Why We Are Active Value Investors

9 min read

Third Quarter 2023 Commentary

Despite a wealth of empirical evidence highlighting the superior returns1 associated with value investing, many investors are still hesitant to fully embrace it. This reluctance to fully commit to value investing has led many investors to turn to “value-light” strategies, which sidestep the most contentious and volatile stocks, often sacrificing the core tenets of the value philosophy. In this essay, we will do the following:

- Show how the returns of value investing have been superior to all styles, including value-light

- Dispel misconceptions about the risk profile of value stocks

- Evaluate the damage indexing value has done to asset allocation over the past 20+ years

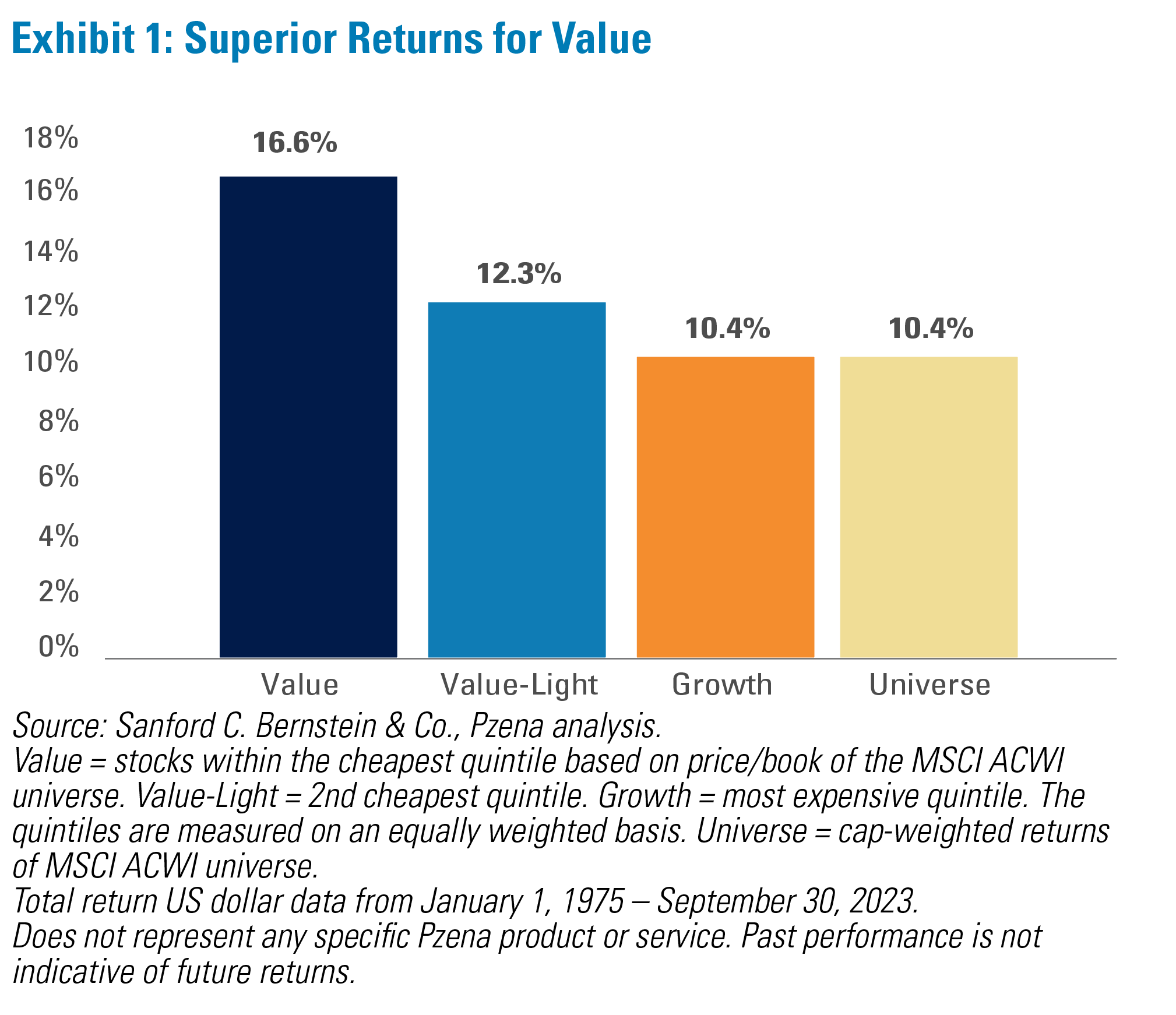

Superior Returns for Value

Superior returns from value investing have passed the scrutiny of a myriad of studies since Graham and Dodd first printed Security Analysis nearly a century ago. In addition, the data clearly make the case for selling stocks that perform well and reinvesting in the cheapest quintile, instead of holding value-light stocks which, on average, doesn’t add as much value (Exhibit 1).

Despite the preponderance of evidence, investors have always been slow to embrace value stocks, which we believe occurs for two reasons:

- There can be pain and discomfort when purchasing out-of-favor stocks.

- There is a perception that value stocks are riskier.

To deal with these issues and still capture the value premium, some investors have pursued value-light strategies. These strategies go by several different names, usually with some adjective appended to value, and generally avoid the most controversial and out-of-favor stocks. Since these strategies purchase stocks beyond

the cheapest quintile, and historically have much lower returns, we believe they sacrifice too much of the rewards of the value philosophy to generate significant long-term outperformance.

The “Value is Riskier” Myth

Value investing works because most investors shy away from the near-term uncertainty and potential pain of holding out-of-favor stocks. Ben Graham’s parable of Mr. Market selling out-of-favor stocks to purchase stocks that are in favor is as true today as it was when he first wrote it in 1949.

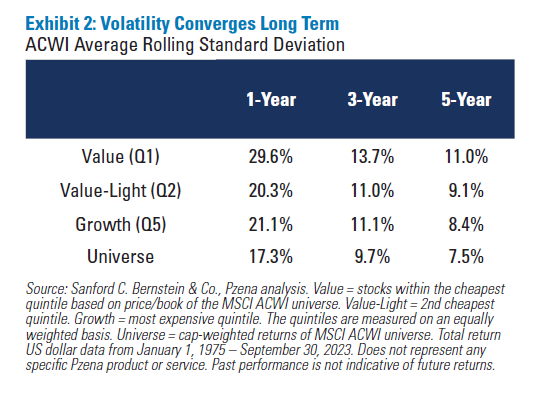

While value investing works due to behavioral reasons, academics have tried to explain its superior returns by theorizing they are generated by taking additional risk. The measure of “risk” they use is generally volatility of short-term returns, which we believe is a poor measure of risk. Using a more appropriate (yet imperfect) proxy for risk, such as five-year volatility, value investing is superior when considered in the context of the returns generated relative to volatility.

Equities in general are a relatively volatile asset class, particularly in the near term. While value stocks can be more volatile in shorter periods, we would not recommend any style of equity investing over less than a five-year time horizon, as the volatility is too high to justify the potential return. However, over longer periods, the incremental volatility of value stocks is less material versus other styles and the market (Exhibit 2).

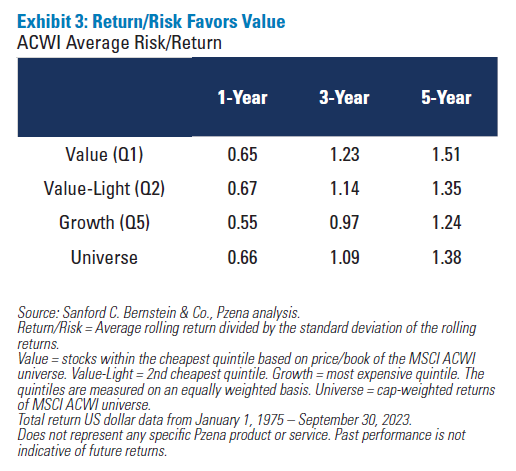

Looking at volatility in isolation ignores the significant reward an investor may earn for bearing the potential near-term volatility. Comparing the reward to the volatility over the same period, value is in line with the market over one-year periods and outshines all other strategies over longer periods (Exhibit 3). Interestingly, for value-light stocks, the return/risk ratio, is more or less in line with the market as a whole, meaning value-light strategies are sacrificing the return of value strategies while paying higher fees for the same return/risk profile as the market.

The Value Dispersion Myth

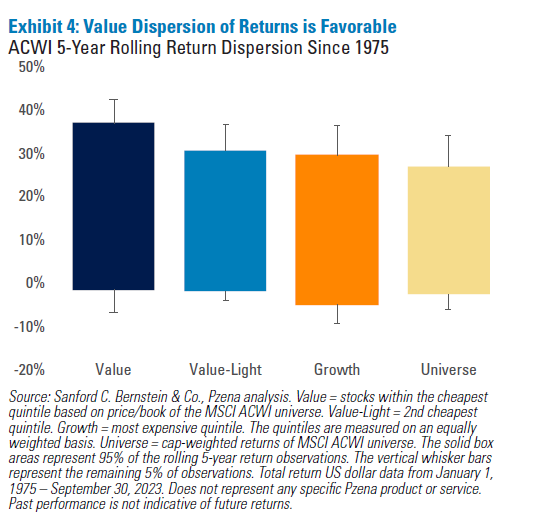

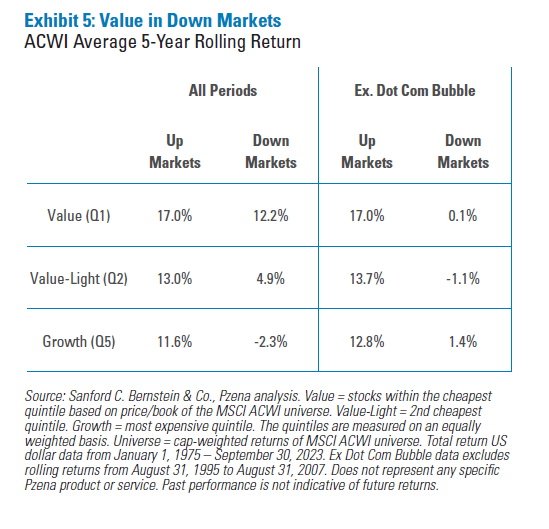

Value’s wider dispersion of returns is a related criticism of value investing. Over rolling 5-year holding periods, value returns are 18% more dispersed than value-light and 31% more dispersed than the universe. However, more dispersed does not mean worse, and in this case, it is good dispersion. The top-performing 5-year periods are significantly higher than the market’s top returns and all other styles, while the worst performance is comparable or better (Exhibit 4—top and bottom of the boxes). Even for the extreme downside periods (Exhibit 4—whiskers), value is in line or better, on average, while performing significantly better in the extreme upside performance periods.

While value is also criticized for performance in down markets, it does better than value-light portfolios in both up and down markets, even excluding the dot-com era, which was the period of value’s best alpha generation (Exhibit 5). Finally, value portfolios generated negative five-year absolute returns just 3.8% of the time, versus 5.4% for value-light and 8.8% for the universe.

Indexing Value — A Flawed Approach

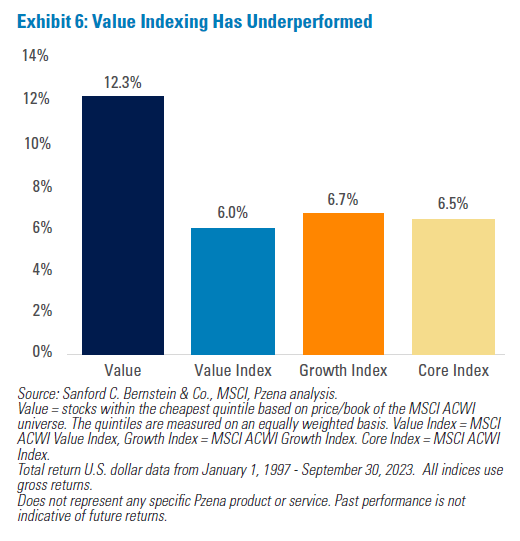

As we mentioned in last quarter’s newsletter, the vagaries of index formation have led to value indices that are filled with stocks that we would not consider bargains. Since value and growth indices match cumulative market caps, expensive mega-caps have caused many growth stocks to fall into the value index. Bizarrely, some stocks wind up with a portion of their weighting in both the value and the growth series. We are firm believers that a stock is either cheap or not.

This has caused investors who chose to index their value allocation, presumably to lower volatility, to significantly underperform. While ACWI Value has significantly underperformed MSCI ACWI and MSCI ACWI Growth since MSCI constituted the indices in 1997, true ACWI value, as measured by the cheapest quintile of stocks, was the top-performing style (Exhibit 6).

Conclusion — Patience Pays

As most performance studies have shown, value investing has generated superior returns, and we’ve shown that those returns have outpaced those of value-light portfolios. In addition, over reasonable investment horizons value stocks:

- are superior on a return/risk basis

- exhibit volatility levels that converge with other styles and the universe over longer time periods

- while more dispersed, have better dispersion characteristics

- do better in up or down markets on average

Finally, indexing a value allocation has historically not been a good strategy, likely due to index formation vagaries.

NOTE: This is the first in our Why We Are Active Value Investors series. In future quarters, we will further explore other topics, including the importance of patience over long time horizons and why deep value works.

“Many investors opt for “value-light” strategies that sacrifice key value principles. This essay demonstrates value investing’s superior returns compared to growth and value-light strategies, dispels risk misconceptions, and exposes the flaws of indexing value.”

Further Information

These materials are intended solely for informational purposes. The views expressed reflect the current views of Pzena Investment Management (“PIM”) as of the date hereof and are subject to change. PIM is a registered investment adviser registered with the United States Securities and Exchange Commission. PIM does not undertake to advise you of any changes in the views expressed herein. There is no guarantee that any projection, forecast, or opinion in this material will be realized. Past performance is not indicative of future results.

All investments involve risk, including loss of principal. Investments may be in a variety of currencies and therefore changes in rates of exchange between currencies may cause the value of investments to decrease or increase. The price of equity securities may rise or fall because of economic or political changes or changes in a company’s financial condition, sometimes rapidly or unpredictably. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. These risks are greater for investments in Emerging Markets. Investments in small-cap or mid-cap companies involve additional risks such as limited liquidity and greater volatility than larger companies. PIM’s strategies emphasize a “value” style of investing, which targets undervalued companies with characteristics for improved valuations. This style of investing is subject to the risk that the valuations never improve or that returns on “value” securities may not move in tandem with the returns on other styles of investing or the stock market in general.

This document does not constitute a current or past recommendation, an offer, or solicitation of an offer to purchase any securities or provide investment advisory services and should not be construed as such. The information contained herein is general in nature and does not constitute legal, tax, or investment advice. PIM does not make any warranty, express or implied, as to the information’s accuracy or completeness. Prospective investors are encouraged to consult their own professional advisers as to the implications of making an investment in any securities or investment advisory services.

The MSCI ACWI Index captures large and mid-cap representations across 23 Developed markets and 24 Emerging Markets countries. The index covers approximately 85% of the global investable equity opportunity set. The MSCI ACWI Value Index and MSCI ACWI Growth Index are constructed from the parent index using value investment style characteristics and growth investment style characteristics, respectively. The indices cannot be invested in directly.

The MSCI information may only be used for internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the MSCI Parties) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages.

For U.K. Investors Only:

This marketing communication is issued by Pzena Investment Management, Ltd. (“PIM UK”). PIM UK is a limited company registered in England and Wales with registered number 09380422, and its registered office is at 34-37 Liverpool Street, London EC2M 7PP, United Kingdom. PIM UK is an appointed representative of Vittoria & Partners LLP (FRN 709710), which is authorised and regulated by the Financial Conduct Authority (“FCA”). The Pzena documents have been approved by Vittoria & Partners LLP and, in the UK, are only made available to professional clients and eligible counterparties as defined by the FCA.

For EU Investors Only:

This marketing communication is issued by Pzena Investment Management Europe Limited (“PIM Europe”). PIM Europe (No. C457984) is authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011, as amended). PIM Europe is registered in Ireland with the Companies Registration Office (No. 699811), with its registered office at Riverside One, Sir John Rogerson’s Quay, Dublin, 2, Ireland. Past performance is not indicative of future results. The value of your investment may go down as well as up, and you may not receive upon redemption the full amount of your original investment. The views and statements contained herein are those of Pzena Investment Management and are based on internal research.

For Australia and New Zealand Investors Only:

This document has been prepared and issued by Pzena Investment Management, LLC (ARBN 108 743 415), a limited liability company (“Pzena”). Pzena is regulated by the Securities and Exchange Commission (SEC) under U.S. laws, which differ from Australian laws. Pzena is exempt from the requirement to hold an Australian financial services license in Australia in accordance with ASIC Corporations (Repeal and Transitional) Instrument 2016/396. Pzena offers financial services in Australia to ‘wholesale clients’ only pursuant to that exemption. This document is not intended to be distributed or passed on, directly or indirectly, to any other class of persons in Australia.

In New Zealand, any offer is limited to ‘wholesale investors’ within the meaning of clause 3(2) of Schedule 1 of the Financial Markets Conduct Act 2013 (‘FMCA’). This document is not to be treated as an offer, and is not capable of acceptance by, any person in New Zealand who is not a Wholesale Investor.

For Jersey Investors Only:

Consent under the Control of Borrowing (Jersey) Order 1958 (the “COBO” Order) has not been obtained for the circulation of this document. Accordingly, the offer that is the subject of this document may only be made in Jersey where the offer is valid in the United Kingdom or Guernsey and is circulated in Jersey only to persons similar to those to whom, and in a manner similar to that in which, it is for the time being circulated in the United Kingdom, or Guernsey, as the case may be. The directors may, but are not obliged to, apply for such consent in the future. The services and/or products discussed herein are only suitable for sophisticated investors who understand the risks involved. Neither Pzena Investment Management, Ltd. nor Pzena Investment Management, LLC nor the activities of any functionary with regard to either Pzena Investment Management, Ltd. or Pzena Investment Management, LLC are subject to the provisions of the Financial Services (Jersey) Law 1998.

For South African Investors Only:

Pzena Investment Management, LLC is an authorised financial services provider licensed by the South African Financial Sector Conduct Authority (licence nr: 49029).

© Pzena Investment Management, LLC, 2023. All rights reserved.