China’s Stimulus Boosts Investor Sentiment

For Financial Advisor Use Only

5 min read

China recently announced several stimulus measures, mostly targeting the beleaguered property sector, which have been interpreted positively by investors. These initiatives include

- The required downpayment for second homes has been reduced to 15% from 25% previously

- The interest rate on existing mortgages was reduced by 50 basis points

- The PBOC is allowing Chinese banks to draw down the full amount of its RMB 300bn lending facility, which is designed to encourage Chinese SOEs to buy up excess property inventory via cheap financing

- The government is issuing one-off cash handouts to the poor (unspecified amount)

- It’s being reported that the government is considering a RMB 1T capital injection into the nation’s state-owned banks, which is similarly designed to spur cheaper lending to weak areas of the economy

- Perhaps most consequentially as it pertains to equities, minutes released from the latest Politburo meeting indicate that the CCP is ready and willing to deploy potentially substantial fiscal stimulus to stabilize the economy, with the property sector specifically cited as a target of that stimulus (though it should be noted that details on these plans are scarce)

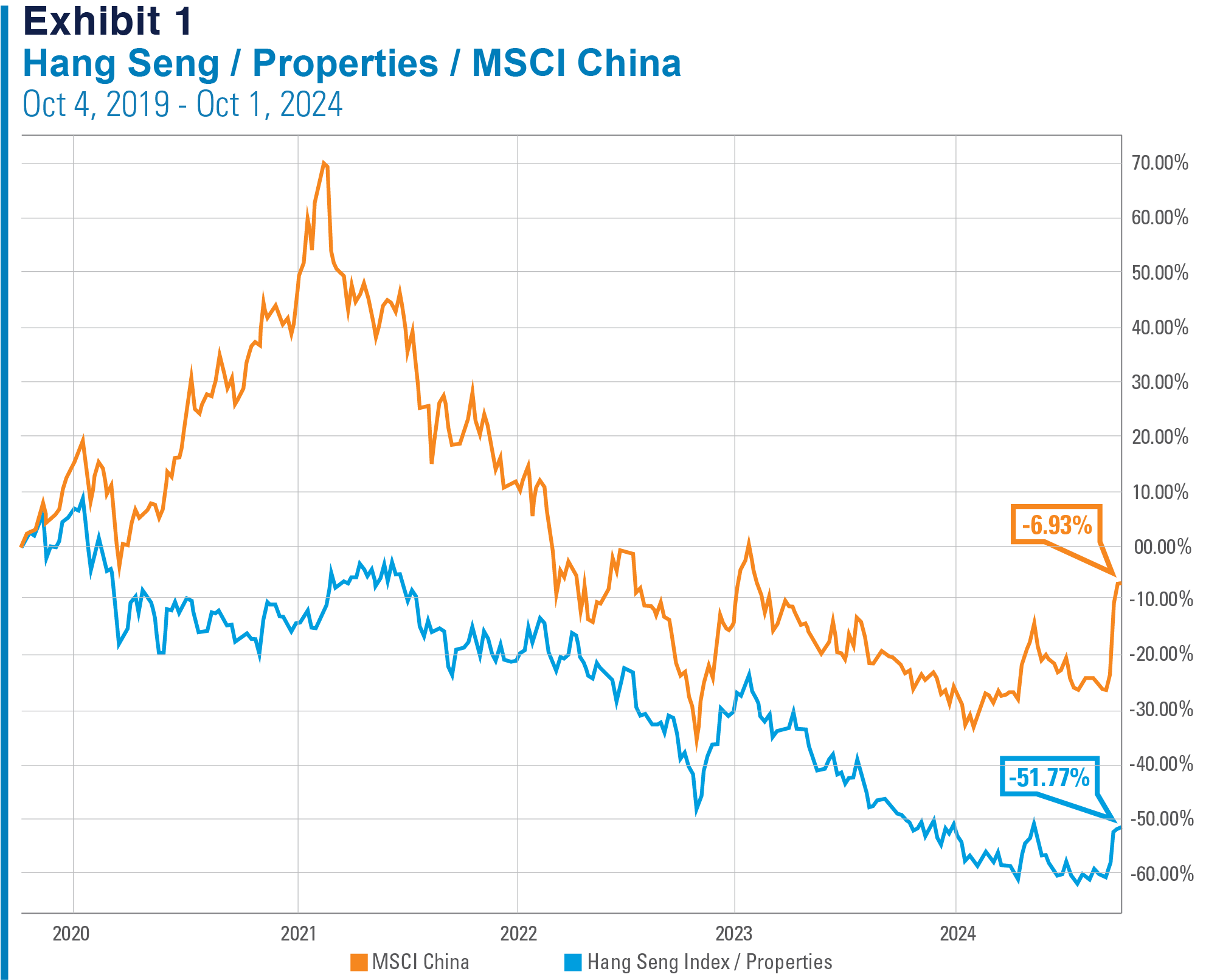

Clearly this is positive for investor sentiment, as it implies President Xi and the CCP are at least acknowledging that the existing stimulus measures haven’t been enough to really move the needle, and more will be required if China is to achieve its 5% GDP growth target for this year. As a result, the Chinese property sector and broader market are both up double digits over the past ~2 weeks. Though we point out that both are still down materially from pre-pandemic levels, and, as such, Chinese stocks broadly remain extremely cheap, with the MSCI China trading at a single-digit forward earnings multiple.

All of this is to say that the Chinese property sector – which is of particular economic importance given that an estimated 70% of household wealth is tied up in real estate – is still in considerable pain, and it remains to be seen whether these recent stimulus measures will help put a floor under housing prices, which, in turn, could provide a boost to consumer spending.

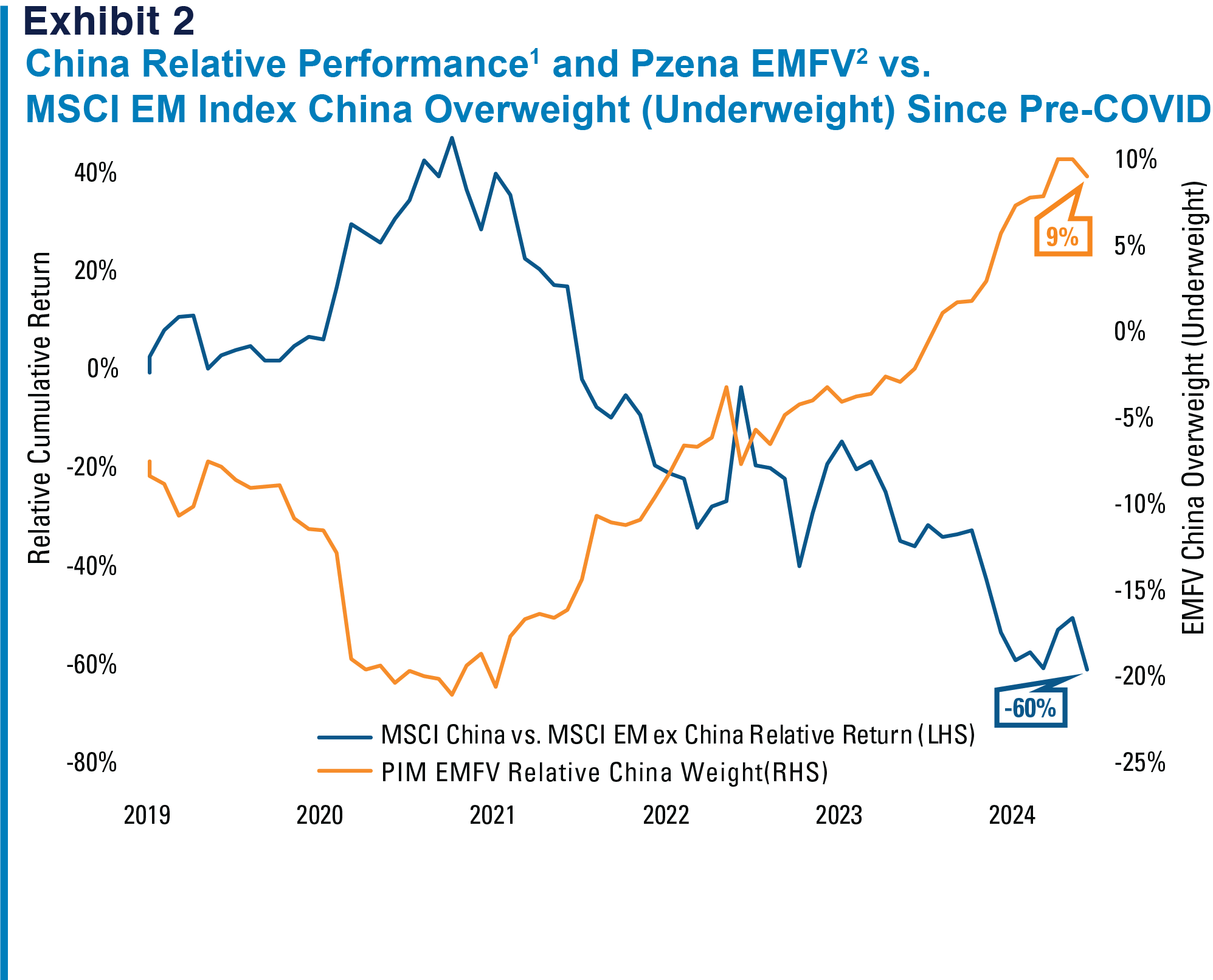

Importantly, our investment theses for the individual Chinese stocks that we own are not predicated on significant monetary or fiscal support from the government. These businesses are, in our view, trading at exceptionally low valuations that already discount persistent and severe pain – the result of investors’ indiscriminate selling of anything with a Chinese domicile in recent years. As Chinese valuations collapsed, we selectively took up our exposure to stocks we believe have been unjustifiably sold off due to temporary geopolitical and macroeconomic headwinds.

Source: FactSet, Pzena analysis

1 Total return data in US dollars December 31, 2018 – June 30, 2024.

2 Pzena Emerging Markets Focused Value Composite estimate; includes both China and Hong Kong.

1. Source: Bloomberg

FURTHER INFORMATION

This document is intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results. All investments involve risk, including risk of total loss.

All investments involve risk, including loss of principal. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased

The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.