Highlighted Holding: Samsung Electronics

First Quarter 2025

Samsung is navigating a cyclical downturn in the global memory market, which is impacting its core business; however, its dominance in conventional memory chips, strong consumer electronics franchises, and robust balance sheet position it well for a powerful recovery and long-term, sustainable earnings growth.

Korea’s Samsung Electronics is perhaps best known for its high-end OLED TVs, audio equipment, popular Galaxy smartphones, and wide array of home appliances. A part of the business that consumers don’t see—memory chips—drives the bulk of the conglomerate’s earnings, but it is also what has been weighing on the stock’s valuation. A memory downcycle has impacted Samsung’s profitability, while investors worry its competitors have an insurmountable lead in a specific type of high-end memory required for AI applications.

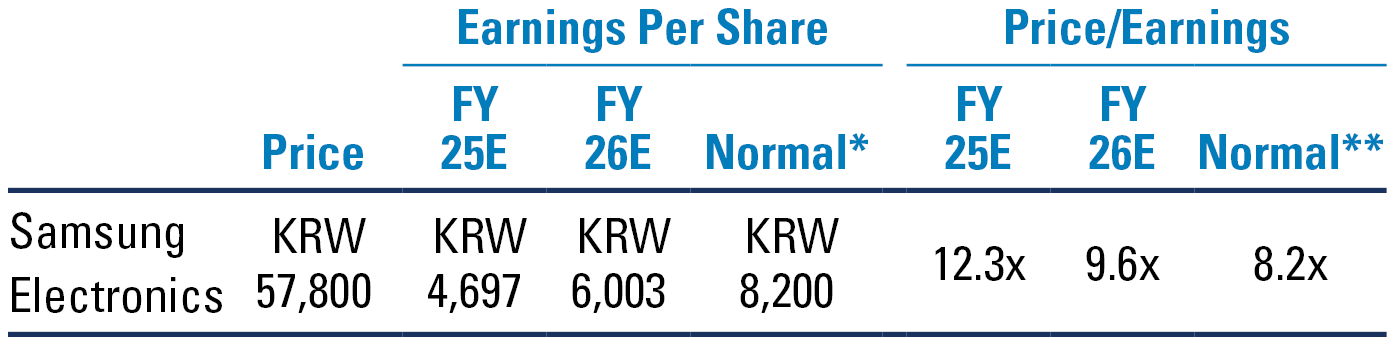

We expect the characteristically cyclical memory market to ultimately normalize, as supply and demand come back into balance, while Samsung should maintain its dominance in conventional chips. With shares trading at a low double-digit earnings multiple despite 15% projected annual earnings growth1, we believe investors are underappreciating Samsung’s scale and financial strength, moderating growth capex2, and dominant smartphone, display, and consumer electronic franchises, while overreacting to its technological gap with peers on next-generation memory chips.

Samsung: A Sprawling Global Electronics Conglomerate

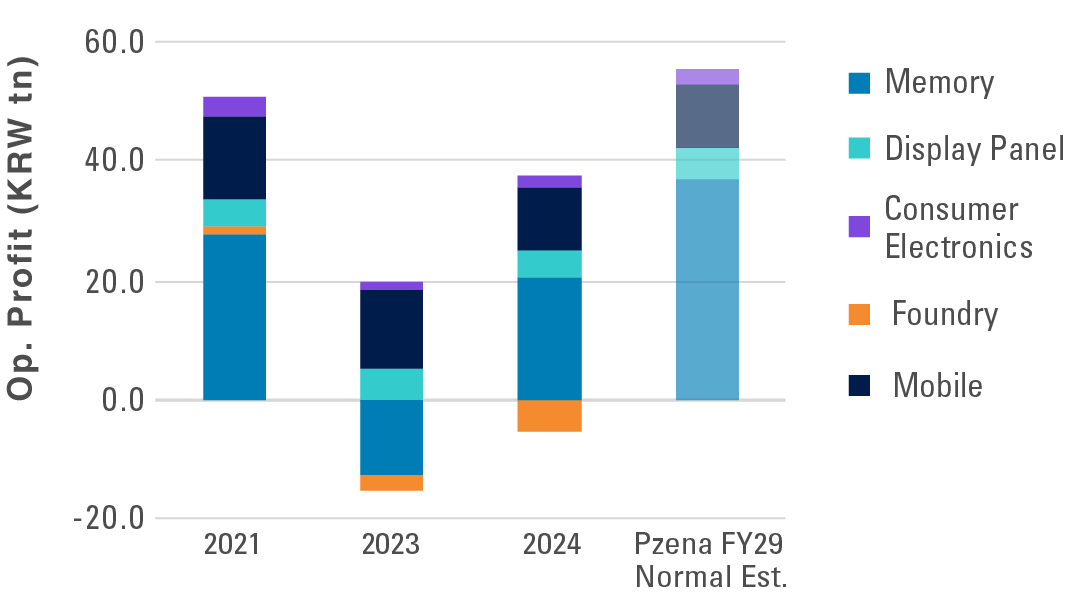

While memory is the main driver of Samsung’s expected earnings improvement, roughly a third of the company’s estimated normal earnings power—representing approximately $147bn in FY24 sales—is derived from its other segments (Exhibit 1). Its 58,000-employee, $20bn revenue subsidiary, Samsung Display, designs and manufactures OLED display panels for devices such as smartphones, laptops, and TVs. This business has a leading 50% global market share3, and makes up ~10% of Samsung’s companywide revenue.

Fiscal year-end March 31.

*Pzena estimate of normal earnings.

**Globally adjusted price-to-normal multiple based on Korean discount rate.

Source: FactSet, Pzena analysis. Data as of March 31, 2025

Samsung’s semiconductor foundry business, though relatively subscale, is still the second largest chip manufacturer in the world behind TSMC4, generating $18bn in annual sales. This business has been in the red for the past two years, though losses are expected to narrow by way of yields improving or capacity reductions, and we are only assuming breakeven profitability in our model.

Samsung’s mobile unit is a global juggernaut, responsible for 223 million smartphone sales last year (behind only Apple)5, translating to $7bn in operating profit. This segment, which we estimate makes up about 20% of normal operating income, has acted as an earnings ballast for the company, with stable volumes, low-double-digit margins that are rangebound, and steadily rising ASP6 driven by high-end popular models like its foldable Galaxy Z phone.

Through its massive consumer electronics arm, Samsung sold 31 million PCs last year (fifth most sold globally)7, is a leading manufacturer of refrigerators, microwaves, washing machines, and other appliances, and is the largest TV-maker in the world—a position it has held for 19 consecutive years8.

Exhibit 1: Samsung’s Segment Earnings

Source: Company filings, Pzena analysis

Source: Company filings, Pzena analysis

Memory: An Essential Component of Modern Computing

Dynamic random access memory, or DRAM, is a type of memory that provides a CPU or GPU with fast access to temporary data storage for programs to run efficiently. It is a crucial component in increasingly powerful electronic devices, such as smartphones, PCs, tablets, and servers. Since 2007, DRAM demand has grown at a nearly 26% CAGR9, with industrywide revenue reaching $100bn in 202410. DRAM typically makes up less than 10% of a system’s total cost, but it is essential for modern CPUs to function, meaning volumes should continue to grow with computing power.

The industry is structured as an attractive oligopoly, with Samsung’s leading 39% market share followed by Korean peer SK Hynix and US-based Micron. These three companies collectively supply nearly 94% of the market11. Samsung’s historical dominance in conventional DRAM is a result of its scale and superior technology, affording it a discernable unit cost advantage over Hynix and Micron.

High-bandwidth memory (HBM) is a type of non-conventional DRAM enabling extremely high-bandwidth data transfer needed for artificial intelligence and other emerging technologies. While not a major part of the memory stack today, HBM is expected to become an increasingly larger piece of the profit pool over time, making it an important growth driver.

While it is a much smaller portion of their overall memory business, Samsung also maintains a leading ~29% market share12 position in NAND flash, a type of storage technology used in portable memory devices such as thumb drives and SD cards. The NAND industry is roughly half the size of DRAM, but it is similarly concentrated, with the largest 6 players controlling 90% of the supply13.

A Turn in the Memory Cycle

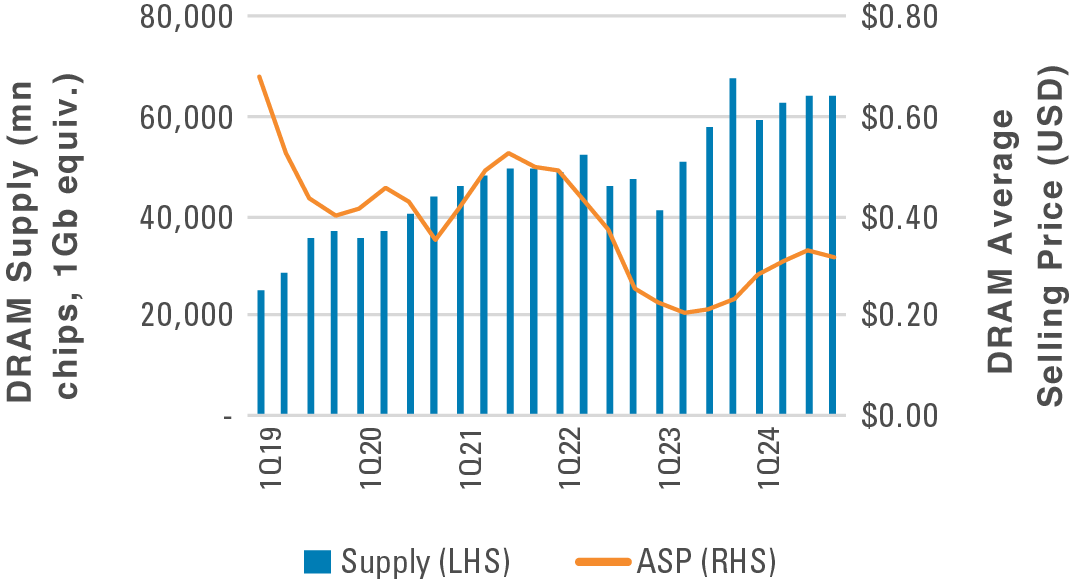

The surge in consumer spending during the early months of the COVID-19 pandemic was particularly acute for consumer electronics, with unit sales of notebooks and tablets up 44% and 81% respectively in the fourth quarter of 202014. Memory suppliers, assuming sustained peak demand, boosted capacity throughout 2021/22 just before end demand started to normalize; as a result, conventional DRAM prices collapsed, sinking industrywide profitability in 2023, and the market is still digesting the oversupply today. NAND, similarly affected by oversupply, also entered a downcycle, with prices falling nearly 50% year-over-year in 2023, exacerbating the profit decline in Samsung’s core memory unit.

Exhibit 2: Conventional DRAM Prices React to Oversupply

Source: Mizuho; ASP and supply of conventional DRAM (excludes HBM)

Samsung shelled out billions of dollars to boost production of conventional, more lagging-edge memory chips whose demand was waning due to inventory destocking. For context, Samsung’s DRAM capex between 2021 and 2023 accounted for 51% of total industry investment15, while its DRAM sales only represented 43% of global industry revenue16. Its cash return on DRAM, which incorporates both operating costs and capex, plummeted to 3% in 2023 after averaging over 30% pre-COVID17. With the stock down roughly 50% from its early 2021 high, we significantly increased our stake in late 2024.

DRAM Mix Shift and the HBM Controversy

Samsung’s management is focusing on what they can control to improve profitability in their core memory business. The company is pulling back capex on wafer expansion and redirecting spending towards node migration and HBM capacity. This should result in a memory mix that’s less exposed to lagging-edge nodes in oversupply, and more in line with Hynix and Micron’s leading-edge skew.

Investors have unsurprisingly been fixated on HBM, given its long-term growth potential and importance in powering the AI revolution. To that end, Samsung has thus far lagged both Hynix and Micron in qualifying for high-end HBM used in AI GPUs—specifically NVIDIA’s—eliciting some concern from investors. Based on our research, we believe that Samsung’s lack of qualification is more a result of being caught off guard by how quickly AI demand has exploded versus it having an insurmountable technology gap with peers on HBM chips. We therefore believe Samsung will ultimately participate in the anticipated demand wave, potentially capturing market share nearly proportional to its conventional DRAM share.

Fortress Balance Sheet Supports Higher Capital Returns

It’s also worth noting that Samsung has $63bn in net cash on its balance sheet, whereas its two competitors—Hynix and Micron—are both levered. The tech giant clearly has the financial wherewithal to return capital to shareholders, and management has been doing just that. Since 2018, when Samsung enhanced its capital return policy, the company has paid out nearly $67bn in cumulative dividends to shareholders, which equates to 34% of aggregate net income. Encouragingly, for the first time since 2017, Samsung started buying back its stock, and we expect the company to continue returning more of its war chest to shareholders going forward.

Conclusion

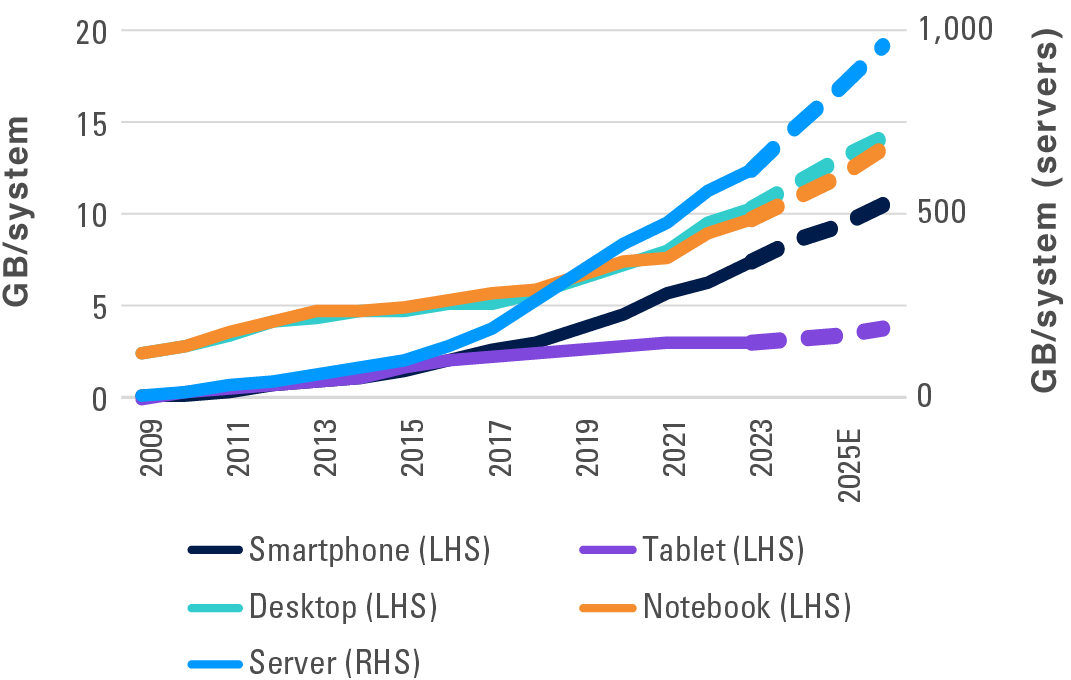

It’s easy to envision a more electrified, connected, and technologically advanced world in the near future. DRAM—particularly leading-edge nodes and, increasingly, HBM—will undeniably play a critical role in enabling such an environment. Memory content per device has steadily risen over the past two decades, with server DRAM exhibiting exponential growth (driven, in part, by AI servers), as computing power continues to expand.

Exhibit 3: DRAM Content per System Should Continue to Grow

Source: Bernstein

Source: Bernstein

After a period of somewhat short-sighted overinvestment, Samsung is, in our view, well-positioned to capitalize on an anticipated memory upcycle. Regarding the U.S. tariff risk, smartphones, PCs, and other electronics – including memory chips themselves – are currently exempt from reciprocal levies, so the direct impact on Samsung is minimal. Regardless, we are closely monitoring the situation, and our model reflects a wider range of outcomes reflecting U.S. trade policy uncertainty.

Even in the unlikely scenario that Samsung proves to be structurally behind its peers at the leading edge in HBM, and the company’s historical competitive dynamic in conventional DRAM deteriorates, resulting in commodity-like returns in perpetuity—none of which we’ve seen any evidence of—we believe the stock is fairly valued today, implying the HBM downside scenario is largely priced in.

In a concentrated, three-player market, we believe the gains from DRAM growth should largely accrue to Samsung in the years ahead, which the market, by ascribing a 8.2x multiple on our estimate of normal earnings, isn’t appreciating, in our view.

Footnotes

- FactSet; Est. EBIT CAGR FY24-FY27

- Capital expenditures

- TechInsights

- Bloomberg Intelligence

- Bloomberg Intelligence

- Average selling price

- Bloomberg Intelligence

- Samsung, Omdia

- Compound annual growth rate; UBS Total DRAM Demand (M 1Gb) 2007-24

- UBS

- Bernstein 2024 shipment estimates

- Morgan Stanley

- Morgan Stanley

- Morgan Stanley

- Mizuho

- Mizuho, company filings, Pzena analysis

- Company filings, Pzena analysis

- Company filings, Pzena analysis

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

Samsung Electronics was held in our Emerging Markets Focused Value, Emerging Markets Select Value, Global Focused Value, Global Value, International Focused Value, International Value, and other strategies during the first quarter 2025.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended), with additional authorisation for management of portfolios of investments, in accordance with mandates given by investors on a discretionary, client-by-client basis, where such portfolios include one or more of the investment instruments listed in Section C of the Annex to the MiFID (Markets in Financial Instruments) Regulations 2017 (S.I. No. 375 of 2017), as amended), and investment advice concerning one or more of the instruments listed in Annex I, Section C to Directive 2004/39/EC. PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2026 by ASIC Corporations (Amendment) Instrument 2024/497. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

The Pzena Emerging Markets Focused Value Fund, Pzena Emerging Markets Select Value Fund, Pzena Global Focused Value Fund, Pzena Global Value Fund are registered and approved under section 65 of CISCA.

Collective Investment Schemes in Securities (CIS) should be considered as medium- to long-term investments. The value may go up as well as down and past performance is not necessarily a guide to future performance. CISs are traded at the ruling price and can engage in scrip lending and borrowing. A schedule of fees, charges and maximum commissions is available on request from the Manager. A CIS may be closed to new investors in order for it to be managed more efficiently in accordance with its mandate. There is no guarantee in respect of capital or returns in a portfolio. Representative Office: Prescient Management Company (RF) (Pty) Ltd is registered and approved under the Collective Investment Schemes Control Act (No.45 of 2002). For any additional information such as fund prices, fees, brochures, minimum disclosure documents and application forms please go to www.pzena.com.

© Pzena Investment Management, LLC, 2025. All rights reserved.