Highlighted Holding: Baxter International

9 min read

Baxter International is a diversified manufacturer of essential medical products and equipment, supplying hospitals and healthcare clinics in over 100 countries. In 2022, Baxter was hit by a perfect storm of headwinds that impacted all four of its segments in tandem, sending shares down over 50% to an eight-year low. This considerable decline in valuation for a durable business experiencing some cyclical pain was, in our view, an exploitable value opportunity.

Baxter’s Business Breakdown

Baxter has four operating segments, with its core Medical Products & Therapies (MPT) unit accounting for a third of total sales. Through this business, Baxter produces infusion pumps, clinical nutrition products, surgical instruments, and IV fluids—where it maintains a dominant ~70% market share, delivering more than one million IV bags per day.1 Baxter’s Healthcare Systems & Technologies business focuses on durable hospital products, such as smart beds, patient monitoring systems, and surgery room fixtures, while its pharma unit develops generic injectables and inhaled anesthesia. Lastly is Baxter’s Kidney Care unit (~30% of revenue)—a stable, but low-margin, mostly non-U.S. business that skews heavily to peritoneal dialysis (PD) home use. Importantly, this business is earmarked to be spun off in 2024 in a transaction we believe could unlock significant value for shareholders.

BAX Shares Reach Critical Condition

Baxter’s core earnings are largely a function of hospital utilization. During the pandemic, the company suffered a decline in revenue, as hospital admissions fell to the lowest levels in decades, while surgical procedures also dropped. Volumes rebounded in subsequent quarters but are still yet to fully recover to pre-pandemic levels, weighing on Baxter’s top line.

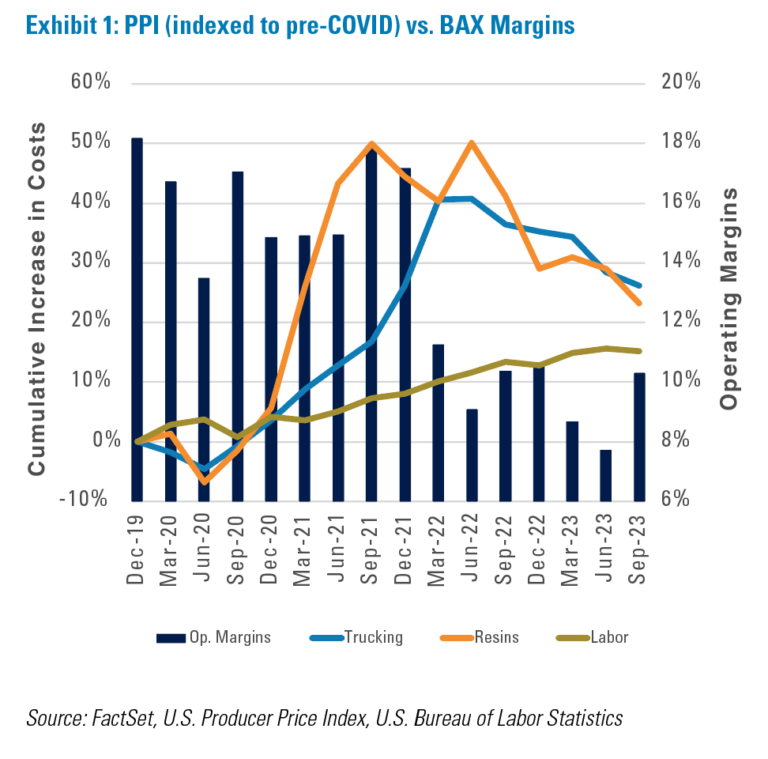

Inflation began to rear its ugly head in 2021, increasing Baxter’s costs by around $1B, with the breakdown roughly 50% materials, 30% logistics, and 20% labor. Due to the nature of Baxter’s core products, which are mostly high-volume commoditized consumables, the manufacturer is particularly sensitive to inflationary pressures and supply chain snarls. Raw material prices like oil-based resins spiked, while fuel costs also swelled, taking a toll on its key medical therapies and renal businesses. Because Baxter’s Kidney Care unit is predominantly PD-focused, a key aspect of the business involves the delivery of dialysis products and materials to patients’ homes, making last-mile logistical costs especially damaging in an inflationary environment. Additionally, procuring semiconductors became nearly impossible, hindering Baxter’s ability to meet demand in its healthcare systems business.

Many of Baxter’s current contracts were negotiated with group purchasing organizations (GPOs) six or more years ago, when the notion of 9% headline inflation was inconceivable. As a result, Baxter’s long-term, fixed price contracts had no serious price escalators embedded, rendering them far less lucrative once costs spiked, as evidenced by 1H23 margins at their lowest level in seven years (Exhibit 1).

As a result of these combined headwinds, Baxter’s forward multiple collapsed from 24.5× just before the March 2020 pandemic sell-off, when it was on par with the industry, to 14.5× in the summer of 2023—41% below the industry.2 We initiated a position with shares trading around 9× our estimate of the company’s normal earnings.

The Ozempic effect

On October 10th, Novo Nordisk announced the early conclusion of its kidney outcomes trial, which aimed to assess whether Ozempic slows the progression of chronic kidney disease, citing significant efficacy. The news sent shares of Baxter (along with peers) down 15% on the premise that its renal business would be permanently impaired. After researching the issue, we determined that the impact to Baxter’s normal earnings power, if anything, would likely be de minimis; with shares trading at under 7× our normal earnings estimate, we increased our stake in the company.

Margin Reset

Baxter’s GPO contracts in the U.S. represent the lion’s share of its core MPT revenue and are up for renewal in 2025. We point out that Baxter, as the largest IV manufacturer in the world, has significant scale and global reach, while high barriers to entry make for an attractive oligopolistic market structure. As such, we expect Baxter to negotiate materially better terms for its renewed contracts, which should provide a nice boost to MPT margins even if inflation remains elevated (margins have already begun to inflect even before the updated contracts, as high-cost inventory is being sold down).

While contract renewals are perhaps the most concrete near-term catalyst for earnings normalization, Baxter’s management isn’t stopping there. The company is taking self-help cost initiatives by increasing plant automation, improving suppliers’ direct access (i.e., cutting out middlemen), and reducing single-source suppliers. Baxter has also been divesting non-core assets—most recently, its BioPharma Solutions business—to reduce leverage and simplify the company.

Baxter is expected to spin out its renal business next year, in what has the potential to be a value-accretive corporate action. Management’s rationale for offloading Kidney Care is, in our view, sound. The business is distinct from Baxter’s core operations, caters to different end users, is internationally focused, low-margin, and highly dependent on payor reimbursements. As such, it doesn’t make much financial sense for Baxter to hold onto Kidney Care, and the math underpinning the future transaction is compelling. Earnings are currently depressed due to the aforementioned cost inflation in conjunction with pandemic-induced excess mortality. We estimate that Kidney Care should earn roughly $640M in normal EBITA,3 which equates to an EV of $10.1B.4 After removing this business from Baxter’s current EV of $30B, the pro forma medical products company’s EV/EBITA5 multiple is roughly 8.2×. This compares to an industry forward multiple of over 18×6—a considerable differential7 we believe could be narrowed upon a successful spin-off of Kidney Care next year.

Secular Earnings Drivers

Beyond the more near-term tangible profit opportunities, Baxter has several structural tailwinds working in its favor. The pharma business, which has been contending with increased competition in the U.S. generic injectables market, is showing signs of life, as the FDA has become more aggressive post-pandemic. Baxter is also in the process of decentralizing its cost structure. For the first time, segment-level executives will be accountable for their own P&Ls. We believe this could lead to future cost savings and strategic divestments, as management will look to maximize profit at each individual business unit. Additionally, the company is awaiting FDA approval for its latest pump, which is expected to arrive in 2024 and should provide a major boost to its Infusion Therapies business.

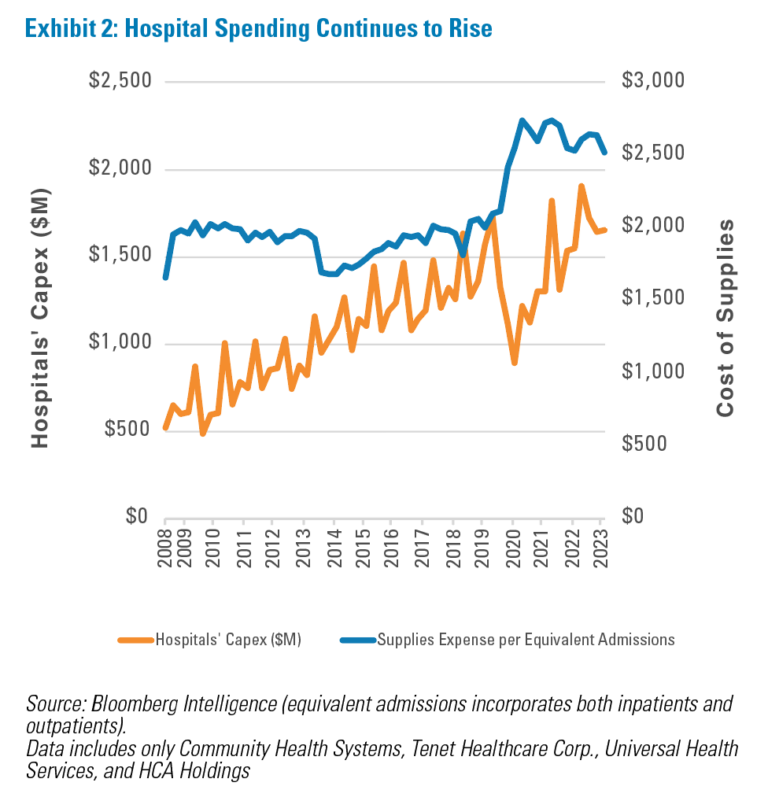

Ultimately, Baxter’s long-term earnings trajectory will be a function of total hospital expenditures, regardless of any short-term volatility on input costs, patient volumes, payor reimbursements, etc. The reality is that hospitals’ outlays have only been increasing over time (Exhibit 2). Considering the nation’s aging population, the expectation is for hospital utilization and capacity to keep rising over the long run—the benefits of which should accrue to Baxter, given the medical supplier’s discernable economic moat. In fact, the U.S. government projects spending on medical equipment & products to top $277B by 2031,8 representing a 5.2% CAGR9 from 2022.

Conclusion

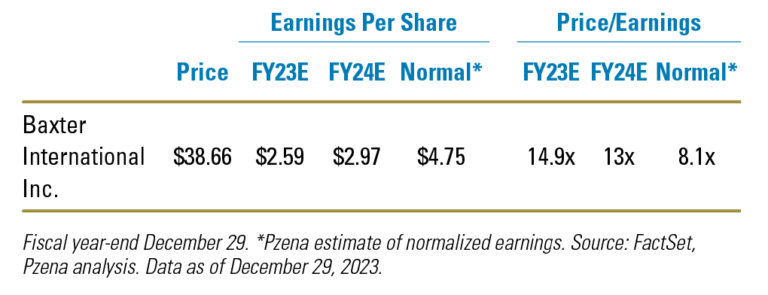

With hospital staffing back above its pre-pandemic trend, and healthcare job openings down over 28% from 2022’s peak,10 Baxter’s end markets are rapidly improving. At the same time, inflation is moderating, while potentially major revenue drivers are on the horizon. The stock’s 9.8× forward EV/EBITDA multiple is the lowest (outside of November’s reading) since it became a separate company in 2015 (post-Baxalta spin-off), and an indication that the market is severely underappreciating Baxter’s normal earnings power—which we estimate at $4.75/share, equating to a multiple of just 8.1×.

Footnotes

- Company filings

- FactSet, Russell 1000 – Medical Equipment and Services industry P/E – NTM

- Earnings before interest, taxes, and amortization

- Applying an industry median FY22 15.9× EV/EBITA multiple on the renal business

- Pzena’s estimate of RemainCo’s normal EBITA of $2.45B

- Russell 1000 – Medical Equipment and Services

- Median NTM EV/EBITDA differential is ~3.1× (monthly data, Dec. ’13–Dec. ’23)

- Centers for Medicare & Medicaid Services projections for durable medical equipment and other non-durable medical products

- Compound annual growth rate

- FactSet, U.S. Bureau of Labor Statistics, Pzena analysis of Hospitals employment and Health Care & Social Assistance job openings

“Baxter International, a vital supplier of medical products and devices, currently has several major catalysts for earnings normalization. We believe the company’s material valuation discount is unjustified. ”

FURTHER INFORMATION

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

Baxter International was held in our Focused Value, Global Focused Value, Global Value, Large Cap Focused Value, Large Cap Value, Mid Cap Focused Value, and other strategies during the fourth quarter of 2023.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2024. All rights reserved.