Highlighted Holding: Dollar General

4Q 2024

Dollar General (DG) is the largest retailer in the U.S. by store count, with more than 20,000 locations across the country. Its core business is selling a limited assortment of daily necessities, including groceries, household supplies, and other staples, typically to lower-income shoppers in rural America. DG’s unique combination of value and convenience has fueled impressive network expansion since its first location opened in 1955, and approximately 75% of the U.S. population now lives within five miles of a store1. Following decades of strong growth and enviable returns on capital, the company was caught off guard by the post-pandemic shift in consumer buying patterns, compounded by company-specific missteps and the outsized impact of inflation on DG’s core customer. Despite near-term headwinds, we do not believe the company’s value proposition has fundamentally changed; we believe management has a clear and credible plan to improve profitability, resulting in a very attractive valuation.

A Reputable Business Model

DG generates the bulk of its sales from the sub-$35,000/year income bracket—a cohort that includes more than 27 million households2. In contrast to other domestic dollar chains, DG’s footprint leans overwhelmingly rural, with approximately 80% of its stores located in towns with fewer than 20,000 people3. These communities are often underserved by competing food retail channels, including traditional grocers and big-box formats, creating an opening for DG to establish itself as a ubiquitous, small-box neighborhood market, where shoppers needing to stretch their budgets can grab necessities in non-bulk at competitive prices in between less frequent “stock up” trips to Walmart and the like. DG’s pricing is generally within three percent of Walmart’s, but the company’s playbook is to take share from less competitive channels, particularly conventional grocers and drugstores, where price gaps are closer to 20% and 40%, respectively.

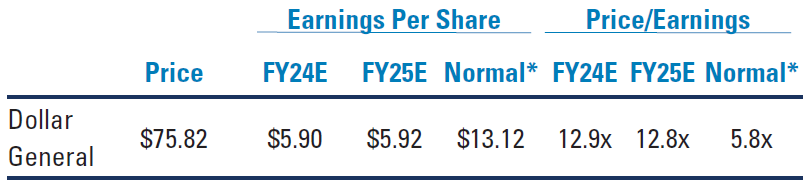

Fiscal quarter-end December 31. *Pzena estimate of normalized earnings.

Source: FactSet, Pzena analysis. Data as of December 31, 2024

Importantly, DG has been an aggressive first mover in many of its rural markets, effectively boxing out competing dollar chains in areas too small to sustain a second player. Superior network density and the resulting convenience advantage enables DG to compete against Walmart and deep discounters like Aldi. Given that the average ticket at DG is less than $20, even if a competitor further away is offering marginally lower prices, the incremental fuel costs quickly become material, rendering the trip uneconomical for low-income consumers.

Despite a proven business model, channel-leading scale, and a track record of profitable growth, DG shares are down nearly 70% over the past two years, and are now trading at an all-time low valuation multiple4.

The Downturn

In response to the stimulus-fueled boom in consumer spending during the pandemic, coupled with the procurement challenges faced by countless retailers in 2020/21, DG took on too much of the wrong inventory in management’s overzealousness to improve in-stock levels. For context, DG’s product mix is roughly 80% consumables and 20% higher-margin, non-consumables (e.g., home products, apparel). The timing proved inopportune, as consumer demand for discretionary goods was waning just as DG was building inventory and adding SKUs in the category. With so much excess product, DG’s existing distribution centers were quickly overwhelmed, forcing the company to lease inefficient temporary warehouse space to handle the overflow. DG’s inventory mismanagement triggered another headache for the company: elevated “shrink”, or theft (both internal and external), as well as damages that resulted from having too much product at the distribution centers and on store shelves.

Meanwhile, in-stock levels for the highest-velocity consumables that shoppers did want were unacceptably low, further eroding the in-store experience. At the same time, employee turnover rates spiked, as an already demanding job became intolerable for many. The company ultimately parted ways with its CEO in late 2023 after less than a year, opting to bring back former CEO Todd Vasos (2015–2022) for a second act.

DG’s same-store-sales growth (SSS) today remains well below its pre-COVID average of 2–4%5, while operating margins have been cut in half. DG’s single biggest margin headwind is higher “shrink”, and while it is far from the only retail chain facing pressure in that area, the impact has been more acute given DG’s over-inventoried supply chain, untimely rise in employee turnover, and low-cost operating model. The company had also added self-checkouts to most of its stores in recent years, and as staff became increasingly preoccupied triaging inventory, the front end of too many stores was neglected or abandoned altogether, exacerbating external theft.

Against this backdrop, the macroeconomic elephant in the room has been inflation, given its disproportionate impact on DG’s lower-income demographic, compounded by the roll-off of COVID-era stimulus payments, including SNAP benefit emergency allotments. Inflationary periods have historically been a boon for dollar stores, as middle-income households traded down into the channel, but the current cycle has been different, with persistently low unemployment and real wage growth for the upper end of the income spectrum. This has proven to be an inauspicious combination for DG: its core customer has pulled back on spending, especially in the most profitable non-consumable categories, but the shortfall has not been fully offset by incremental trade-down activity.

A Clear, Profitable Path Forward

DG’s challenges came to a head when the company reported quarterly results in August 2024, which revealed disappointing growth, a near-20% reduction in full-year EPS guidance, and incremental uncertainty regarding its longer-term recovery, prompting a 30% share price decline. Near-term earnings pressure notwithstanding, we believe management is taking the appropriate actions to right the ship and improve profitability.

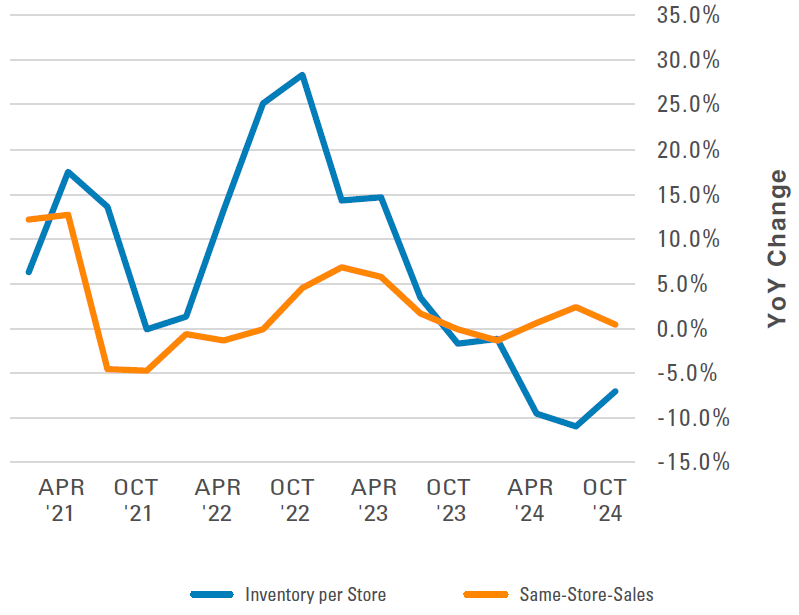

Specifically, CEO Todd Vasos is laser focused on getting DG “Back to Basics”, starting with addressing the inventory situation. This measure will take time, but we are seeing signs of progress: whereas inventory was growing at more than three times the rate of SSS as recently as 2022, it has since turned negative (Exhibit 1). Importantly, this normalization is being driven by non-consumables, which declined year-over-year by 17% and 9% on a per store basis in 2Q24 and 3Q24, respectively. This has enabled DG to exit 15 temporary warehouse facilities within the last year, and management expects to exit three more in 20256.

Exhibit 1: Inventory vs. Sales Growth

Source: FactSet

Beyond basic inventory reduction, DG has removed self-checkout functionality from most of its stores, which should reduce external shrink. Employee turnover is also down across the organization—an important step toward combatting internal shrink. Together, these and other initiatives, such as new anti-shrink incentives for managers, investments in labor, and bolstering the front end of stores, are already yielding results, as shrink flipped from a headwind to a 29-basis point tailwind7 in 3Q24. While this is a small improvement, it is important proof that management’s actions are bearing fruit.

In another positive move, DG is reallocating a large portion of its capex8 from growth to store remodels, with plans to upgrade around 20% of its existing footprint in 2025 alone—all without increasing total capital spending. Beyond 2025, management is considering upgrading most stores within the next three to five years, roughly doubling the prior remodel cadence. We believe this to be a good use of capital that should improve the in-store experience for customers in a variety of ways, such as expanding refrigerated space, installing more reliable HVAC systems, and reoptimizing planograms.

Conclusion

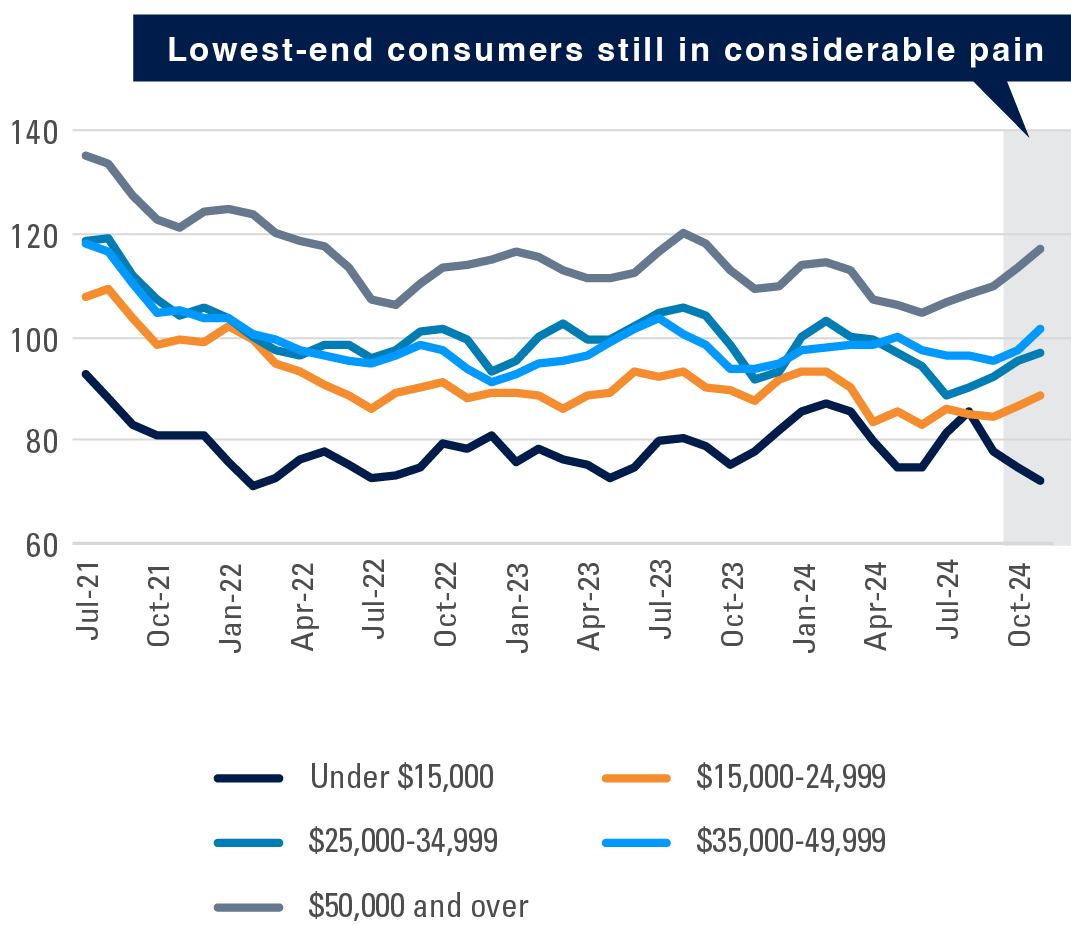

From our perspective, DG has the right management team in place, which has been empowered to execute a turnaround, and we are seeing green shoots despite the unfavorable macro environment. While consumer sentiment has improved in recent months, there is a clear distinction between income brackets, and sentiment is still broadly lower than pre-inflation levels across the spectrum (Exhibit 2).

Exhibit 2: Consumer Confidence Index (3-month Average)

Source: FactSet, The Conference Board

In our opinion, the current stock price is so low that only small improvements are needed for the shares to re-rate higher. In our model, we assume SSS growth never reverts to >2%, and that DG ultimately recovers about half the margin compression from the last few years; on both fronts, we believe improvement is largely within management’s control. Meanwhile, the eventual recovery of the lower-end consumer provides an additional souce of upside to both SSS and margins via mix benefits (i.e., a higher proportion of non-consumable sales). Given these assumptions, which we believe to be on the conservative side, DG is trading at under 6x our estimate of normal earnings.

Footnotes

- Company filings

- U.S. Census Bureau, 2023

- Company filings

- FactSet; P/E – NTM (monthly)

- FactSet; Avg. annual SSS growth from 2011–2020

- Company filings

- Company filings

- Capital expenditures

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

Dollar General was held in our Focused Value, Global Focused Value, Global Value, Large Cap Focused Value, Large Cap Value, Mid Cap Focused Value, and other strategies during the fourth quarter 2024.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Class Order CO 03/1100 and the transitional relief under ASIC Corporations (Repeal and Transitional) Instrument 2016/396, extended through 31 March 2026 by ASIC Corporations (Amendment) Instrument 2024/497. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2025. All rights reserved.