Brazilian Equities: Unveiling Undervalued Opportunities

7 min read

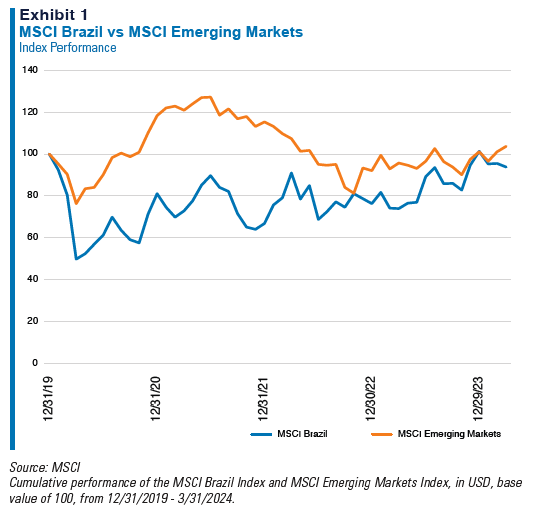

Brazilian equities performed well in 2022 and 2023, posting annual returns of 14% and 33%, respectively (Exhibit 1). Despite two years of strong performance, the MSCI Brazil Index continues to trade below its pre-COVID level.

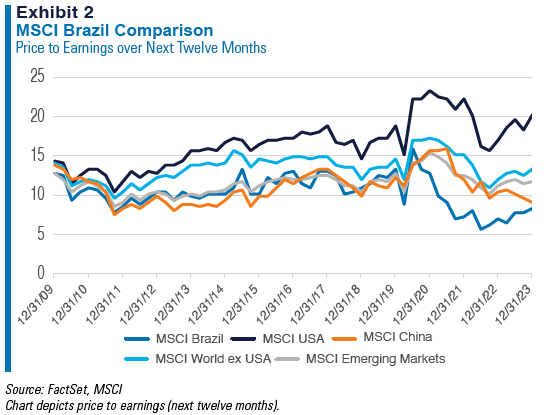

On a forward earnings basis, Brazilian equities are cheaper than they were during the early months of the COVID-19 pandemic, as well as the previous recession of 2014-2016 (Exhibit 2). Meanwhile, the macroeconomic backdrop is more encouraging than in the past. Unemployment is at its lowest level since 2015, and inflation is down to 4% from double-digit percentage points in 2021 and 2022.

Despite the benign economic environment, Brazilian equities appear priced for a gloomy outlook. Against this backdrop, we are invested in companies whose valuations we believe have been unduly punished because of macro and political fears, as well as company-specific controversies.

We added Ambev, the largest brewer in Latin America and Canada, to the portfolio in 2020. At the time, the company faced beer volume declines amid COVID-19 restrictions. Although volumes have bounced back to record highs, Ambev has faced several macroeconomic challenges, including higher input costs due to a weak Brazilian real and commodity cost inflation. More recently, shares fell due to earnings impacted by the devaluation of the Argentine peso, as well as uncertainty surrounding Brazil’s new tax regime. Despite potential future tax burdens, we believe the current share price more than discounts any forthcoming changes. Looking ahead, we are optimistic about Ambev’s underlying business. We believe the company’s premiumization strategy will contribute to further margin expansion, as macroeconomic headwinds abate.

Cosmetics and personal care company Natura & Co. is currently executing the integration of its 2020 acquisition of Avon. In 2023, Natura de-levered its balance sheet by first selling the Aesop brand to L’Oréal at an attractive valuation and subsequently selling its UK-based personal care retailer, The Body Shop. Since we added Natura in 2023, the company has begun to integrate Avon’s Latin America business with Natura’s existing unit. A key focus of management has been better incentivizing Avon agents to sell product rather than recruit other agents, which led to margin compression in the past. The integration has thus far translated to margin expansion driven by increased productivity and cross-selling.

When we added Banco do Brasil to the portfolio in 2023, the share price reflected fears that potential intervention by the newly elected government could hinder the company’s profitability, as seen during the presidency of Dilma Rousseff. The company currently offers the highest return on equity among Brazil’s largest banks. Asset quality has remained strong, and we view the current valuation as compelling.

FURTHER INFORMATION

This document is intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results. All investments involve risk, including risk of total loss.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

All investments involve risk, including loss of principal. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased

The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

For UK Investors: This marketing communication is issued by Pzena Investment Management, Limited (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Jersey Investors Only: Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For EU Investors Only: This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only: This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia. In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For South African Investors Only: Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial

Sector Conduct Authority (licence nr: 49029).