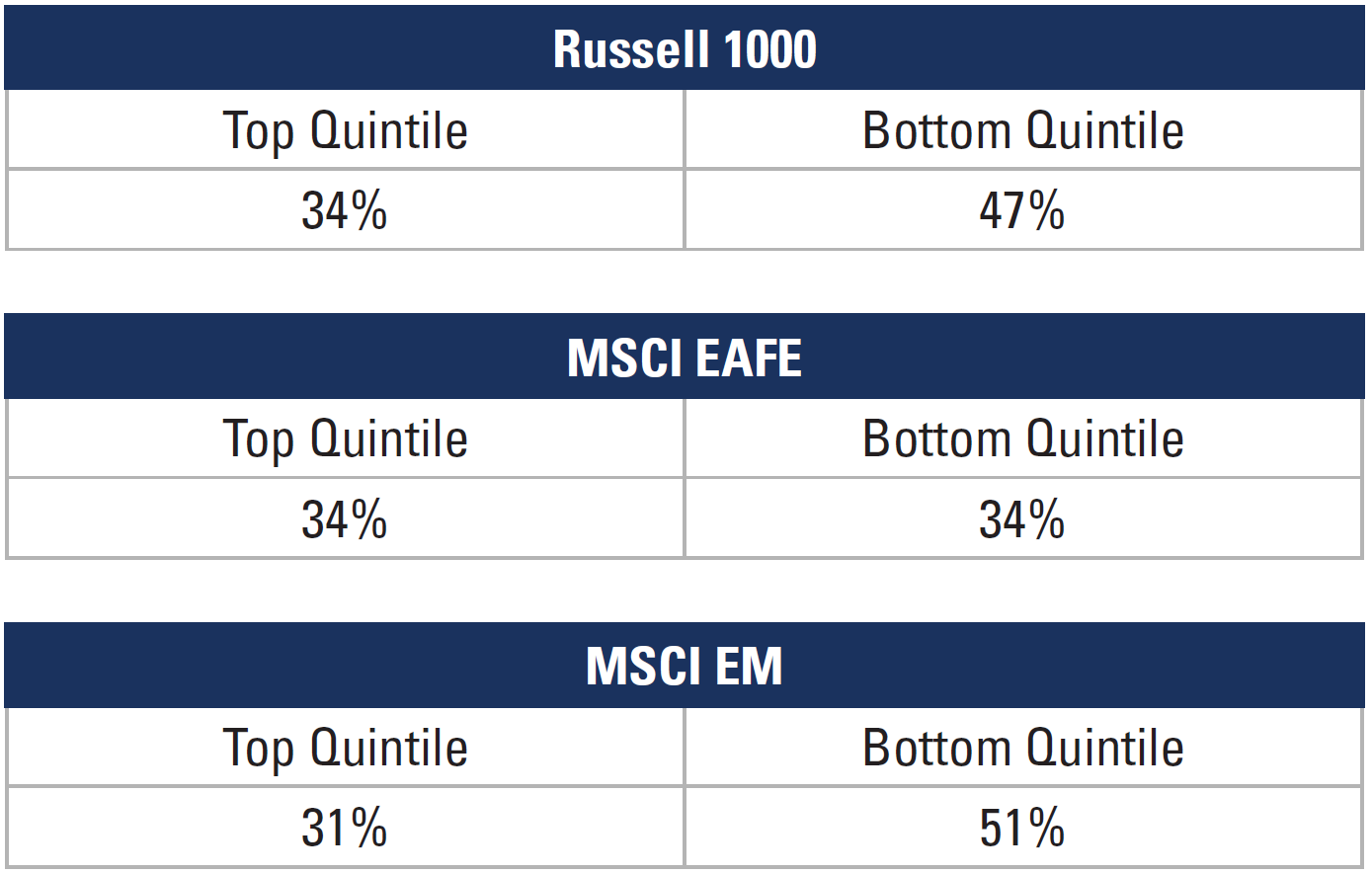

Change in Score Quintile – Percentage of Companies²

² Percentage of companies that moved our of the relevant quintile based on 3-year forward ESG score.

Source: MSCI, Pzena Analysis, FactSet

Data table displays forward 3-year rolling monthly averages from December 31, 2013 – December 31, 2019.

Past performance is not indicative of future returns.

Our results show that, on average and regardless of geography, roughly two-thirds of top quintile ESG performers remain in the top cohort. This indicates a tendency for these companies to maintain their status as ESG leaders. In contrast, the bottom quintile demonstrates much more variance across geographies.

In the US and emerging markets, there was a noticeable churn in the bottom-scoring quintile of companies on a three-year forward basis. Roughly 50% of companies, on average, improved their scores on a sector-relative basis and moved out of the bottom quintile. However, in EAFE, the results were much lower, with only 34% improving over the same period.

From both analyses, we can see that top-quintile ESG scorers remain best-in-class relative to their peers, despite a slight negative trend in overall ESG scores. Meanwhile, the biggest laggards across all markets see more significant absolute score improvement but show less progress in graduating from the bottom quintile. The performance advantage we have observed for companies that improve their ESG scores may be a result of the market rewarding these companies accordingly.

As fundamental investors, we pride ourselves on our deep understanding of the companies in which we invest and the underlying factors that drive their performance. We use multiple sources of information, including ESG scores, to inform our understanding while recognizing there are flaws in how these scores are currently assessed and rated. However, our research indicates that ESG scores can play an important role in driving engagement. They help identify areas for improvement in ESG laggards and allow the market to pressure these companies to improve.

The ability to distinguish leaders from laggards may encourage a more focused effort to improve material ESG issues within companies lagging behind their closest peers. As active investors, we believe we have a role to play in this identification process. We aim to extract value while the necessary improvement takes shape.

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management

(“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in

Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Mirabella Advisers LLP, which is authorised and regulated by the Financial Conduct Authority. The Pzena documents are only made available to professional clients and eligible counterparties as defined by the FCA. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority

(licence nr: 49029).

© Pzena Investment Management, LLC, 2023. All rights reserved.