Highlighted Holding: Ibstock

3Q 2024 – For Financial Advisor Use Only

In the United Kingdom, approximately 75% of housing facades are made of brick1, and Leicestershire-based Ibstock is the country’s #1 manufacturer of clay bricks2, with a supplemental portfolio of five well-known concrete brands that cater to construction end markets.

Ibstock’s business is levered to residential building activity in the UK, and with housing starts down sharply in recent quarters, the company’s top and bottom lines have, unsurprisingly, come under pressure. We believe that Ibstock, given its dominant market position, flexible cost structure, and vertical integration, is among the best-positioned building materials companies to capitalize on an anticipated rebound in UK residential construction—an eventuality that we do not believe the market is appropriately pricing in.

The UK Housing Downturn

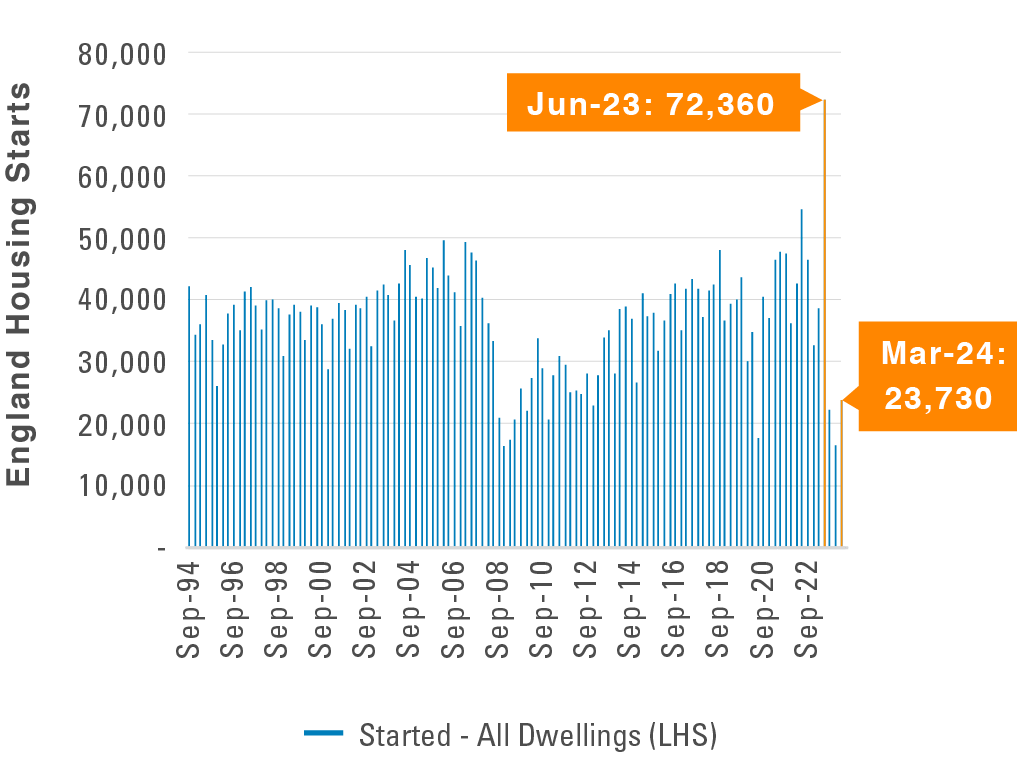

At the end of 2021, the Bank of England began rapidly hiking its policy rate to combat inflation. UK mortgage rates rose in concert, with the 5-year fixed rate peaking at 5.7% in the summer of 2023, up from 1.3% in late 20213. At the same time that mortgage costs were surging, UK real wages were plummeting, along with the near-term prospect of homeownership for millions of Britons. In 2023, with housing affordability at its lowest in nearly 15 years4, the UK government unveiled new building standards, prompting a massive pull-forward of construction to get ahead of the regulations (Exhibit 1, June ’23 quarter). What naturally followed was a major drop-off in new builds, and with the lack of affordability sapping demand, developers have had little incentive to ramp up construction since.

Exhibit 1: New Builds Plummet

Source: UK ONS

Consequently, UK brick deliveries collapsed, falling nearly 30% year-over-year in 2023, and by our estimates, they remain approximately 20% below-trend today.

Industry Resilience

The environment has been undeniably challenging for UK brickmakers, but an attractive industry structure has insulated Ibstock from further financial pain. Ibstock, along with peers Wienerberger and Forterra, maintains a roughly 90% market share in what is effectively an oligopoly—the result of decades of market consolidation. The industry also has very high barriers to entry, given the massive capital investments and permits required, while foreign brick imports come with especially high transportation costs.

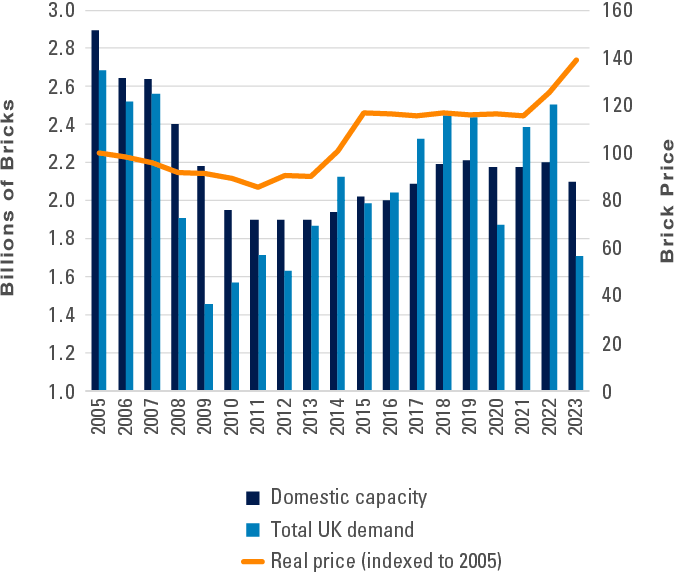

During the 2008–09 housing collapse, the industry responded by taking a significant amount of capacity out of the system. As the market rebounded, domestic demand began to outstrip available supply around 2014, and the shortfall had to be filled via expensive imports, which peaked at about 23% of demand in 20225 (Exhibit 2). Imports have since begun to normalize lower, which we expect to continue, while domestic brick capacity today is more aligned with a normal level of demand, supporting structurally higher margins for Ibstock.

Exhibit 2: UK Brick Supply and Demand

Source: Redburn Atlantic

Most importantly, the trio have remained exceptionally disciplined on price amid the pronounced volume drop-off, being unwilling to undercut one another for market share gains at the expense of margins. This is a major reason Ibstock was able to post a 33.8% adj. EBITDA6 margin for its clay business in 2023, down just 50 basis points from the prior year, despite deliveries falling approximately 30% year-over-year7.

Earnings Inflection

In contrast to Ibstock’s core Clay business, which is mostly exposed to residential housing, its non-core Concrete unit has more diversified end market exposures (rail & infrastructure, fencing, elevator shafts, etc.), which is a key reason the segment’s FY24 sales are expected to be up year-over-year. That said, Concrete only accounts for approximately 12% of our normal earnings estimate, so Ibstock’s re-rating is contingent on the Clay business normalizing.

There are two aspects to Ibstock’s Clay earnings recovery, in our view. One is cyclical and market-driven, while the other is more company-specific. After underbuilding for decades, the UK needs homes—a lot of them. Britain’s housing deficit now stands at an estimated 4.3 million homes, while population growth is outpacing housing completions at the steepest pace since the 1940s, according to Bloomberg.

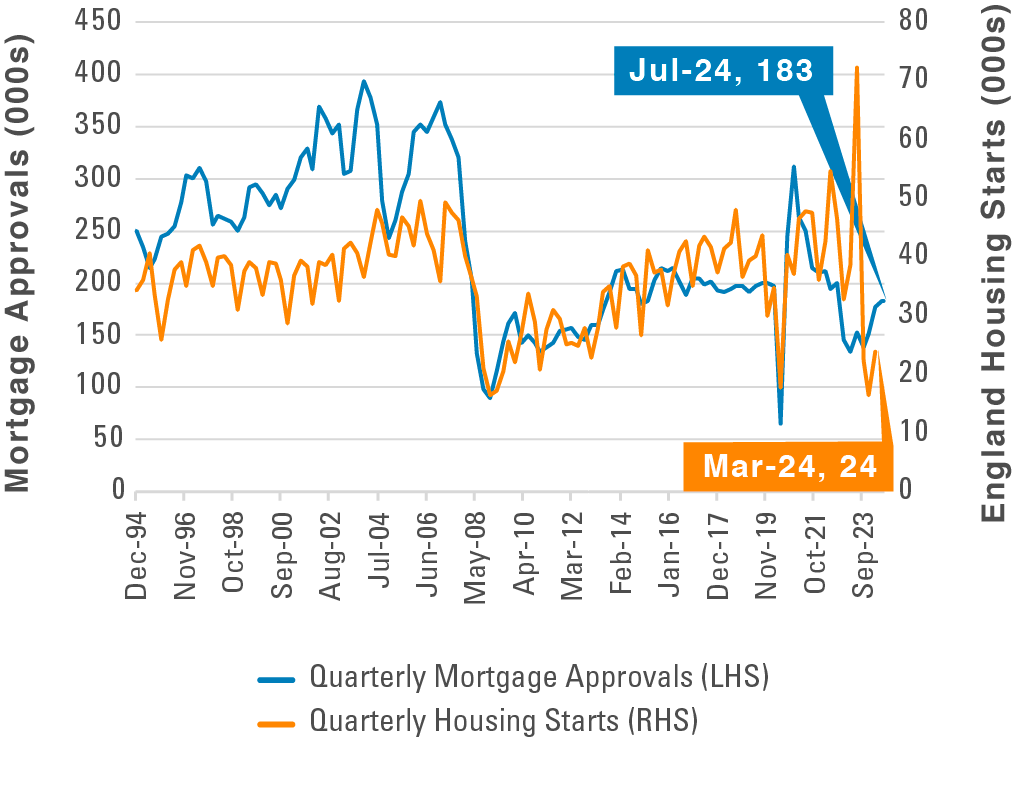

In response to the glaring housing shortage, the new UK government is aiming to build 300,000 homes per year in England over a five-year period. This is an extremely ambitious target, considering UK builders have not added that number of dwellings in a calendar year since the 1960s8; however, it is directionally positive insofar as the government is actively trying to tackle this increasingly acute issue. At the same time, mortgage rates have been declining, which should materially improve housing affordability and thus, barring a major recession, demand. This is already showing up in the data, as UK mortgage approvals, which are positively correlated with housing starts, have been steadily rising for the past 10 months9 (Exhibit 3).

Exhibit 3: Mortgage Approvals on the Rise

Source: Bloomberg, ONS, Bank of England

*2Q24 housing starts data has yet to be released

The implication is that UK brick demand is slated to rise materially from 2023’s depressed level of 1.7 billion, which is roughly 600 million below the average between 2000 and 202210. We are conservatively modeling total UK demand of 2 billion bricks by 2028, which is underpinned by an estimated 150,000 housing completions—well below both the government’s target and 2019’s level of 177,00011.

On the company-specific front, we believe Ibstock’s vertical integration and operational flexibility are paramount to its long-term earnings power. Ibstock operates 32 clay and concrete manufacturing plants (all in the UK) and owns 73 million tons of clay reserves12 in close proximity to its facilities, providing it with long-term, strategic access to its key input. Ibstock’s supply chain advantage is a major reason it has maintained above-industry operating margins, and we expect that to persist through the current cycle.

We also expect Ibstock to continue replacing high-cost capacity with cheaper production, resulting from years of investment in state-of-the-art facilities. While Ibstock’s growth spending is beginning to wind down, the benefits of a higher-quality asset base have yet to show up on the P&L statement, and we believe the market is not appreciating the prospect of a structurally higher margin profile once volumes normalize. In the interim, Ibstock’s strong balance sheet should enable it to weather the current downturn without the need for additional capital.

Conclusion

In our view, Ibstock is the quintessential value stock: an excellent franchise operating in a consolidated industry that is experiencing cyclical—but temporary—pain. The stock’s solid performance in the third quarter is a reflection of investors’ rising expectations of a top-line recovery; however, we believe this represents only a fraction of the anticipated multi-year earnings improvement conservatively underpinned by a normalization of housing starts and modest margin expansion. We believe Ibstock’s normal operating profit is approximately twice this year’s expected level of £44M, which equates to approximately 8.1x our normal earnings estimate.

Footnotes

- Brick Development Association

- Company filings

- Bloomberg

- Bloomberg, relative mortgage cost = mortgage payments as % of mean take-home pay (first-time buyers)

- Redburn Atlantic, ONS

- Earnings before interest, taxes, depreciation, and amortization

- Company filings

- ONS

- Bloomberg, ONS, Bank of England

- Redburn Atlantic

- ONS

- Company filings

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not

be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

Ibstock was held in our International Small Cap Focused Value strategy during the third quarter 2024.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2026 by ASIC Corporations (Amendment) Instrument 2024/497. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1

of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2024. All rights reserved.