Managing Climate Risk as a Value Manager

Updated May 2025

Approaching climate risks and opportunities in portfolio construction

Managing Climate Risk as a Value Manager

Pzena Investment Management applies a classic value approach to investing. Our approach is based on a bottom-up, research-driven stock selection process that fully integrates ESG considerations, requiring a focus on the long-term sustainability of business models.

When thinking about business longevity, climate change risks and opportunities are increasingly fundamental considerations. As a long-term ESG-integrated investor, we believe we have a role to play in allocating capital efficiently to both address financially material climate risks and capitalize on business opportunities in the energy transition over time.

Climate change poses risks to many industries that must undergo costly transitions to pivot legacy business models (e.g., oil & gas, auto) toward activities that facilitate the energy transition (e.g., green hydrogen, carbon capture and storage). The financial implications of these decisions can be significant, affecting a company’s future revenues, costs, expenditures, assets, and liabilities. It is therefore critically important that we assess, mitigate, manage, and monitor climate risks and opportunities specific to each individual investment.

When we uncover an undervalued company facing these challenges, its path toward long-term profitability quite often involves decisions that will improve its impact on the environment. For most companies, this typically involves a plan to reach net zero. The specifics of how and when net zero will be reached depends on the individual company situation. Our research and advocacy with companies in which we invest will therefore always be case-by-case.

As the quality of climate-related data is still improving, so too is the relevance and value of disclosure. Consequently, we believe our bottom-up, ESG-integrated company research provides better insight into specific developments at the business level than a top-down, scores-based system. Engagement with companies to improve business resilience and practices can be more effective in accelerating decarbonization efforts and driving change than an exclusionary approach based on third-party data.

Here we lay out our approach to managing climate change risks and opportunities in our portfolios, in line with the industry-leading Taskforce on Climate-Related Financial Disclosures (TCFD) disclosure framework. What follows is a detailed look at how the different aspects of our business come together to oversee and manage our clients’ exposure to climate change-related risks and opportunities.

1. GOVERNANCE

Organizational oversight of our ESG approach and policy is the responsibility of our Executive Committee, with input from our ESG Steering and Operating Committees. As an investment management firm, the most material way in which climate change risks and opportunities present themselves is through our investment portfolios, rather than through the day-to-day operations of our firm.

The entire investment team is responsible for the governance of climate change risks and opportunities within the portfolios. Our co-CIOs formulate an investment-specific ESG approach and set of policies, ensuring consistency and integration with our value investment philosophy and process. Our research analysts thoroughly evaluate and financialize any material issue relevant to a company, including where climate change is relevant to a given investment. Our ESG team and portfolio managers work with the research analysts, ensuring consistency in methodology. This dovetails into our bottom-up approach to investment analysis, placing the responsibility for managing material investment issues in the hands of those most closely connected to the relevant information. Portfolio construction decisions ultimately incorporate all of the above.

In addition, we have set up several internal ESG governance structures that have proven helpful in managing climate change risks and opportunities:

- The ESG Steering Committee is comprised of members of the Research department, specifically a sub-set of portfolio managers and the ESG team. The committee meets quarterly to guide priorities at the intersection of ESG and research. The ESG Steering Committee’s responsibilities include determining quarterly thematic ESG research and setting external facing priorities, such as publications, interviews, and conference attendance.

- The ESG Operating Committee is a cross-functional group of representatives from our Research, Client Services, Legal, Compliance, and Operations departments. The ESG Operating Committee meets annually or as needed to oversee the day-to-day operations of Pzena’s ESG efforts. Responsibilities include overseeing ESG reporting initiatives, monitoring evolving ESG regulations, evaluating membership in third-party ESG organizations, and other firm-level ESG initiatives.

- The Proxy Voting Committee, comprised of members of our Research, Operations, Legal, and Compliance departments,

is responsible for overseeing our approach to proxy voting. In 2021, this committee recommended additional guidelines for

our proxy voting policy related to climate and other ESG-related disclosure. Increasingly robust climate-related disclosure is needed to help investors assess and quantify related risks and opportunities. To ensure full transparency, the committee also recommended publishing proxy votes on our website.

Given that climate change is not a static issue, we are constantly evolving and updating our approach to managing it. Current areas of focus include::

- Concentrating our climate change-related engagement efforts on the companies with the highest 10% of carbon emissions intensity (scope 1+2 emissions/$M sales) as determined by investment universe. Companies that fall into this designation are usually added to our ESG Opportunity List. The Opportunity List seeks to systematically identify opportunities in the portfolio where material ESG issues exist and engagement could have a positive impact, improving financial outcomes for investors.

- Providing clients with more detailed insights into climate-related exposure in their investment portfolios.

- Identifying additional external data sources to supplement our own research and analysis.

Opportunity List Process

2. STRATEGY

We believe climate change has the potential to cause significant disruption to the operations and franchise longevity of many businesses. This disruption can be highly material to earnings over varying timeframes and can play out through higher levels of operating and capital expenditures, as well as elevated risk of stranded assets. Disruption also brings opportunities, and we see evidence of companies capitalizing on areas of competitive strength to meet the needs of the energy transition.

Given the magnitude of transition that is underway and the range of potential outcomes for industries and individual companies, analyzing the impacts of climate change is necessary to make informed investment decisions and have a productive dialogue with management teams about any associated risks and/or opportunities.

Investment Strategy

As value managers, we seek to underpay for companies relative to their expected long-term earnings potential. We analyze material risks and opportunities and incorporate them into our decision-making for every investment. Consequently, understanding climate risks and opportunities, as long-term drivers of business outcomes, is central to our investment philosophy; they are analyzed and priced in to help inform our investment thesis, just like any other issue. As a result, we may choose not to invest in a company if we think exposure to climate-related risks will impair future earnings and the valuation does not reflect the potential impairment. Alternatively, we might invest in a company with a higher-than-average carbon footprint if we see potential for it to manage the energy transition effectively and the valuation does not reflect the improvement potential.

With regard to climate change, investment considerations may include, but are not limited to the following:

- Transition risk, such as the stranding of non-useful assets and levying of a price on carbon emissions

- Opportunities arising from the energy transition, including technological innovation and new business growth opportunities across sectors

- Direct climate risk caused by the physical impacts of climate change, such as the increased severity of hurricanes or frequency of wildfires

- Indirect climate risk caused by the physical effects of climate change, such as disruption of a company’s suppliers or customer-base

When evaluating individual holdings, we use a range of forward-looking scenarios at the company and industry level to determine the impact on company profitability. These scenarios may include—but are not limited to—those published by the Intergovernmental Panel on Climate Change (IPCC).

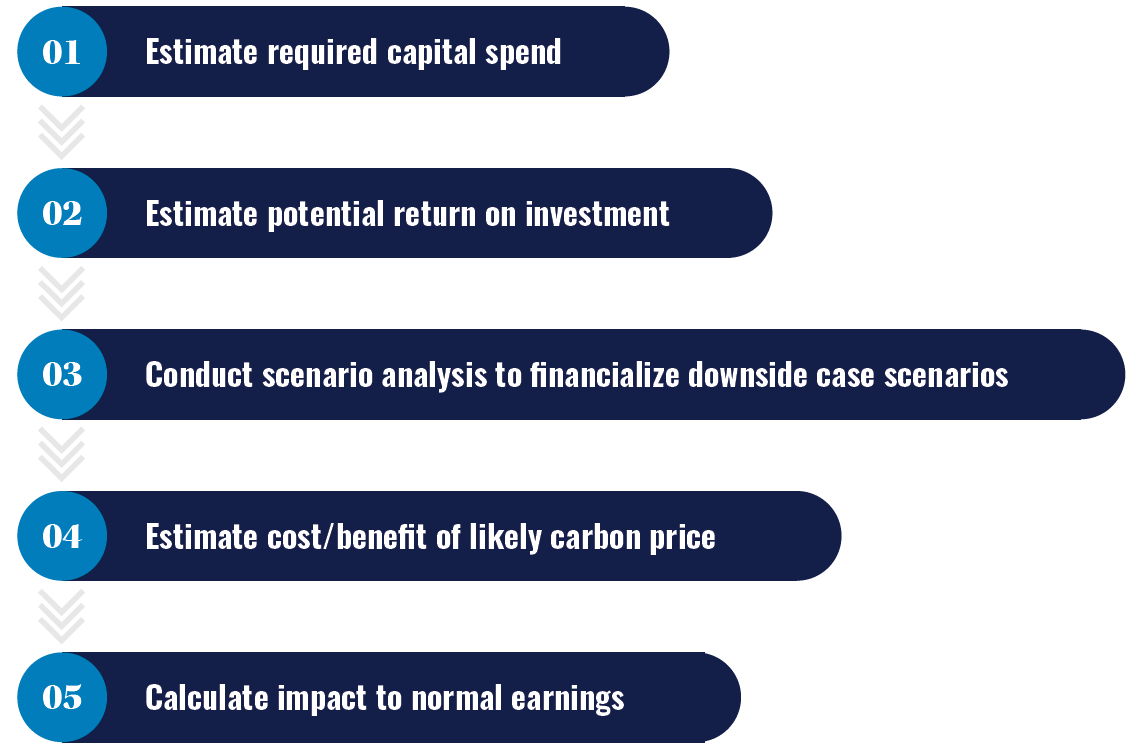

As an example of how we quantify transition risk, we consider a base-case and likely future- state carbon price for the companies we are researching in geographies where a carbon price is relevant. These projections are based on our knowledge and understanding of the ambition of various regulatory frameworks around the world.

Quantifying Transition Risk

Enel: an example of the energy transition as a value driver

Enel, a diversified Italian utility, inherently possesses some climate transition risk given its large traditional generation fleet and exposure to coal-fired power. However, Enel’s management has embarked on a forward-thinking strategy that should ultimately position the company as a contributor to and beneficiary of the energy transition.

Management’s forward-thinking approach to its asset base has effectively turned a risk into an opportunity through three main initiatives:

- Enel more than halved its coal capacity between 2017 and 2022 and has accelerated its eventual exit to 2027, minimizing its interim investment in those assets.

- Enel has invested heavily in renewables, such that now it has optionality to pursue the projects with the highest returns. Its large existing asset base and project management experience also give it advantages of scale compared to other renewable operators.

- Enel will maintain its position in select natural gas generation plants during the energy transition, where plants are still profitable and offer sufficient returns. Overall, Enel projects its electricity production will be approximately 90%greenhouse gas-free by 2030, up from 83% in 2024. Additionally, Enel is targeting emissions cuts consistent with a 1.5 degree warming scenario and a commitment to net zero by 2040.

Enel is on our Opportunity List because the energy transition is an inherent risk, yet also an opportunity, for the business. We engage regularly with senior management, and we have been pleased to see Enel making progress toward its emissions reduction targets while also pursuing a disciplined approach to capital allocation. We will continue to engage management to ensure they stay on course toward these goals. Enel is currently rated a 2 on our proprietary rating scale for Opportunity List companies, reflecting the progress being made on decarbonization. Enel will be a candidate for a 3 rating once the company completes the planned coal exit.

Stewardship Strategy

We engage with company management throughout our due diligence process and extensively after investment. We view stock ownership as an opportunity to help steer companies toward long-term shareholder value creation and therefore favor engagement over divestment. For material ESG issues, including climate change, our aim is to develop a robust understanding of the company’s exposure to the issue and management’s plans to address it. Broadly speaking, our discussions with company management have the following purposes in mind: 1) testing assumptions, 2) maintaining an informed dialogue, and 3) advocacy.

We continually engage with the management of our companies to ensure they are prepared for the energy transition and are structuring their operations to preserve shareholder value. We thoroughly evaluate the quality of company transition plans, and a key part of this analysis is the extent to which we think a company can contribute to and/or benefit from the energy transition. We are also diligent in assessing a company’s carbon intensity (Scope 1 & 2 emissions/$M sales) and will engage with management to discuss the alignment between business strategy and the realities of the energy transition.

Highest Emitters

While we engage with management of our holdings across the board on this issue, we place particular focus on the highest emitters (top 10% of carbon emissions intensity by investment universe) as identified on our Opportunity List. Some of the areas where we may advocate for changes to a company’s actions include, but are not limited to: improved disclosure, including disclosure of scope 1 and 2 emissions at a minimum; laying out a credible path to net zero by 2050 or earlier; and capital allocation earmarked for the energy transition on areas of competitive strength.

We do not exclude companies solely based on their emissions history or carbon intensity. We believe that automatically excluding or divesting from companies with a high carbon footprint negates the importance of active ownership and improvement over time. With the transition to a lower carbon economy underway, starving economically critical businesses of capital because they are more carbon intensive will only make the monumental task of the transition that much harder. The economic criticality of a business does not vanish because it needs to find a way to decarbonize. Simply divesting achieves nothing and may actually drive these companies toward less accountable sources of capital. With that said, if we do not think the company is well positioned in the energy transition, we may avoid buying the stock in the first place, or we may sell it if the investment thesis materially deteriorates throughout the course of our ownership.

Escalation

If engagement has not satisfied our concerns, we may consider multiple escalation strategies. Examples include, but are not limited to, a private meeting with the chairman or other board members; a written letter to members of the senior management team and/or board members; voting against members of the board or resolutions at annual general meetings; and divestment, if the lack of progress changes our view of the risk-reward embedded.

Opportunity List

Our Opportunity List provides us with a structure to utilize fundamental research for assessing the likelihood of issue improvements.

Shell: an example of why engagement matters

Climate transition risk is clearly top of mind when researching any oil and gas company, such as Shell. We actively engage the management of each of our energy holdings on an ongoing basis, with particular focus on key topics, such as: i) whether emissions reductions are in line with market and societal expectations, and therefore minimizing undue risk; ii) quantifying the potential downside case from the energy transition; and iii) ensuring energy transition investments can earn or exceed their cost of capital over time. Informed by these discussions, we develop different scenarios for oil and gas demand based on the potential progress toward decarbonizing, then assess the robustness of our investment thesis under these scenarios.

It is our view that the marketplace still somewhat misunderstands Shell’s efforts to future-proof the business against stranded asset risk. Based on our discussions with Shell management and our own diligence, we continue to view Shell as increasingly well positioned for the needs of the energy transition for the following reasons:

- Shell has outlined a credible net zero plan by 2050. Shell has been criticized for focusing only on intensity (rather than absolute) emissions reductions targets on the pathway to net zero. We believe this criticism is misplaced because, by definition, net zero is an absolute target in the end. It is our view that Shell is being more realistic in the shorter-term targets, acknowledging (as we also believe) that gas demand will not peak for some time.

- Shell is investing in areas of competitive advantage rather than trying to reinvent its business overnight and risking shareholder capital on projects where they have no competitive advantage or expertise. For example, Shell has positioned itself as the largest player in the liquified natural gas (LNG) value chain, an important transition fuel.

- Shell is also making measured investments in transition businesses, including carbon capture and storage (CCS), biofuels, and hydrogen. While the economics of these businesses are still somewhat uncertain, we believe Shell should have a natural competitive advantage once the market matures.

Shell is on our Opportunity List, reflecting the company’s improvement trajectory, while also acknowledging the near-term investment controversy of the energy transition. As part of our engagement plan for Shell, we expect to see continued progress towards stated emissions reduction targets, with appropriate capital discipline, as well as continued evolution of business mix, given eventual runoff demand for fossil fuels. Shell is currently rated a 2 on our proprietary rating scale for Opportunity List companies. While we agree with Shell’s transition plan, we also acknowledge the challenges the oil and gas industry faces in getting to net zero by 2050. We continue to discuss Shell’s energy transition strategy and associated medium- and long-term capital allocation priorities with management.

3. RISK MANAGEMENT

At Pzena, we think about and manage climate risks the same way we consider any fundamental investment issues. First and foremost, we define risk as the permanent impairment of capital, taking seriously any issue that has this potential, and climate change falls into this category. Risk controls are embedded throughout the investment process, from research to portfolio construction to trading.

Commitment to Research Depth

The most meaningful risk management technique we employ is our commitment to research depth. As bottom-up value investors, we place a particularly strong focus on downside risk in the companies in which we invest. We look to minimize risk mainly through our bottom-up company research, as we seek to determine the nature of a company’s undervaluation, the quality of its operations, and the strength of its balance sheet. Our analysts track material news affecting the industries and/or companies they cover and incorporate key developments into our company-specific financial models, including physical and transition climate risk. This analysis is informed by our ongoing engagement with company management, and it helps to structure our engagement agenda.

Extra Due Diligence

As an extra layer of due diligence, our ESG team is responsible for helping to ensure consistency across the research team, thinking about how material issues such as climate change cross-cut various industries. While climate change poses significant risks to most global industries, we believe there are a few key industries where the changes will be felt earlier, with greater implications for company earnings potential. The ESG team led a deep dive on the topic of net zero, providing the research team with a framework to assess the credibility of company net zero plans. Research analysts have since conducted net zero assessments for companies under their coverage with exposure to material climate transition risk. These companies are also typically on our Opportunity List, which means we are consistently monitoring and updating associated company engagement plans.

Portfolio Management

Companies and, by extension, industries receive higher weightings in the portfolio when the valuation discount is high and we can reasonably judge the range of potential business outcomes to be narrow. The ideal investment is a company that, based on our estimate of normalized earnings, trades at a significant discount to the market and where we believe we have properly assessed the downside risk.

Risk management is implemented at the portfolio management level by the portfolio managers and the portfolio implementation group. Portfolio Review meetings are generally held every other week. All portfolio managers and those involved in the administration of client portfolios review the investment strategy and the current holdings in each portfolio. Issues such as turnover, security weightings, and sector weightings are all reviewed to confirm we are following both strategy and client guidelines. Model changes, priority buys, sells, and trims are set at these meetings. Risk management is also incorporated into our subsequent trading procedures, including abiding by limits determined by the portfolio implementation process and limiting the volume of trading so as not to impact prices.

Tools

Through the firm’s proprietary screening tool, StockAnalyzer, along with third-party risk management tools (e.g., FactSet, MSCI Barra), we regularly review individual stocks and aggregate portfolio-level risk factors. As it pertains to climate change, these risk factors include, but are not limited to, company carbon emissions intensity, MSCI ESG score, and a failure of UN Global Compact Principles (UNGCP). Reports are run by the portfolio administrators and monitored by the portfolio managers. This review may result in additional company-level analysis, further engagement with company management, and adjustments to position sizes where necessary, as estimates of expected upside versus downside evolve.

4. METRICS AND TARGETS

Data

Without good data, it is impossible to accurately assess and quantify the impact of climate change on our investments. There are significant limitations with available climate-related metrics, especially related to availability, consistency, and reliability. We question the utility of many of the scenario analysis datasets available from third parties because they rely too heavily on forward-looking estimations and assumptions to be particularly useful when assessing the optionality available to individual companies.

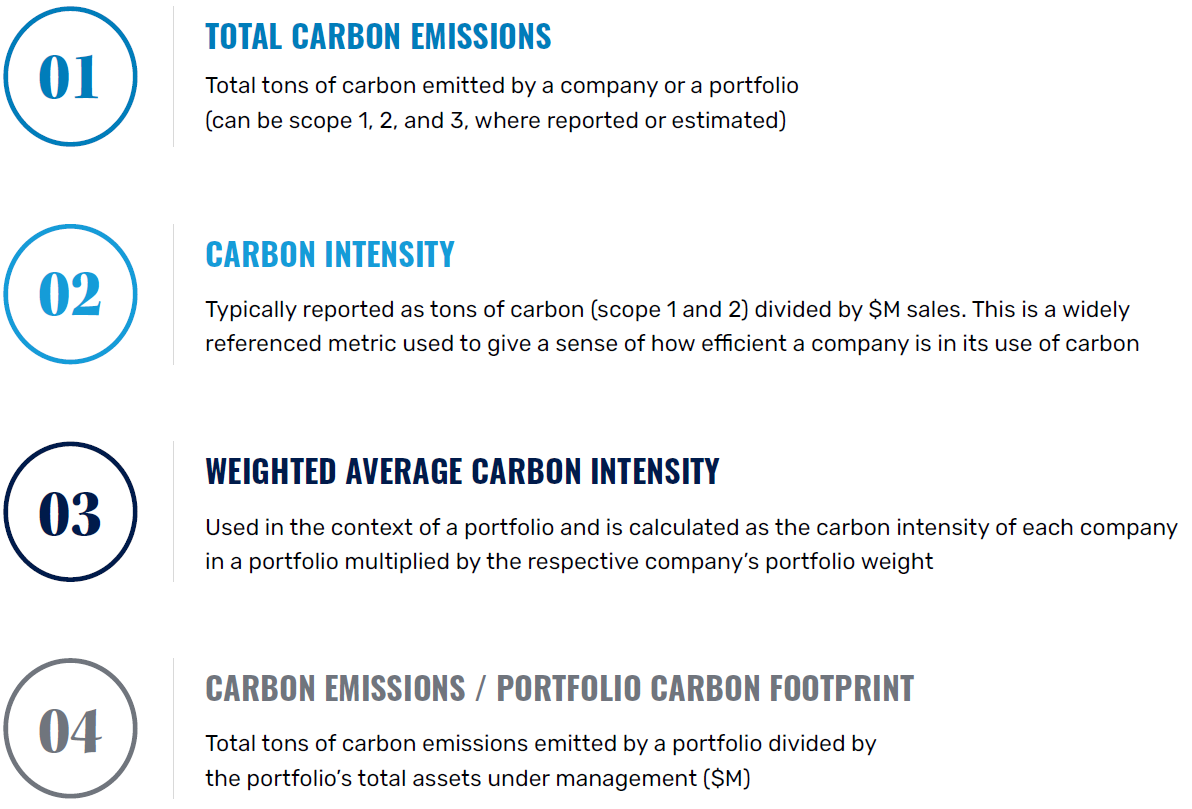

It is important to have access to relevant information, even considering the aforementioned limitations. For our standard strategies, we deem it a priority for our investment team (and our clients) to have access to the following specific metrics provided by third parties:

We use these metrics to assess the carbon exposure of all of our portfolios and determine which companies are the biggest detractors and contributors. While we do not target a particular carbon exposure (unless directed by a client), this gives us the opportunity to take stock of the overall portfolio exposure and prioritize engagements as needed.

In addition, we use general data sources (ESG or otherwise) that include reference to climate-related risks and opportunities at the company level. To gain additional insight, we engage regularly with companies on climate, review climate-related reporting, data, and research, and attend and present at industry events where these issues are discussed. One of our ongoing areas of focus is encouraging better disclosure of climate-related metrics from companies where climate change presents a material risk or opportunity.

Goals

For our standard strategies, we have not set any top-down portfolio targets for managing climate-related risks and opportunities, though we will manage to client-directed targets or emissions budgets as needed. Instead, we focus our efforts at the company level, encouraging portfolio companies to achieve emissions reductions over time and capitalize on opportunities in the energy transition where they have a competitive advantage. Given that our portfolio is regularly cycling (turnover averages about 30%), with companies that reach fair value being replaced, these company-specific improvements may not show up in a portfolio-level snapshot at a point in time. We therefore prefer to focus attention on the bottom-up improvement story for individual companies in the portfolio, rather than setting top-down emissions reductions targets.

Global Value Climate

At the request of clients, we launched a Global Value Climate portfolio. For clients that decide to invest in this strategy, we have more explicit climate-related metrics and targets aligned with the Paris Aligned Investment Initiative Net Zero Framework, including the following:

Conclusion

As investors, we play an important role in the responsible allocation of capital. Assessment of financially material climate risks and opportunities is an essential part of making better and more informed investment decisions. This is not, however, an issue where we can remain static; we will continue to reassess and refine our approach, continually exploring ways to better identify, measure, and assess the impacts of climate change. To the extent that this depends on better data availability from companies, we will continue to advocate for more consistent and readily available disclosure where climate risk is material to companies in which we invest.

Further information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management, LLC (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such

as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2026 by ASIC Corporations (Amendment) Instrument 2024/497. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

© Pzena Investment Management, LLC, 2025. All rights reserved.