Tariffs Through the Lens of Our Risk Framework

First Quarter 2025 Commentary

12 min read

While tariff fears and economic volatility are testing markets, our systematic risk framework allows us to evaluate exposures and identify resilient companies amid global trade uncertainties.

Volatility in global markets ticked up in the first quarter as investors grappled with uncertainty. Tariff fears have been at the forefront since President Trump won the U.S. presidential election in November of last year, exacerbated by the broad-based tariffs announced in April. In this essay, we discuss the following:

- Pzena’s risk analysis framework

- The unprecedented tariffs announced at the beginning of April

- How we assess both the tariff and broader economic risks within our risk framework

PZENA’S RISK FRAMEWORK

Having an appropriate risk framework is critical to successful investing, to avoid what we believe

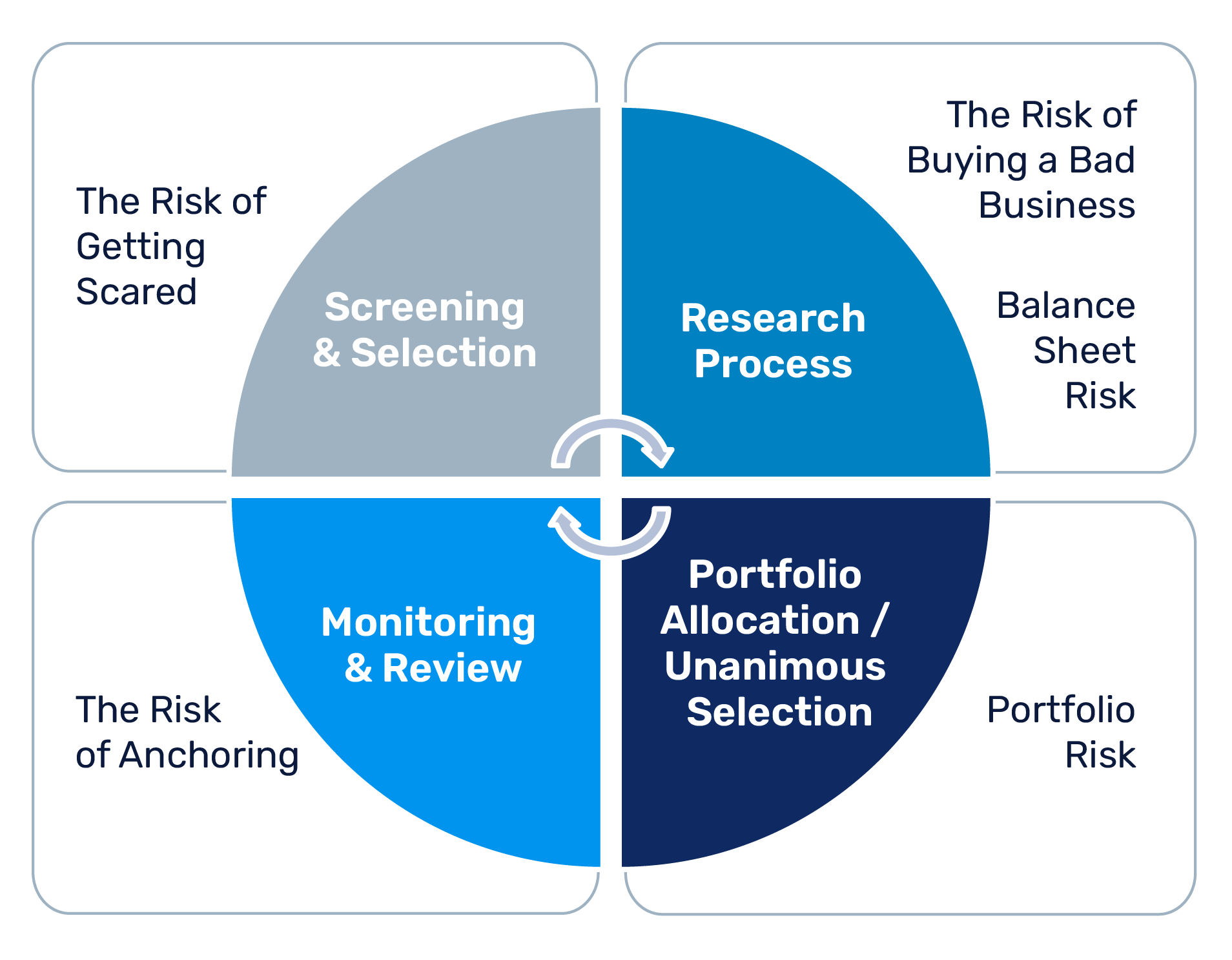

is the ultimate impediment to long-term portfolio performance: permanent impairment of capital. As value investors, we seek opportunities among cheap stocks—where there is controversy and/or something has gone wrong, and the risk of impairment is low. This tension—buying cheap stocks versus avoiding permanent capital loss—is central to our process. The cost of safety is paying a premium for businesses with fewer issues, reducing potential returns; however, taking excessive risks can quickly impair performance. To manage this balance, among the many risks we consider, we focus on five key categories of risk: getting scared, buying a bad business, balance sheet events, portfolio construction, and anchoring on deeply researched positions (Exhibit 1).

Exhibit 1: Pzena Risk Analysis Framework

RISK OF GETTING SCARED

A central tenet of our philosophy as value investors is that you only get the opportunity to buy good businesses at a substantial discount when there is a problem. The challenge this presents to human beings with emotions is that the instinct is often to avoid problems and find something less scary. We avoid this bias by focusing our screens only on companies likely to be in the cheapest quintile. Focusing on the cheapest quintile ensures we look at the most promising names and maintain our valuation discipline.

Our starting point is a company’s previous 10 years of history, which we use in a systematic process to forecast future earnings. This ensures the forecast is based on the company’s history and not the current fear.

RISK OF BUYING A BAD BUSINESS

We seek to develop a deep understanding of the economics of the underlying business we are considering. We have several formal touchpoints where we gather as a team to debate, probe, and deepen our understanding. During this process, we seek out the bear thesis and other contrarian views to bring different perspectives. We research each position as if we were buying the entire business and try to understand the underlying economic drivers, the industry’s competitive dynamics, management’s plans, supplier/customer behavior, and other key factors.

Once we have a fully baked investment thesis, we visit the management team on-site. These visits are intentionally done at the end of the process, so we have an informed view and are not just listening to management’s standard pitch. We do a final review, debating the company’s normal earnings power. When a research project completes this process, there have been multiple formal opportunities for everyone to debate the issues, ensuring we understand the business, its earnings potential, and the possible range of outcomes.

RISK OF A BALANCE SHEET EVENT

Equally, if not more important, is whether the business has a liquidity profile that allows it the flexibility to reach that long-term potential. This involves looking at the level of debt and its maturity dates, in the context of our assessment of the company’s cash flow profile. Leverage is the enemy of the value investor, as being right about the long-term outcome is meaningless if a liquidity event substantially dilutes the equity on its path to recovery.

To mitigate liquidity risk, we model equity issuance for each company to reduce its net debt to net working capital. This forces many of the most leveraged names—where cheapness of the equity may be a function of excessive balance sheet debt—out of the first quintile. If a name makes it through the process with high leverage, and we choose to invest, we will typically hold a smaller position in the portfolio than we might otherwise.

PORTFOLIO CONSTRUCTION RISK

We regularly assess portfolio construction to manage industry and country exposures. Portfolio decisions require unanimous agreement among the portfolio managers, which sets a high bar, ensures thorough debate, and eliminates individual biases. When a stock underperforms, we ask: should we buy more, hold, or exit? We may increase our stake if incremental data supports our thesis, but the stock drops. If new data contradicts our thesis, we reduce or exit the position.

We also utilize external tools to monitor whether our perceived risks align with actual exposures. This helps ensure the portfolio remains balanced and diversified while maintaining our valuation discipline. It is also consistent with historical research highlighting that, over the longer term, the richest rewards lie in investing in the cheapest quintile of market valuations.

RISK OF ANCHORING

Deep research can lead to emotional attachment. To counteract this, we enforce a strict sell discipline. Stocks are sold when their valuation reaches the market midpoint, with gradual trimming as they appreciate. This constant recycling into cheaper stocks maintains portfolio discipline.

We continuously monitor industry news, earnings, and macro events to assess whether new information aligns with our original thesis. Contradictory data prompts re-evaluation and potential position adjustments. We also speak with management periodically and meet with them at least annually to stay informed.

We rotate industry coverage among analysts every 3–5 years to prevent cognitive biases. This fresh perspective helps avoid anchoring and complacency, while enhancing team development.

TARIFFS

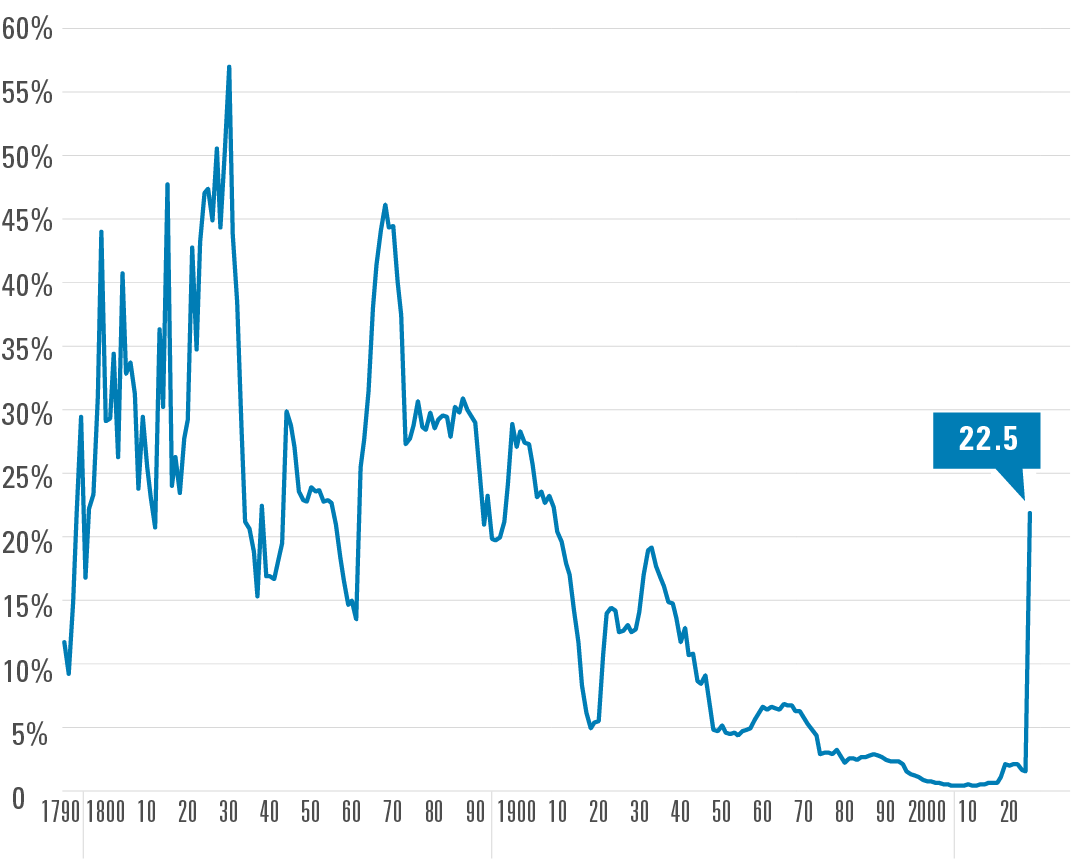

Our investment process is focused on identifying and analyzing all the risks of a potential investment before it enters the portfolio, while ensuring a company has the market position and financial wherewithal to absorb unforeseen risks that inevitably arise. Broad-based tariffs and trade concerns have emerged as a significant market risk over the past six months, particularly after the April 2nd announcement (see Exhibit 2).

Exhibit 2 – Proposed US Tariffs: Highest Level in Over 100 Years

The US Effective Tariff Rate on Dutiable Imports 1790 Through 2025

Source: Empirical Research Partners

Data as of April 9, 2025.

Global markets sold off sharply following the announcement, on fears that the tariff war would trigger a global recession. We’ve previously written extensively about the impact of recessions (2Q22 Commentary). We found the following to be true:

- It is incredibly hard to predict recessions. Paul Samuelson, a Nobel Prize winner in Economics, famously said, “The stock market has predicted nine out of the last five recessions.”

- Successfully trading around recessions requires not only calling the recession itself but timing both exit and re-entry points.

- By the time a recession is declared, the pain has already been felt, and the outlook for equity investors is typically attractive.

- Value tends to underperform in the sell-off leading into a recession, but significantly outperforms coming out of a recession, ultimately well ahead of the market for the period starting from the pre-recession peak.

TARIFFS THROUGH THE PZENA RISK FRAMEWORK

Tariffs and trade wars are always a threat, and we assess these risks on a company-by-company basis under the same framework described above:

- Bad Business/Balance Sheet – With the final policy so uncertain, our starting point was to stress-test all portfolio companies to assess the potential impact on normal earnings in a worst-case scenario and ensure each balance sheet was not at risk of impairment.

- Getting Scared – There are potentially new companies in the cheapest quintile due to trade fears.

- Portfolio Construction – We want to ensure our portfolios aren’t overly exposed to any potential tariffs.

- Anchoring – N/A

The current iteration of the Trump administration’s policies is far more punitive than most had predicted, though the potential impact of tariffs on the global economy remains to be seen. It is crucial to evaluate the impact on a company-by-company basis, considering the core value-add and market position of each relative to competitors. This helps identify which companies or industries may gain or lose market share due to specific tariffs and which have the pricing power to transfer these costs to customers.

We undertook a review of all companies in our portfolios to determine their relative vulnerabilities to tariffs and their strategies for coping. Below, we offer examples:

- Over the past several years, U.S. consumer products company Newell Brands has cut its hinese manufacturing down to roughly 15% of the cost of goods sold, with a plan to reduce this number to 10% by the end of 2025. Most of the Chinese exposure is in the baby division, and it is currently exempt from Section 301 tariffs to give relief to young families. Initially, we believed this would give the company a significant cost advantage, but the broad geographic tariffs announced in early April touched geographies the company had shifted to. Additionally, only 5% of the company’s cost of goods sold (COGS) is in Mexico, and the Canadian exposure is negligible. With most of its manufacturing and sourcing in the U.S., we believe the company should still likely have a cost advantage over its competitors.

- Tire manufacturing represents a non-discretionary replacement item that should

be able to pass through the tariffs to the end user, but this might affect competitors in very different ways. Roughly 60% of U.S. tires are imported. French tire manufacturer Michelin supplies about 75% of its U.S. demand from local production, which is not subject to tariffs. The company could benefit as import tariffs would raise the cost of cheaper, low-end tires produced by Asian competitors. On the cost side, Michelin has manufacturing flexibility

to move production longer term, while raw materials for tires are typically sourced locally, so supply chain issues should be manageable. - Chinese home appliance maker Haier generates about 30% of its revenue in North America, with 50% of that sourced from the U.S., 30%from Mexico, and 10% from China. Tariffs primarily impact the 10% from China, equating to around 3% of revenue. To address tariff pressures, Haier plans to share costs with suppliers, improve manufacturing efficiency, and adjust prices without sacrificing market share. In the case of severe tariffs, Haier would increase U.S. production with additional capital spending, which could be easily accommodated with its strong cash flows. Despite potential downstream economic effects, Haier’s appliance business remains stable, as a large portion of revenue is driven by replacements and upgrades rather than new home sales, making it more resilient than other consumer categories.

These are just a few examples, but they are indicative of the broader conversations our research team is having regarding tariff risk. Many of our companies with manufacturing assets in China have downsized their production capacity since the last tariff iteration in 2018–2019, only to see the broad tariffs announced once again impact them. There is still a high degree of uncertainty regarding future and final policies from the Trump administration, especially since they are broad-based. And because we don’t know what tariffs may look like, we stress-test our holdings with potential exposure to quantify the earnings impact in a worst-case scenario.

CONCLUSION

While tariffs and trade uncertainties present risks to global businesses, history suggests ingenuity of management and adaptability of business models could mitigate the impact of trade issues. At Pzena, our rigorous risk framework allows us to navigate these uncertainties with discipline and focus. By concentrating on fundamental business quality, balance sheet strength, portfolio construction, and maintaining valuation discipline, we aim to mitigate potential downside and explore potential opportunities created by the uncertainty, positioning for long-term returns. Although the ultimate impact of current trade policies remains uncertain, our investment approach ensures that we assess each company’s ability to withstand and adapt to evolving conditions. This disciplined, research-driven methodology enables us to capitalize on opportunities that arise from market fears while attempting to safeguard against permanent capital impairment.

TARIFFS AND TURBULENCE

Portfolio Manager John Flynn and Director of Business Development & Client Services Adrian Jackson discuss the topical subject of tariffs, through the lens of the risk management framework of Pzena’s investment process.

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2026 by ASIC Corporations (Amendment) Instrument 2024/497. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

The Pzena Emerging Markets Focused Value Fund, Pzena Emerging Markets Select Value Fund, Pzena Global Focused Value Fund, Pzena Global Value Fund are registered and approved under section 65 of CISCA.

Collective Investment Schemes in Securities (CIS) should be considered as medium to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. There is no guarantee in respect of capital or returns in a portfolio. Representative Office: Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any additional information such as fund prices, fees, brochures, minimum disclosure documents and application forms please go to www.pzena.com.

© Pzena Investment Management, LLC, 2025. All rights reserved.