Fundamentals Point To An Enduring Value Cycle

First Quarter 2022 Commentary

This Pzena Investment Management, LLC (“Pzena”) commentary is a historical document and is intended solely for informational purposes. The views expressed reflect the views of Pzena Investment Management (“PIM”) as of the date published and are subject to change. Neither the writer nor PIM undertake to advise you of any changes in the views expressed therein. There is no guarantee that any projection, forecast, or opinion in this material has been or will be realized. Past performance is not indicative of future results. All investments involve risk, including risk of total loss.

History provides a strong case for maintaining focus on fundamentals in the face of geopolitical shocks and macroeconomic concerns.

We commonly hear two questions at opposite ends of the value cycle: “Is value dead?” and “Is the value cycle over?” The psychology behind these questions is what drives enduring value cycles and creates the opportunity for long-term alpha. Not long after the pro-value cycle started in October 2020, we started hearing the latter question.

Recent concerns relate to the impact of supply chain issues, rising inflation, and, more recently, Russia’s invasion of Ukraine. Higher prices, particularly for energy, and concerns about a Fed-induced recession are leading to talk of stagflation, something markets have not seen in more than four decades. The range of outcomes has certainly widened, but we believe history and market fundamentals support the case for an enduring value cycle.

GEOPOLITICAL SHOCKS AND VALUE CYCLES

As Russia amassed troops on the Ukrainian border, the market turned down sharply, as investors fled to perceived safety. In the face of a humanitarian crisis and a geopolitical showdown unlike anything seen since the Cold War, the fears were understandable.

While the long-term impact of the Russian invasion remains uncertain, we can look to history to examine the impact of geopolitical shocks on markets. We reviewed 38 notable geopolitical shocks that took place over the past 85 years to see the impact on the broader market and on value stocks specifically. We found that market sell-offs following these shocks were generally short lived, typically lasting on average just a couple of weeks. Contrary to popular belief, there was no place to hide; cheap stocks performed essentially in line with expensive stocks. The market generally recovered over the next couple of months, as the shock either wound up being temporary or businesses adapted to the changing landscape. Additionally, the volatility created by fear-induced sell-offs often created opportunities for disciplined value investors. Finally, we didn’t find a pro-value cycle that ended due to a singular geopolitical shock.

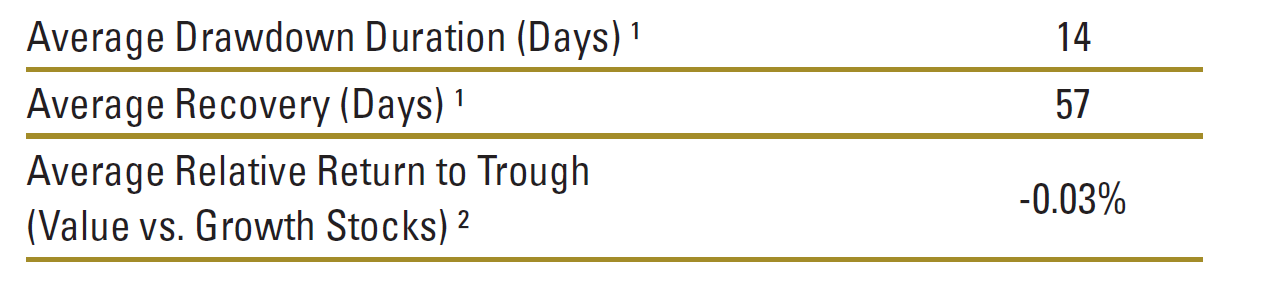

Drawdowns on Geopolitical Shocks the Past 85 Years

Source: Kenneth R. French, Pzena analysis. Table is based on 38 notable geopolitical shocks over the past 85 years.

¹ The US universe used is all NYSE, AMEX, and NASDAQ stocks defined by Kenneth R. French data library and calculated using cap-weighted returns.

² Value and Growth is defined as the cheapest and most expensive quintile of stocks based on book/price within the universe. To calculate the cohort of stocks for each quintile, we excluded the smallest 20% of the universe based on aggregate market capitalization to remove the small cap effect. Quintiles calculated using cumulative equal-weighted returns. Does not represent any specific Pzena product or service. Data as of March 31, 2022 and in US dollars.

Past performance is not indicative of future returns.

THE SPECTER OF STAGFLATION

Putting current concerns into historical context, this period is reminiscent of the stagflation period from 1973–1982. Recognizing no two periods are exactly alike, the similarities are striking. That period featured a regional conflict, leading to higher oil prices caused by the OPEC oil embargo. Inflation averaged 8.5%, and real GDP barely grew 2% per year. Despite three recessions in this period, the market returned an average of 8.2% per year, while value significantly outperformed at 18.9% per annum.

Of course, there is no way to predict how events will unfold. However, it is worth remembering that an investor in 1973, who happened to have perfect knowledge of future economic conditions, would most likely not have predicted the solid market returns that were realized over the next decade. That’s why it is important to focus on investing in deeply undervalued companies that have the market positions, business models, financial strength, and flexibility to thrive over the long term, through various economic conditions.

VALUE SPREADS SUPPORT AN ENDURING VALUE CYCLE

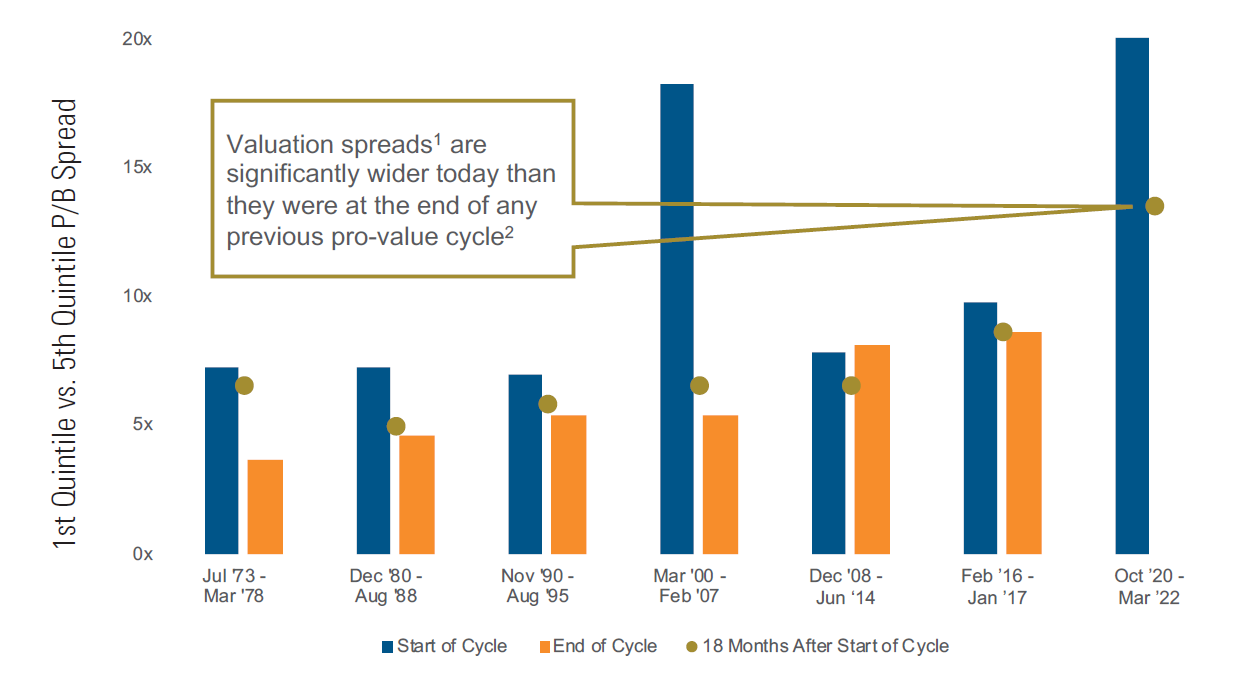

One common theme at the end of value cycles is the prevalence of narrow valuation spreads. This is important because as cheap stocks begin to outperform, disciplined value investors seek cheaper opportunities in other good businesses to replace fully valued holdings. Wide spreads indicate a rich opportunity set of cheap stocks for value investors to potentially rotate into, whereas narrow spreads indicate a smaller relative opportunity.

The current value cycle began 18 months ago when the first COVID-19 vaccine was announced. It accelerated as the Omicron wave subsided, and interest rates began to rise. Despite significant narrowing, spreads remain wider today than at any point historically other than the tech bubble. Impressively, spreads are more than twice as wide as they were at the same point during the post tech bubble value cycle (see Exhibit 1). These wide spreads provide the opportunity to take profits on holdings that have outperformed, and are approaching our estimate of fair value, and rotate into new, deeply undervalued opportunities that have lagged during the recovery (see Global Research Review, page 4).

Exhibit 1: Narrowing of Spreads Through a Value Cycle

Source: Sanford C. Bernstein & Co., Pzena analysis

¹ Price to book spread between the cheapest and most expensive quintile within the ~1,000 largest US stock universe (equal-weighted data).

² We define a cycle as when the relative performance of value vs. the market from the last peak or trough is at least +/-1500 basis points and has persisted for a minimum of 12 months. Here we define value as the equal-weighted returns of the cheapest quintile price to book within the ~1,000 largest US stock universe. The market represents the cap-weighted returns of the universe. Analysis does not represent any specific Pzena product or service. Data in US dollars through March 31, 2022. Past performance is not indicative of future returns.

LONG POST-RECESSION RECOVERIES

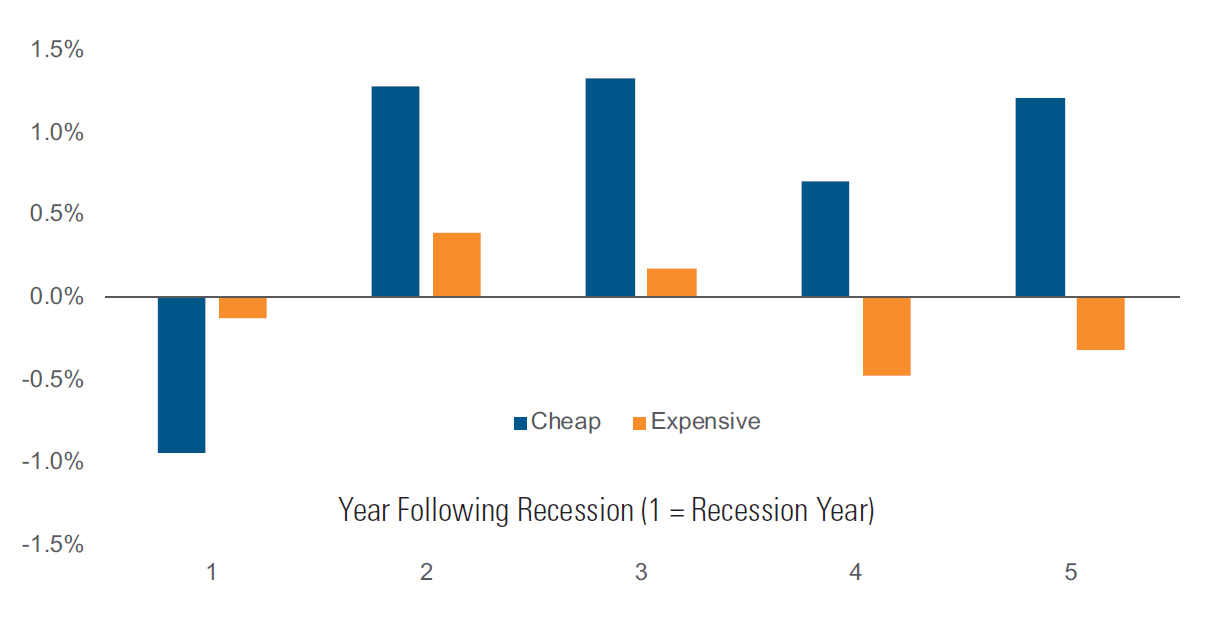

As discussed in our third quarter 2020 newsletter, cheap stocks have delivered significant five-year alpha following the start of recessions, outperforming the market by 530 basis points annually on average. Following a recession, the long path of value outperformance mirrors the operating recovery of cheap stocks. Over the previous three recessions, we found that while margins on cheap stocks contracted by 100 basis points in the calendar year a recession begins, they improved by an aggregate 450 basis points over the following four years (Exhibit 2) before stabilizing or contracting. This compares favorably to expensive stocks, which see margins contract only slightly going into a recession but also see them contract further later in an economic recovery.

This occurs because companies react to recessions by cutting costs in response to lower expected revenue. As economies emerge from recessions and companies’ top lines start to recover, revenue grows faster than costs, generating several years of expanding margins, often exceeding pre-recession levels. These results are more pronounced for cheap stocks, where company managements generally tend to cut costs the most.

Exhibit 2: Year-on-Year Operating Margin Change¹ Following the Past Three US Recessions²

Source: FactSet, National Bureau of Economic Research, Pzena analysis

¹ Average change in operating margins of the cheapest and most expensive stocks (based on price-to-book quintiles) within the Russell 1000 Index; all equal-weighted data.

² Recessions in 1990, 2001, and 2008 per NBER.

The recession and recovery around COVID-19 have been similar to past economic cycles, both in timing and trajectory. Margins on cheap stocks plummeted quickly in 2020, as the world was in lockdown for a good part of the year. The recovery was just as rapid, resulting in 2021 margins that exceeded 2019’s. These margins were achieved in the face of rising inflation, indicating, so far, that companies have been able to pass along higher input prices. For companies experiencing below-trend demand for their products and services, the prospect is quite good for continued earnings growth, as they benefit from operating leverage driven by revenue recovery.

CONCLUSION

It is certainly hard to ignore the daily news flow without imagining the possible negative implications to equities. It is also impossible to predict whether there will be temporary interruptions in the value cycle caused by some of these events. However, we believe the lesson from history is clear: In the face of geopolitical fears, investors should stay the course in value because the market’s reaction typically doesn’t last long, and the recovery is powerful and enduring. Even after a period of significant outperformance, we believe the outlook for value remains strong given the solid post-recession fundamentals for cheap stocks.

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results. All investments involve risk, including risk of total loss.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Mirabella Advisers LLP, which is authorised and regulated by the Financial Conduct Authority. The Pzena documents are only made available to professional clients and eligible counterparties as defined by the FCA. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2022. All rights reserved.