Energy Transition Update (2Q 2024)

Stewardship Insights – 2Q 2024 | For Professional Investors Only

9 min read

The mainstream energy transition narrative has evolved since we last wrote about the issue in February 2021. We are observing more explicit acknowledgement of the myriad of political, social, and economic tradeoffs that must be navigated. Catalysts for this shift include changes in the macroeconomic environment, the rising importance of energy security, and uneven return profiles for some clean technology investments. Against this backdrop, companies have adjusted energy transition plans to maintain credibility and sources of competitive advantage. Our approach to the energy transition, however, remains unchanged. We have always believed in taking a dynamic fundamental view of the companies we invest in. Below we outline how we continue to think about the evolving demands of the energy transition.

What Has Changed

Macroeconomic environment

Against the backdrop of the war in Ukraine and recent periods of high inflation, the policy priorities of the energy transition now go beyond “decarbonization at all costs” to include previously unacknowledged tradeoffs with energy security and affordability.

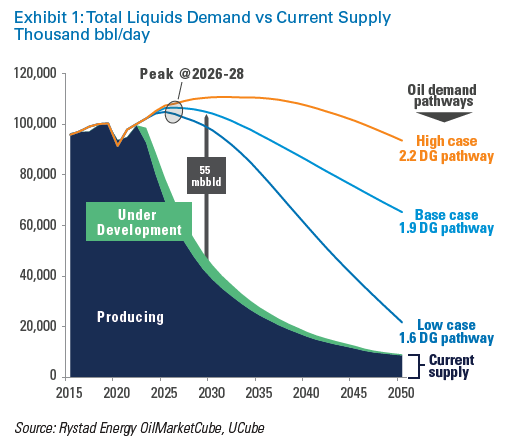

Updated view of near-/medium-term oil and gas demand

The 2021 IEA Net Zero Scenario laid out a pathway for the world to reach net-zero emissions by 2050 with the technology viable at the time. While not intended as a deterministic prediction, a series of attention-grabbing headlines followed about the need to cease all “new” investments in oil and gas. However, demand for oil and gas is still rising (see Figure 1). Not only are trillions of barrels of oil needed in all scenarios, but so is “new” investment to meet the energy needs of the global economy. Natural gas is expected to remain an important transition fuel for longer than oil, with demand peaking in the mid-2030s. This is important if we are to rapidly replace coal, which still comprises 30% of the global energy mix.

Clean technology returns

The recent disappointing return profiles for some clean technology investments have been notable. Offshore wind in particular was disproportionately affected by post-Covid supply chain issues and inflation. Structural challenges also remain in the deployment of wind and solar at scale, including resolving intermittency and grid stability concerns; despite deployment costs coming down, renewables projects continue to earn just 5-8% on their equity compared to more than 15% for oil and gas1. Many technologies acknowledged as important to reach net zero by 2050 are still at relatively low TRLs2 and/or are not yet fully commercially viable.

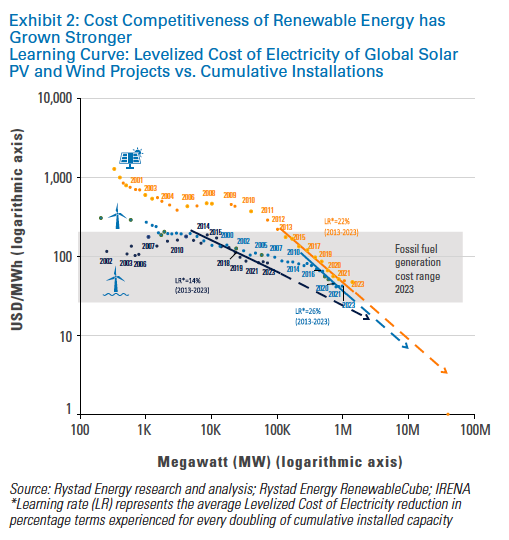

Despite these challenges, there are signs of growing scale. While not the only important measure of progress, the cost competitiveness of renewable energy has improved significantly (see Figure 2).

According to the IEA3, clean energy investment is expected to reach $2 trillion for the first time in 2024, putting the clean-energy-to-fossil-fuel investment ratio at roughly 2:1. Renewables investments are expected to account for $770 billion in 2024, which represents roughly 10 times that of investments in coal and gas-fired electricity generation.

Investment implications

When evaluating the impact of these shifts on our investments, signs of scale in the energy transition must be balanced with the economic, geopolitical, and regulatory realities.

Sharpening of energy transition plans

Short- to medium-term, companies have had to acknowledge inherent decarbonization tradeoffs more explicitly and focus on areas of true competitive advantage. Shell’s March 2024 energy transition update was interpreted by some as a weakening of previous climate targets. However, our view is that the changes to Shell’s transition plan better reflect new market realities and are therefore credible. Shell’s unique competitive advantage in LNG will allow it to play a key role in energy affordability and security for years to come, while Shell continues to invest in areas of competitive advantage within the energy transition (carbon capture, biofuels, etc.).

ArcelorMittal (MT) maintaining previously issued green capex guidance (while peer SSAB recently increased green capex guidance 20-30%, citing cost inflation) was interpreted by some as a weakening of decarbonization commitments. Our view is that MT’s more cautious approach is prudent because it maintains capital discipline in the short term and allows MT to keep decarbonization technology options open in the medium to long term. MT maintains a competitive advantage by proactively securing government funds and using its global footprint to import lower carbon material into Europe from geographies, such as Brazil, where it may be cheaper to decarbonize steel production.

Innovation

Innovation is required to meet the goals of the energy transition, and we see attractive sources among industry incumbents from traditionally higher emitting sectors. Incumbents have substantial technological know-how that can be effectively deployed into low carbon solutions, such as hydrogen, sustainable fuels, carbon capture, and circular plastics. For example, Shell’s CANSOLV carbon capture system is one of the industry’s leading solutions. Equinor is taking the lead on developing a comprehensive carbon capture solution for the European industry with its Northern Lights project, while Exxon is doing the same for the US with its Houston carbon hub project.

Industry incumbents are also increasingly partnering with innovative early-stage clean technology start-ups, largely in private markets. For example, Vale signed an MOU with GravitHY, founded in 2022 as a green iron pure play, with the intent to become operational in France by 2028. Vale will act as the number one supplier for high-grade iron ore and as the technology partner on developing lower carbon direct reduced iron and green briquettes technology.

The innovation potential for industry incumbents is also supported by academic literature. For example, 15% of the energy sector’s patent base are green, and utilities and industrial commodities also have high green patent shares.

Conclusion

As when we first wrote about this topic in 2021, our view is that the path of the energy transition is not necessarily linear. A one-size-fits-all approach oversimplifies the realities for companies balancing competing priorities, particularly as lower carbon technologies continue to mature. Deep fundamental research matters now more than ever to figure out which companies are best positioned for the energy transition, not just at a specific point in time but over time. We continue to analyze competitive advantage and the innovation potential required to build differentiated and profitable energy transition strategies. Engagement remains the best tool at our disposal to encourage companies to deploy capital effectively and build shareholder value over time.

Footnotes

-

Brett Christophers, a British academic, builds a compelling case in his recent book The Price is Wrong that profitability has been an underappreciated impediment to at-scale deployment of wind and solar.

-

Technology Readiness Level. Nomenclature originated at NASA to indicate the level of technological maturity. Has now been adopted by the IEA in the Energy Transition Pathway Clean Energy Technology Guide, which contains information for over 550 individual technology designs on a TRL scale of 1-11

-

IEA 2024 World Energy Investment Report.

“The mainstream energy transition narrative has evolved in light of recent social, political, and economic shifts. Our approach to researching and analyzing our investments has remained consistent, as we continue to dynamically analyze the credibility of company transition plans. ”

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The specific portfolio securities discussed in this presentation are included for illustrative purposes only and were selected based on their ability to help you better understand our investment process. They were selected from securities in one or more of our strategies and were not selected based on performance. They do not represent all of the securities purchased or sold for our client accounts during any particular period, and it should not be assumed that investments in such securities were or will be profitable. PIM is a discretionary investment manager and does not make “recommendations” to buy or sell any securities. There is no assurance that any securities discussed herein remain in our portfolios at the time you receive this presentation or that securities sold have not been repurchased.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2025. All rights reserved.